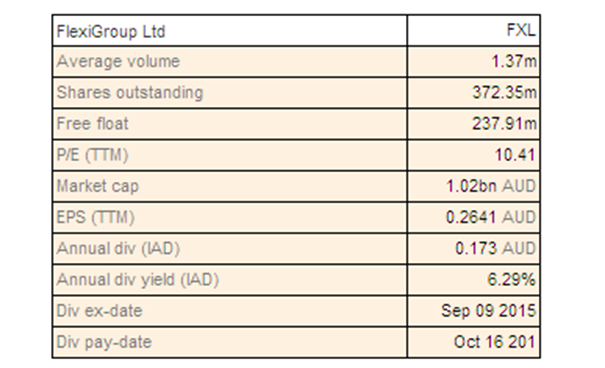

FlexiGroup Ltd

FXL Dividend Details

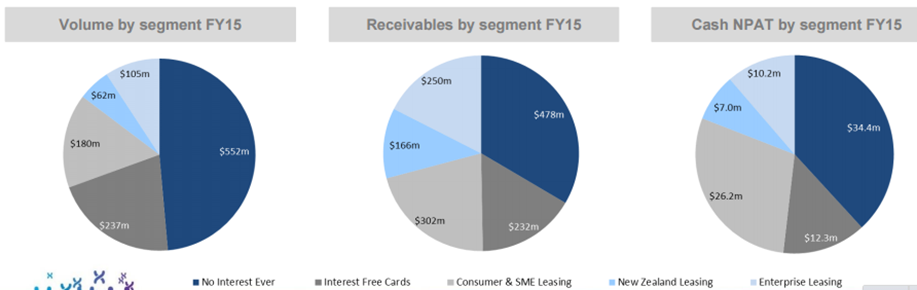

Positive outlook: FlexiGroup Limited (ASX: FXL) shares fell over 21.7% in the last six months (as at November 26, 2015) partly due to unexpected resignation of CEO and the Managing director, Tarek Robbiati coupled with the group’schairman Chris Beare and non-executive director Anne Ward announcing their resignations, raising concerns on the firm performance. On the other hand, FXL reported a decent FY15 performance, with a 6% year on year (yoy) increase of cash NPAT to $90.1 million driven by increase in performance across its Interest Free Cards, New Zealand business and Certegy segments. Volumes and receivables surged by 5% and 8% respectively on a year over year basis. The group’s transaction volume for its Certegy segment improved by 9% yoy to $552 million, while the small and medium enterprise (SME) leasing division was under pressure, delivering 23% yoy decline during the year. FXL issued a positive outlook with Cash NPAT in the range of $92 million - $94 million, for the fiscal year of 2016, while dividends are estimated to be in the range of 50-60% of Cash NPAT. Lower interest rates would continue to drive the demand of its products while its core Certegy business growth would be driven by the better VIP customer program, improved penetration through present retail partners and expansion into new product and merchants. The company has also completed the retail component of its 1 for 4.46 accelerated non-renounceable entitlement offer of new shares announced on October 27, 2015.

FY15 Performance across segments (Source: Company Reports)

FXL is targeting the Education sector in New Zealand Leasing to increase its volumes and also reorganizing the business to focus on broker based origination channels and managed service products, to offset the pressure from the Enterprise Leasing segment. The group recently appointed Symon Brewis Weston as its CEO in order to strengthen its management team.

Moreover, FXL is trading at attractive P/E of about 10x, and has a strong dividend yield of about 6%. We maintain “BUY” recommendation on the stock at the current price of $2.77

.png)

FXL Daily Chart (Source: Thomson Reuters)

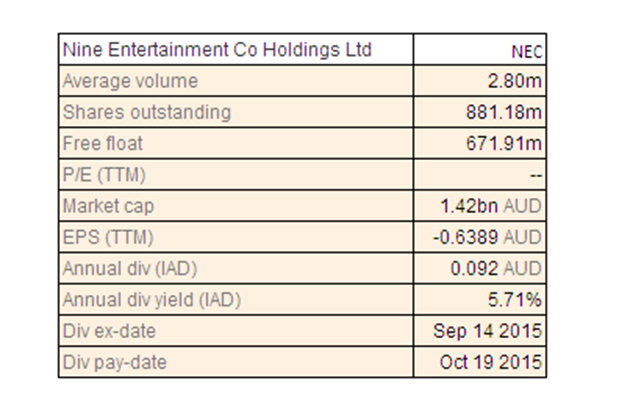

Nine Entertainment Co Holdings Ltd

NEC Dividend Details

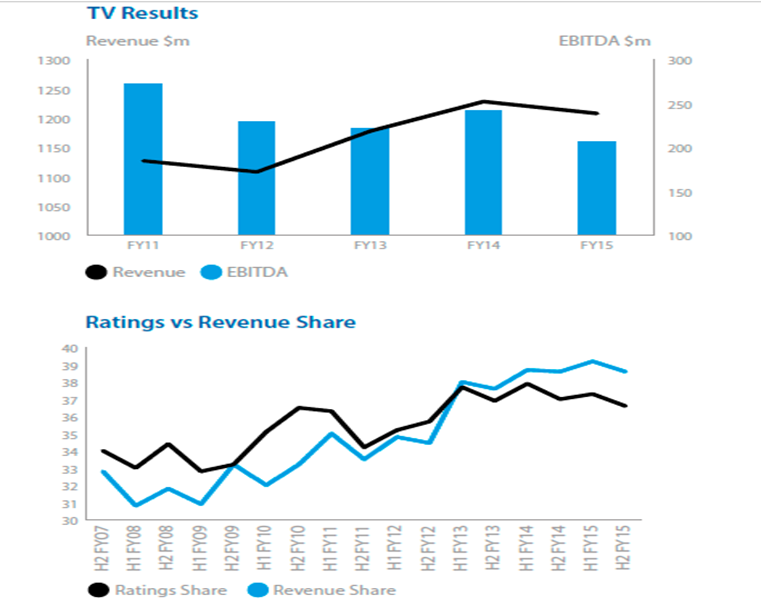

Diversifying business to offset market pressure: Nine Entertainment Co Holdings Ltd (ASX: NEC) shares have surged over 11.03% in the last three months (as at November 26, 2015) as the group reported a better metro revenue share increase of 0.2% to 38.9% during the fiscal year of 2015, despite the overall Metro FTA market lowering by 1.5% during the same period.

TV market performance (Source: Company Reports)

In fact, the stock rose over 3.87% in the last four weeks (as at November 26, 2015) on rumors of a potential merger discussion with Southern Cross Media. But, the group reported that they did not arrive at a final agreement. Meanwhile, NEC is diversifying its business to offset the ongoing pressure of Metro FTA market and accordingly launched Stan (SVOD service) during January 2015. Although NEC’s network division reported a revenue decline of 1.1% yoy to $1,207.9 million in FY15, the group’s digital segment delivered solid performance improving by 33.2% yoy during the period. NEC sold its Nine Live for $640 million and consequently boosted its cash position to $150 million. Nine Entertainment also won the National Rugby League (NRL) broadcast rights which could offer support to the business in the coming periods. As of now, News Corp, NEC and Telstra would deliver $1.8 billion to NRL for securing the game’s future for the long term.

We reiterate our “BUY” recommendation on this 5.7% dividend yield stock at the current market price of $1.62

NEC Daily Chart (Source: Thomson Reuters)

Vita Group Ltd

.png)

VTG Dividend Details

Attractive Opportunity: Vita Group Limited (ASX: VTG) shares rallied over 10.78% (as of November 26, 2015) in just last four weeks boosted by its solid FY15 performance while the group even declared additional special dividends of 2 cents per share apart from its earlier special dividends of 6 cents per share. VTG reported a solid revenue growth of 34% yoy to $601.4 million during fiscal year of 2015, on the back of strong telecom retail performance which improved by 44% yoy to $541.5 million.

.png)

Optimizing portfolio to revamp growth (Source: Company Reports)

The group’s investments in the telecom segment paid off with SMB, Enterprise and Sprout generating an increase of 79%, 60% and 77% respectively while the like for like stores generated 26% increase. Vita opened 5 Telstra stores and 4TBCs leading to 137 points of presence of its telecom retail in FY15. The FY16 outlook seems to be steered by acquisitions and retail network optimisation program. The stock is trading at a cheaper P/E of 10.6x as compared to its peers while VTG has a decent dividend yield of 4.2%.

Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $1.86

VTG Daily Chart (Source: Thomson Reuters)

South32 Ltd

.png)

S32 Details

Ongoing Cost Control Efforts: The shares of South32 Ltd (ASX: S32) plunged by 20% in just last four weeks (as of November 26, 2015) partly impacted by Samancor Manganese fatality pressure and ongoing commodity price volatility. The group’s Samancor Manganese Joint Venture, would be closed till completion of the ongoing strategic review and the management reported that the mining activity might recommence in January 2016. On the other hand, South32 reported a solid Manganese ore production and Silver production increase of 15% and 20% respectively during the first quarter of 2016 as compared to the fourth quarter of 2015. Record production at GEMCO (Australia Manganese) and Illawarra Metallurgical Coal drove the overall quarter’s production performance.

.png)

September quarter production highlights (Source: Company Reports)

The temporary increase in the average ore grade at Cannington boosted silver production. Calciner maintenance completion generated an 11% production rise at Worsley Alumina. Meanwhile, S32 continues to focus on cost efficiency and targets to control costs by at least US$350 million by the end of FY18, while estimates to generate a 25% reduction in the Group and Unallocated costs for FY16. Except South Africa Manganese operations, the group reiterated its FY16 production guidance for all upstream operations.

Investors hunting for long term potential stocks could consider this as an opportunity as we reiterate our “BUY” recommendation on the stock at the current price of $1.225

.png)

S32 Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...