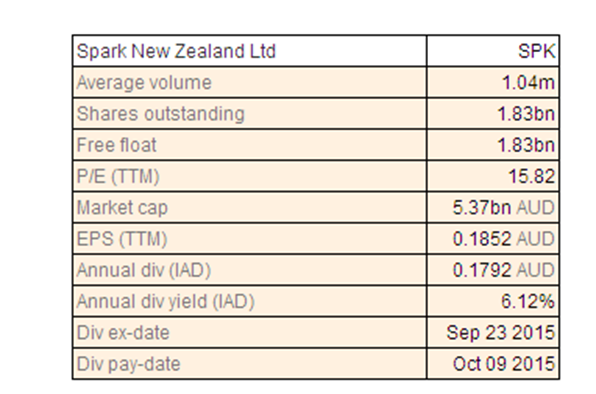

Spark New Zealand Ltd

SPK Dividend Details

Focusing on digital services: Spark New Zealand Ltd (ASX: SPK) acquired Computer Concepts Limited (CCL) for $50 million in an attempt to enhance its cloud services capabilities (acquisition as of now excluded from SPK’s capex guidance). SPK also bought unused radio spectrum (70 MHz block of 2.3 GHz spectrum) from Craig Wireless and Woosh Wireless (NZ) for $9 million. The company also reported that its offering up to $100 million unsecured, unsubordinated fixed rate bonds (Bonds) for institutional as well as New Zealand retail investors, with the ability to accept up to $50,000,000 oversubscriptions. The Bonds are forecasted to have over seven years term and mature by March 2023. SPK’s operating revenues declined by 2.9% year on year (yoy) to $3,531 million in fiscal year of 2015 impacted by continuous fall in calling and access revenues despite solid mobile and IT services revenue growth. But, the group enhanced its net earnings after tax from continuing operations by 16.1% yoy to $375 million driven by its cost control efforts and gain from AAPT sale. SPK is shifting to a digital services retailer from traditional infrastructure based firm and accordingly enhanced its focus on data, mobile and ICT platform services. As a result, SPK launched several products like Revera, Skinny, Bigpip, Lightbox, Qrious big data analytics, Putti apps, and Morepork. Lightbox exceeded the subscriber targets by June 2015 and is witnessing solid growth driven by the rise in average fixed broadband data usage per New Zealand household by 58% during FY15.

Accordingly, SPK’s mobile revenue share surged 40% yoy boosted by solid consumer growth. SPK shares delivered over 11.41% (as of December 04, 2015) increase in the last six months and we believe this positive momentum to continue in the coming months. The group is trading at a P/E of about 16x and has a solid dividend yield of about 6%. We give a “BUY” recommendation on the stock at the current price of $2.92

SPK Daily Chart (Source: Thomson Reuters)

Insurance Australia Group Ltd

.png)

IAG Dividend Details

Revised strategy and issued a positive outlook:Insurance Australia Group Ltd (ASX: IAG) issued a positive outlook for next fiscal year and expects insurance margin to be in the range of 14% to 16%, including a 2% contribution from the Berkshire Hathaway agreement.IAG had been under pressure this year and reported an Insurance profit decline to $1.1 billion in the fiscal year of 2015 against $1.6 billion in the fiscal year of 2014 as the net natural peril claims surged to $1.05 billion in FY15, exceeding the allotted allowance of $700 million for the year by additional $348 million. Therefore, IAG entered into a strategic relationship with Berkshire Hathaway to protect its earnings volatility and capital requirements for the next ten years. This deal would enable IAG to maintain 15% return on equity, as Berkshire Hathaway alliance would reduce IAG’s capital requirement of over $700 million for the next five years, while $400 million of that benefit might be realized by FY16.

.png)

FY15 Financial Summary (Source: Company Reports)

On the other hand, given the tough market conditions in China, the group recently clarified that it would not be making any further investments in China. Meanwhile, Insurance Australia Group stock surged over 13% in the last three months (as of December 04, 2015) and has a decent annual dividend yield of 5.1%. We reiterate our “BUY” recommendation on the stock at the current levels of $5.73

.png)

IAG Daily Chart (Source: Thomson Reuters)

Bank of Queensland Ltd

.png)

BOQ Dividend Details

Focusing on Niche business: Bank of Queensland Ltd (ASX: BOQ) has been building business in niche segments like healthcare, tourism and agribusiness. The bank GLA for healthcare, professional services and agribusiness surged by a CAGR of 243%, 16% and 24% respectively. The bank enhanced its broker share of settlements to 15% in FY15 from 5% in FY14. On the other hand, BOQ is boosting its capital position and recently priced A$550 million of 3.5 year floating rate Notes at a margin of 115 basis points over the 3 month Bank Bill Swap Rate. Earlier, BOQ also raised over $150 million by issuing Wholesale Capital Notes at a margin of 4.35% over the 6 month Bank Bill Swap Rate. The group even enhanced its margins and asset quality during the year as the group’s strategy efforts paid off. BOQ’s cash earnings surged by 19% yoy to $357 million in FY15 while it improved its dividends by 12% leading to a total dividends to 74 cents per share during the year.

.png)

Improving performance (Source: Company Reports)

Meanwhile, BOQ generated a better total return to shareholders of 6.3% in FY15 as compared to group’s peer banks. The stock rallied over 12% in the last three months (as at December 04, 2015) and we maintain our “BUY” recommendation on this 5.5% dividend yield stock at the current price levels of $13.47

BOQ Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.png)

NAB Dividend Details

Offloading non-core assets to boost capital position: National Australia Bank Ltd (ASX: NAB) stock fell over 8.38% (as of December 04, 2015) in the last six months as the group’s earnings were impacted by impairment charges on the back of the UK operations divestments charges, regulatory changes, tough market conditions and ex dividend impact. On the other hand, the bank is focusing on core business and boosting capital position by offloading non-core assets. The group demerged CYBG and even proposed its IPO to institutional investors. NAB proposed a 75% demerger of CYBG to NAB shareholders and a proposed divestment of 25% by IPO to institutional investors. NAB intends to give its shareholders one security in CYBG for every four NAB shares owned. The bank is investing over $300 million in its Wealth business for the next four years and also focusing on customer relationships. NAB even improved its asset quality during fiscal year of 2015, with its total charge for Bad and Doubtful Debts declining by 5% yoy to $823 million on the back of decrease in Australian Banking and UK Banking.The bank’s Common Equity Tier 1 ratio rose by 137 basis points to 10.2% as at September 2015, against March 2015, mainly driven by proceeds from rights issue, on track to comply with the APRA standards.

.png)

National Australia Bank performance (Source: Company Reports)

Nippon Life Insurance might offer a deal in the range of 200 billion and 300 billion yen or US$2.5 billion, to buy National Australia Bank’s insurance operation, which would further boost NAB’s capital position. We maintain our positive stance on NAB given its attractive valuation with a relatively cheaper P/E of about 12x and a solid dividend yield of 6.6%. We reiterate our “BUY” recommendation on the stock at the current stock price of $29.56

.png)

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...