Dick Smith Holdings Ltd

.png)

DSH Dividend Details

Long term potential despite short term hurdles: The shares of Dick Smith Holdings Ltd (ASX: DSH) surged over 15.60% in just last five days (as of November 06, 2015) as the group has been improving its performance, wherein DSH sales rose by 6.9% in the first quarter of 2016 while comp sales improved by 1.3%, driven by better New Zealand business post acquisition. DSH’s online sales also delivered outstanding performance and almost doubled during FY2015, contributing over 8% of retail sales. However, management reported that its Gross profit in 1Q16 would be under pressure impacted by the DSH’s heavy promotions activity and unfavorable product mix. The group is also experiencing a challenging October performance and therefore is cautious on its Christmas trading period outlook. Therefore, DSH decreased its fiscal year of 2016 net profit after tax guidance to the range of $5 million to $8 million. But, DSH intends to grow its network to 420-430 stores by FY2017, by opening over 15 to 20 new stores annually, and improving its private labels penetration, which accounts for more than 12.5% of its FY15 sales. DSH estimates its private labels to be more than 15% of sales by 2017 fiscal year. We believe DSH would deliver better performance in the coming periods.

.png)

Key Initiatives - Small Appliances (Source: Company Reports)

The stock is trading at a very cheap valuation with a P/E of 5.09x while having a solid dividend yield of 14.72%. We remain positive on the stock despite the heavy correction from last few months (fell over 61.19% during this year to date), and give a BUY recommendation at the current price of $0.81

DSH Daily Chart (Source: Thomson Reuters)

AWE Limited

.png)

AWE Details

Enhancing resource potential and cost control efforts: AWE Limited (ASX: AWE) reported a 27% drop in revenues during the third quarter ended on September of 2015 against the second quarter, due to the falling oil prices. The group’s stock fell over 57.96% (as of November 06, 2015) in the last six months impacted by commodity price pressure and slowdown impact in China. On the other hand, the group’s north Perth Basin, Western Australia delivered solid results during the September quarter, and the Waitsia, Senecio, Synaphea and Irwin gas fields gross combined 2P Reserves and 2C Resources improved to 721 Bcf. In fact, flow tests at the second of two target zones in the onshore Waitsia-1 well recorded an output rate of 25.7 million cubic feet of gas per day. This resulted in the total combined flow rate to more than 50 million cubic feet per day. Accordingly AWE has resource potential of >22 years of production at current rates with net 2P Reserves of 114.4 mmboe, and 2C Resources of 121.9 mmboe with the ability to convert most of these assets to 2P within the short to medium term.

.png)

Sales Revenue (Source: Company Reports)

However, AWE reported a 3% production decrease to 1.38 mmboe in third quarter of 2015 against the earlier quarter, but BassGas production generated 23% increase driven by the Yolla-5 and 6 development wells while Sugarloaf production rose 7% as over 20 wells (gross) were brought onto production. Meanwhile, AWE’s cost cutting initiatives also paid off during the quarter and was able to decrease Field opex by 21% and cut overall investment expenditure (exploration and development) by 29%. The group sold its non-core assets by divesting its 57.5% interest in the Cliff Head oil project to Elixir Petroleum. We believe investors need to leverage the recent correction as an opportunity to enter the stock, given the group’s long term potential. Accordingly, we put a BUY on AWE at the current market price of $0.655

AWE Daily Chart (Source: Thomson Reuters)

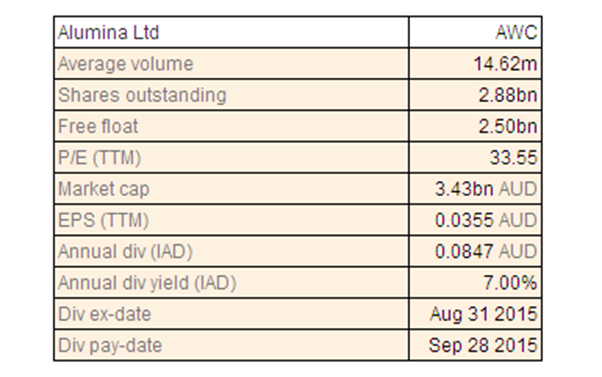

Alumina Ltd

AWC Dividend Details

Improving Costs : Alumina Limited (ASX: AWC) made partnership (60% interest) with Alcoa (40% interest) to form AWAC, a major bauxite miner in the world with Cost curve position in the first quartile. AWAC delivered a dividend of USD 34.6 million to Alumina since the end of the third quarter of 2015. AWAC’s average realized price of alumina surged by $21 per tonne while AWAC cash from operations went up by $239 million to $321 million during the first half of 2015. Meanwhile, Alumina enhanced its net profit after tax of US$122 million in the first half of fiscal 2015 driven by productivity gains, against the net loss of US$47 million in the corresponding period of last year. The group forecasts a better long term growth with the global aluminum demand estimated to rise at a CAGR of 4.3% during the 2014 to 2024 period, driven by the electricity transmission in China and transport in China and RoW. Moreover, recently Alcoa announced its plans to separate its upstream business and launch two standalone companies, which might open opportunities for Alumina for entering into deals. AWC stock corrected over 31.64% in the last six months (as at November 06, 2015) impacted by highly volatile commodity prices. Nonetheless, AWC rose about 3.42% in the last one month and has long term potential with an attractive dividend yield of 6.99%. The stock offers an attractive investment opportunity for long term investors, and we reiterate our BUY recommendation on the stock at the current price of $1.19

AWC Daily Chart (Source: Thomson Reuters)

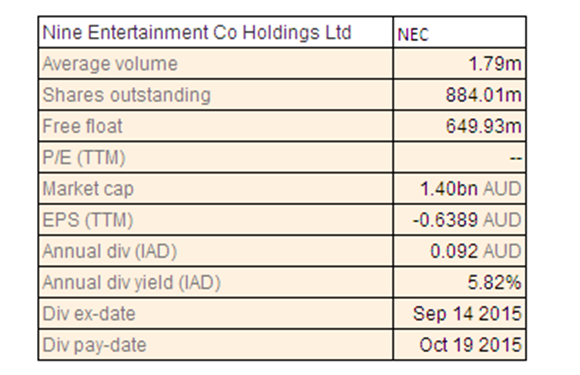

Nine Entertainment Co Holdings Ltd

NEC Dividend Details

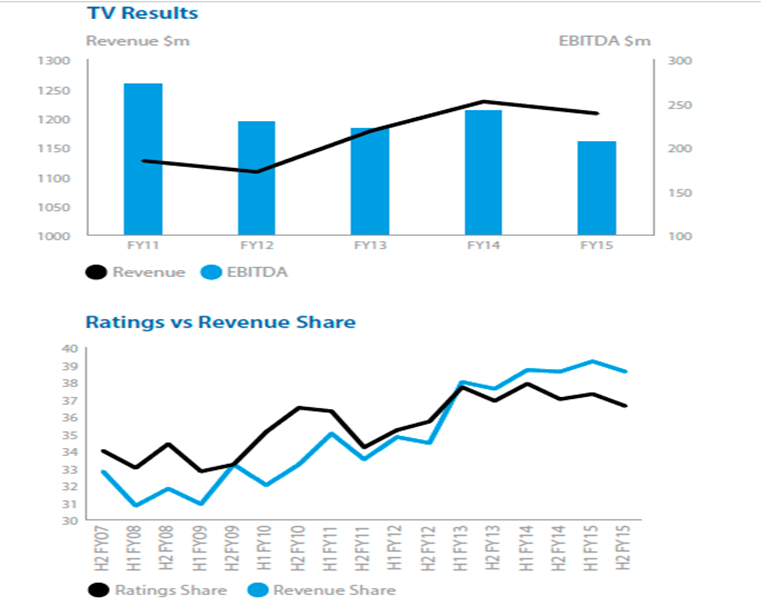

Enhanced FTA market share and cash position: Nine Entertainment Co Holdings Ltd (ASX: NEC) improved its metro revenue share slightly by 0.2% to 38.9% during the fiscal year of 2015, despite the overall Metro FTA market lowering by 1.5% during the same period. NEC is diversifying its business and the group’s Stan (SVOD service) launch during January 2015 is performing on track with expectations. Although NEC’s network division reported a revenue decline of 1.1% yoy to $1,207.9 million in FY15, the group’s digital segment delivered solid performance improving by 33.2% yoy during the period. NEC sold its Nine Live for $640 million with which the group’s cash position enhanced to $150 million. NEC also improved its operating free cash flow conversion by 16 basis points to 103% during the fiscal year of 2015, and accordingly NEC enhanced its dividends per Share to 9.2 cents in FY15 from 4.2 cents in FY14.

TV market performance (Source: Company Reports)

Nine Entertainment seems to have a dominating position in the TV market boosted by its win of National Rugby League (NRL) broadcast rights and other programs. Positive indications also come from the new chief executive, Hugh Marks who views NEC leading the innovation for premium content business. With the shares correcting over 30.70% in the last six months (as at November 06, 2015), we view this an opportunity to enter this 5.82% dividend yield stock and accordingly give a BUY recommendation at the current market price of $1.545

.png)

NEC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...