Four big rises of last fiscal year

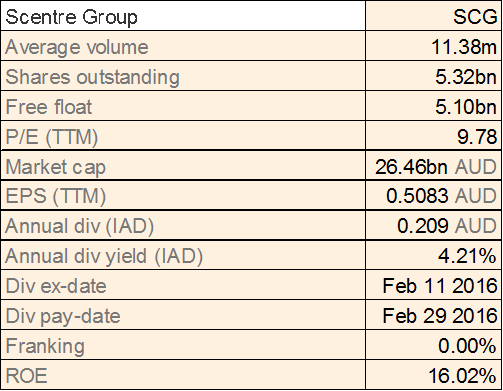

Scentre Group

SCG Details

Redemption of Notes: Scentre Group (ASX: SCG) has agreed with PGGM Private Real Estate Fund to redeem approximately $600 million of the $1.2 billion Property Linked Notes that it holds and to extend the review dates of the remaining notes totaling almost $555 million. Meanwhile, for CY 2015, SCG’s fund from operation grew 3.8% to $1.19 billion which was above the company’s estimates. The stock has risen about 28% in the last fiscal year (as of June 30, 2016).

The company could have achieved growth of 5% if there was no dilutionary impact of asset sales during the year. SCG is deploying $3 billion for the major redevelopments. In addition, SCG has a decent dividend yield, and is trading at cheap P/E. We give a “Hold” recommendation on the stock at the current price of $5.03

SCG Daily Chart (Source: Thomson Reuters)

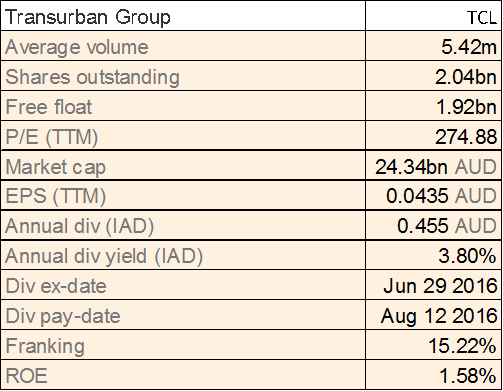

Transurban Group

TCL Details

Partnering with Brisbane City Council: Transurban Group (ASX: TCL) stock surged over 23% (as of June 30, 2016) in the last one year. The group recently reported that they would partner with Brisbane City Council through Transurban Queensland for the upgradation project of Inner City Bypass (ICB) for $80 million. Meanwhile, Transurban Queensland is raising fund of CHF 200 million (A$280 million) in the Swiss market by issuing senior secured 7 year notes. The proceeds would be swapped into fixed Australian dollars and used to repay existing term bank debt due to mature in July 2017. TCL has already raised $460 million via new non-recourse debt facilities, with a weighted average tenor of over 9 years for the financing of Lane Cove Tunnel Project.

In addition, TCL is distributing totaling 23.0 cents per stapled security for the six months ending on June 30, 2016, leading to full FY2016 distribution to 45.5 cents per stapled security of which 7.0 cents will be fully franked. On the other hand, we believe that the stock is trading at higher valuations with an unreasonable P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $12.11

TCL Daily Chart (Source: Thomson Reuters)

CSL Limited

.png)

CSL Details

Approval for Influenza Vaccine: CSL Limited (ASX: CSL) has got approval from US Food and Drug Administration for the Influenza Vaccine FLUCELVAX QUADRIVALENT against the A viruses and B viruses which would further broaden their influenza coverage. CSL has been granted seven years of marketing exclusivity in March 2016 by the U.S. Food and Drug Administration for IDELVION. CSL has completed the acquisition of

Novartis' influenza vaccine business, and integrated the subsidiary, bioCSL, to create Seqirus, the second largest influenza vaccine business in the US$4 billion global industry. Accordingly, the stock has risen over 28% in the last one year (as of June 30, 2016). The company is also running its on market buy-back program. CSL is trading at a high P/E. Given the stock fundamentals, we believe CSL is “Expensive” at the current price of $112.40

CSL Daily Chart (Source: Thomson Reuters)

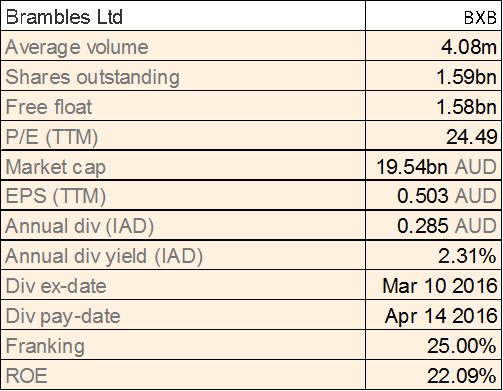

Brambles Limited

BXB Details

Divested LeanLogistics business: Brambles Limited (ASX: BXB) has completed the sales of LeanLogistics business to Kewill for US$115 million which would lead to a pre-tax gain of US$53M in FY16 accounts. Meanwhile, BXB has reaffirmed the expected sales revenue and underlying profit growth at constant forex to be in the range of 8% to 10% for FY 16 and expects underlying profit for FY 16 to be in the range of US$1,015-1,035M.

.png)

Financial Performance (Source: Company Reports)

BXB has surged about 18% in the last fiscal year (as of June 30, 2016) while Brexit impact is anticipated on its performance to some extent. With the stock also trading at high P/E, we give an “Expensive” recommendation on the stock at the current price of $12.46

BXB Daily Chart (Source: Thomson Reuters)

Four big falls of last fiscal year

Woodside Petroleum Limited

.png)

WPL Details

Increase of Exploration Potential: Woodside Petroleum Limited (ASX: WPL) plunged about 23% in last fiscal year (as at June 30, 2016) but reported increase in exploration potential in the estimate of contingent resource by 83 MMboe to 4,481 MMboe of the two offshore gas discoveries of Myanmar in Q1 2016 recently. The company has achieved an annualized loaded LNG production rate equivalent of 4.8 mtpa at Pluto LNG (100% project) which is more than expected annual production capacity of 4.3 mtpa. WPL’s JV Greater Enfield project with Mitsui E&P Australia has also been approved for development.

.png)

Expansion Plan (Source: Company Reports)

Woodside Energy Trading Singapore Pte Ltd had also signed a Heads of Agreement (HOA) with PT Pertamina (Persero) for the supply of approximately 0.5 to 1.0 million tonnes of LNG per annum from Woodside’s LNG portfolio for a period of 15 to 20 years (commencing in 2019). Moreover,

Woodside’s exploration of four to seven wells is expected to start in early 2017. The company's 2017 drilling program off Myanmar would accelerate options for commercialization. We maintain our “Buy” recommendation on the stock, at the current price of $26.79

WPL Daily Chart (Source: Thomson Reuters)

Woolworths Limited

.png)

WOW Details

Struggling with credit ratings but planned potential reinvestments: Woolworths Limited (ASX: WOW) stock has fallen 24% in the last one year (as of June 30, 2016) due to challenges faced by the group like heavy restructuring costs, management changes, credit rating downgrade from BBB+ (Outlook Negative) to BBB (Outlook Stable) by Standard and Poor, weak third quarter financials and rising competition. However, WOW is rebuilding and reinvesting in their business with an additional $150 million to be invested in H2 16 on price, service and loyalty in Australian Supermarkets.

In addition, WOW has started the implementation of a new group operating model which is designed to reduce costs, increase the business accountability and improve shared service delivery effectiveness. Having a good dividend yield, we believe the stock offers potential for long term investors and we reiterate our “Buy” recommendation on the stock at the current price of $20.82

WOW Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Details

Expansion Efforts: Australia and New Zealand Banking Group Ltd (ASX: ANZ) reported that the bank would consolidate dividend payout ratio within the range of 60-65 percent of annual cash profit, from prior 65-70 percent and is expecting improved financial outcomes from institutional in future periods. Meanwhile, the bank stock was under pressure this year and fell over 27% during last fiscal year (as of June 30, 2016) given bank’s first half of 2016 weak performance as there was 22% fall in profit to $2.7 billion. But, ANZ is focusing on its consumer and small business franchises and is expanding at New South Wales in Australia, while focusing on long term growth in Asia despite short term hurdles. The bank has a strong dividend yield and is trading at attractive P/E.

The bank has paid interim dividends as 80 cents franked at 30% on July 01, 2016, which is 7% lower than that paid in first half of 2015. Despite short term pressure given Brexit outcome and Australia’s political scenario, we maintain our “Buy” on the stock at the current price of $23.75

.PNG)

ANZ Daily Chart (Source: Thomson Reuters)

BHP Billiton Limited

.png)

BHP Details

Investments in Exploration to increase: BHP Billiton Limited (ASX: BHP) has fallen about 32% in last fiscal year (as at June 30, 2016) and has been issued an interim order by the Superior Court of Justice in Brazil to suspend the decision of the Federal Court of Appeal to ratify the Framework Agreement related to Samarco. The effect of this interim order of the Superior Court of Justice is to reinstate the BRL20 billion public civil claim made by the Brazilian Authorities against Samarco, Vale and BHP Billiton Brasil. BHP has shown intentions to appeal the decision. Given the fundamentals, BHP is expected to withstand the pressures related to Samarco event. For the next financial year, the company would invest approximately US$900 million dollars in exploration, which represents 18 per cent of their overall capital budget.

.png)

Controlling Capex (Source: Company Reports)

In addition, BHP is targeting deep water oil in the Gulf of Mexico, Caribbean and Western Australia and for copper exploration program.

Meanwhile, BHP has outlined the path for its Coal business to improve returns by unlocking productivity, reducing costs and releasing latent capacity. Having a decent dividend yield and fundamentals, we maintain “BUY” recommendation on the stock at the current price of $19.53

.PNG)

BHP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...