TPG Telecom Ltd

.PNG)

TPM Details

Debt is expected to increase in FY 17: TPG Telecom Ltd (ASX: TPM) reported a 69% increase in the Net Profit After Tax (NPAT) of $379.6m in FY 16 and a 61% increase in the earnings per share to 45.3 cents per share. Moreover, TPM expects the underlying EBITDA for the group to be in the range of $820m to $830m in fiscal year of 2017, excluding any impact from potential operations in Singapore and the capital expenditure is expected to be range of $370m to $420m.

.png)

FY 16 Financial Performance (Source: Company Reports)

The guidance for capex in FY 17 includes the $72m for 1800 MHz spectrum, $50m for committed international capacity purchases (SX & SEA-US) and substantial fibre rollout capex. In addition, TPG has a bank debt of $1,350m and a net debt to EBITDA leverage ratio of about 1.8x at the end of the FY 16 ending 31st July 2016. TPM stock has fallen 42.81% (as of November 22, 2016) in the last three months due to struggling core business coupled with rising debt and capex concerns. The group will hold its AGM on December 07, 2016. We give an “Expensive” recommendation on the stock at the current price of – $ 7.20

.png)

TPM Daily Chart (Source: Thomson Reuters)

Vocus Communications Limited

.PNG)

VOC Details

Completion of Nextgen Acquisition: Vocus Communications Limited (ASX: VOC) has completed the acquisition of Nextgen and two development projects, the Australian Singapore Cable and the North West Cable System for $806.7 million as upfront consideration and $54 m as deferred consideration. VOC had planned to expand its connection points to the NBN from 68 to 112 of a possible 121 nationwide NBN points of interconnect (POIs). Moreover, VOC is completing the integration of the Amcom business with the synergies target of $13-15 million, expected to be achieved by the end of FY17. The merger with the M2 business is also proceeding with all integration milestones being met and the $40 million synergy target is on track to be completed by the end of FY18. On the other hand, VOC has announced the resignation of James Spenceley and Tony Grist as two of its board members. The resignations are after a difference of opinion between the Departing Directors and the Board on an alternative leadership framework. Moreover, VOC stock has fallen 42.21% (as of November 22, 2016) in the last six months while being up about 3% on November 23, 2016, and still the stock is trading at a high P/E. The group will hold its AGM on November 29, 2016. We give an “Expensive” recommendation on the stock at the current price of – $ 5.41

VOC Daily Chart (Source: Thomson Reuters)

Telstra Corporation Ltd

.PNG)

TLS Details

Rising capital expenditure: Telstra Corporation Ltd (ASX: TLS) has given the detail about the $3 billion incremental capital expenditure, a commitment to expand its productivity target to at least $1 billion over the next five years, and a review of the company’s capital allocation strategy. The $3 billion expenditure will entail use of more than $1.5 billion in building networks for the future, around $1 billion in accelerating the digitization of the business and up to $500 million in other customer experience related improvements. TLS is expecting to reduce the net underlying core fixed costs by over $1 billion by FY21. Additionally, TLS has reported 6.3% growth in revenues to $28.3 billion in FY 16 and 36% growth in the net profit to $5.8 billion including $1.8 billion from sale of Autohome shares against FY 15. TLS’s outlook entails ‘mid to high’ single digit revenue growth, and ‘low to mid’ single digit EBITDA growth in 2017, indicating some weakness. Meanwhile, TLS stock has fallen 13.43% in six months as on November 22, 2016. Given the prospects, we maintain an “Expensive” recommendation on the stock at the current price of – $ 5.00

.png)

TLS Daily Chart (Source: Thomson Reuters)

Macquarie Telecom Group Ltd

.PNG)

MAQ Details

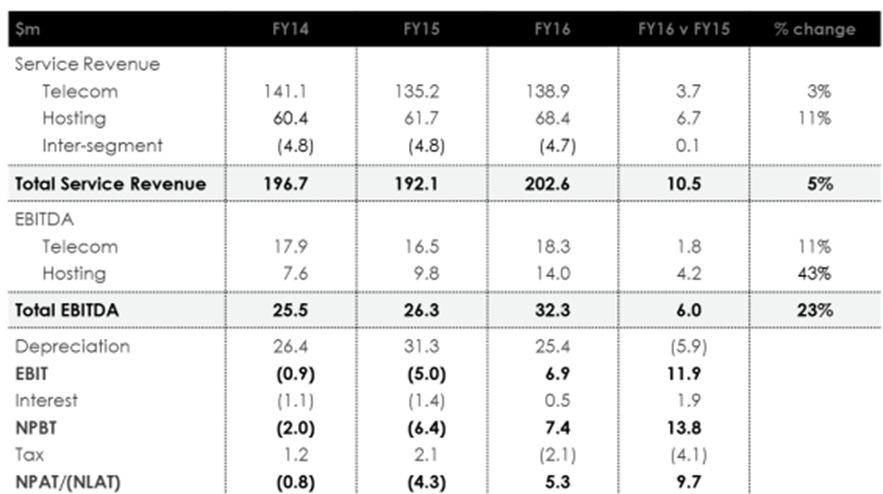

Higher valuations: Macquarie Telecom Group Ltd (ASX: MAQ) reported a 5% growth in the total service revenue in FY 16 and a 223% growth in NPAT. MAQ also reported a 23% growth in the EBITDA as compared to FY 15. Moreover, EBITDA profit for the first half of FY17 is expected to be between $17.0 million to $19.0 million, up from $15.6 million in the previous corresponding period.

FY 16 Financial Performance (Source: Company Reports)

The expected capex is $21 to $23 million. MAQ stock has fallen 13.39% in three months as on November 22, 2016 due to concerns over volatile market conditions while trading at an unreasonable P/E. We give an “Expensive” recommendation on the stock at the current price of – $ 11.00

MAQ Daily Chart (Source: Thomson Reuters)

Hutchison Telecommunications (Australia) Limited

HTA Details

Weak bottom line performance: Hutchison Telecommunications (Aus) Ltd (ASX: HTA) in 1H 2016 has reported the statutory net loss of $65.7 million, representing a $24.4 million improvement in the $90.1 million net loss in the corresponding period of 2015. HTA’s revenue from ordinary activities consists of the interest income received on loans to VHA and has increased 46.4 per cent to $3.6 million as a result of increased shareholder loans provided to VHA in first and second quarters of 2015.

.png)

Financial Performance (Source: Company Reports)

Meanwhile, no dividend was declared or paid by HTA during the half-year 2016. But given the bottom line pressure, we give an “Expensive” recommendation on the stock at the current price of – $ 0.07

HTA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations

AU

AU

Please wait processing your request...

Please wait processing your request...