Ainsworth Game Technology Ltd

.PNG)

AGI Details

Second half of FY 17 expected to be stronger than the first half: Ainsworth Game Technology Ltd (ASX: AGI) stock has fallen 9.6% in the last three months as on January 06, 2017 due to weak first half of 2017 projections. The unit volume will reduce 30% in 1H FY17 as compared to 1H FY16 due to challenging industry conditions in domestic market while positive outcome is expected from international markets. Additionally, the normalized pre-tax profit, excluding currency gains, for 1H FY17 is expected to be $15 million. But, AGI is expecting stronger second half with significant improvement in profits in the second half as compared to 2H FY16.

.png)

Financial Performance (Source: Company Reports)

AGI sales revenue has increased by 19% to $285.5m for FY16 versus the prior corresponding period. Moreover, AGI’s acquisition of Nova and a Class II product offering has enabled the company to leverage the technology allowing greater access to new markets in the Americas. AGI has reported 68% of segment profits from the Americas. AGI stock is trading at an attractive P/E. Given the mixed sentiments, we give a “Hold” recommendation on the stock at the current price of – $ 2.04

.png)

AGI Daily Chart (Source: Thomson Reuters)

Baby Bunting Group Ltd

.PNG)

BBN Details

Moderate performance expected in FY17: Baby Bunting Group Ltd (ASX: BBN) has reported a 31.4% growth in sales for FY16 to $236.8 million while pro forma EBITDA rose 51.1% to $18.7 million in FY 16 as compared to FY 15. BBN has exceeded the FY16 prospectus forecasts. Moreover, BBN has opened five new stores thereby the comparable store sales grew 12.5%. BBN’s pro forma net profit after tax (NPAT) grew 55.8% against the prior corresponding period. BBN has planned four to eight new store openings in FY 17. Four new store leases have been signed and the stores are expected to open before February 2017. On the other hand, BBN is expecting a slightly slower growth rate for EBITDA in FY 17 and forecasting a range of $21.5 million to $24.5 million, representing a growth in the range of 15% to 31%. The year to date sales growth has been 20.3% at November 13, 2016. Moreover, BBN stock is trading at a high P/E. We give an “Expensive” recommendation on the stock at the current price of – $ 2.39

BBN Daily Chart (Source: Thomson Reuters)

Cash Converters International Ltd

.PNG)

CCV Details

Not in favor of final report of the SACC Law Review recommendation: Cash Converters International Ltd (ASX: CCV) stock has fallen 12.05% in the last six months (as on January 06, 2017). CCV has reported a 30% drop in lending volumes in the first quarter of FY 17. Moreover, CCV reported that they are not supporting recommendations of the Final Report of the SACC Law Review as it caps a customer’s loan repayments as a percentage of the net income of 10%. This review would also hurt over 500,000 CCV customers who access the short-term Cash Advances (six-week loans). However, the government is intending to develop this legislation during 2017, subject to its other legislative priorities, which means that the impact of these changes would not occur until at least 2018.

.png)

FY17 First quarter performance (Source: Company Reports)

The group reconfirmed the full year NPAT guidance of $20 million to $23 million and reported net profit for first quarter FY17 in line with the earlier forecast. On the other hand, we believe the stock fall offers a good opportunity. We give a “Buy” recommendation on the stock at the current price of – $ 0.36

.png)

CCV Daily Chart (Source: Thomson Reuters)

Coca-Cola Amatil Ltd

.PNG)

CCL Details

Targeting mid-single digit earnings per share growth: Coca-Cola Amatil Ltd (ASX: CCL) has appointed Mark G. Johnson as its new Director. The stock has risen 20.7% in the last six months as on January 06, 2017. For the first half of 2016, CCL had reported about 3% growth in the total revenue to $2517.1 million and a 7.8% growth in the profit to $198.2 million.

.png)

1H 16 Financial Performance (Source: Company Reports)

Moreover, CCL is targeting mid-single digit earnings per share (EPS) growth in the medium term as the EPS grew 7.8% to 26 cents in the 1H 2016. The group has plans to introduce incidence pricing in 2017 in Australia for better economic alignment between pack sizes. CCL expects to have $50 million of restructuring costs and $75 million of capex in 2017. CCL’s property division was also said to be setting up in January 2017. We maintain a “Hold” recommendation on the stock at the current price of – $ 10.31

.png)

CCL Daily Chart (Source: Thomson Reuters)

Dicker Data Ltd

.PNG)

DDR Details

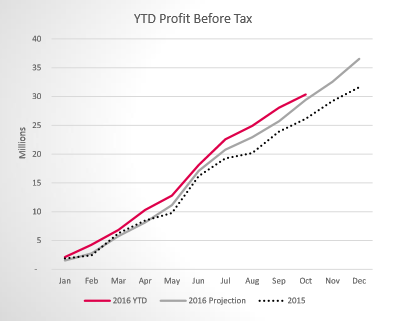

Appointed as a distributor for Lenovo: Dicker Data Ltd (ASX: DDR) has signed the agreement with Lenovo New Zealand and is appointed as a distributor for the New Zealand market. For 10 months of 2016, DDR has reported the revenue growth of 9.6% and forecasts that this growth rate would be sustained for the rest of FY16.

Guidance for Profit before Tax (Source: Company Reports)

DDR expects to achieve a pre-tax operating profit of $36.5 million for FY16 and NPAT is expected to grow 16% to $25.5 million. DDR has a solid dividend yield and a high ROE. The stock has risen over 28.98% in the last six months as on January 06, 2017. We give a “Hold” recommendation on the stock at the current price of – $ 2.25

.png)

DDR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...