G8 Education Ltd

.png)

GEM Details

Decent 1H FY16 results: G8 Education Ltd (ASX: GEM) in the first half 2016 reported a 16.2% growth in the revenue mainly due to increase in fees and acquisitions. But, the underlying EBIT rose only 8.5% due to an additional ratio related headcount impacting the Q1 wages, with significantly improved performance in Q2. The investment in staff training and centre refurbishment, is substantially offset by savings in other areas.

.png)

1H 2016 Financial Performance (Source: Company Reports)

GEM has total licensed places to 37,045 as on 30th June 2016 and is expecting to settle a further 12 centers for $32.0m in H2, with these purchases being funded by internal operating cash flow. Meanwhile, the stock has fallen 18.8% in the last four weeks (as of August 29, 2016). We maintain our “Buy” recommendation on the stock at the current price of $3.12

GEM Daily Chart (Source: Thomson Reuters)

Navitas Limited

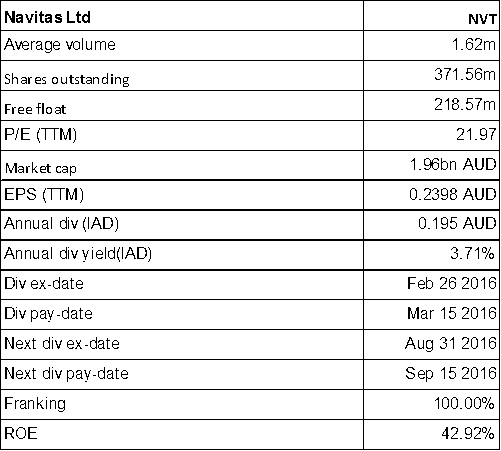

NVT Details

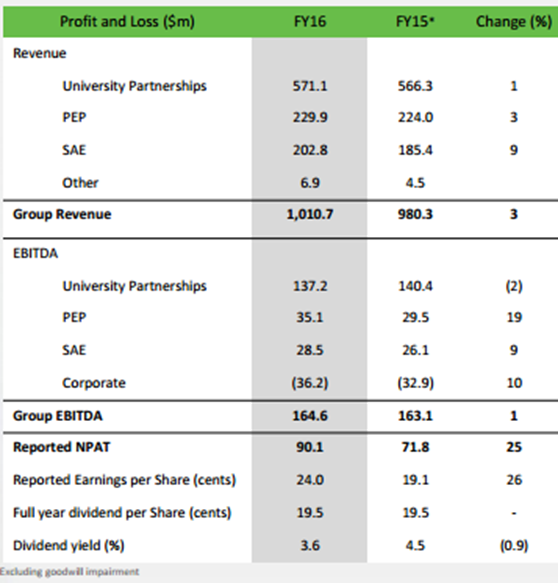

Solid bottom line growth: Navitas Limited (ASX: NVT) has renewed the Eynesbury contract with the University of Adelaide for five years to 2021. NVT recently reported a revenue growth of 3% to $1,010.7m for FY 16 but the net profit after tax delivered an even more solid growth of 25% to $90.1m. In FY 16, NVT had a significant internal restructuring to better position the company for long term growth.

FY 16 Financial Performance (Source: Company Reports)

The University Partnerships Division was reorganized to operate under three core regions like Australasia, North America and Europe. The global Learning and Teaching function was created to drive academic innovation while created shared service centers for core support services like Finance, IT and HR.

Moreover, NVT expects FY17 EBITDA to remain broadly in line with the FY16 result, taking into account the solid underlying organic revenue growth in core markets and the final financial impact of closing colleges in Australia in H1 FY17. Meanwhile, the stock has risen 12.37% in the last six months (as of August 29, 2016). We give a “Hold” recommendation on the stock at the current price of $5.30

NVT Daily Chart (Source: Thomson Reuters)

3P Learning Limited

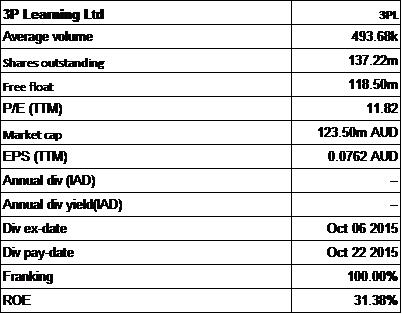

3PL Details

Impact on EBITDA:3P Learning Ltd (ASX: 3PL) reported FY16 results with underlying core EBITDA down 21% to $13.3m at the back of investments in North America, products and global support. The revenue witnessed 10% growth to $49.3m, which is just above the expected range of $48.0m to $49.0m (7% to 9% year on year). This came at the back of support from growth in all the regions. However, the company’s net interest expense went up owing to the strategic investment in Learnosity. 3PL had a new CEO & Managing Director from 1

st June, 2016.

Meanwhile, 3PL stock has fallen 36.2% in the last six months (as of August 29, 2016), and still trading at a high P/E. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $0.96

3PL Daily Chart (Source: Thomson Reuters)

Ashley Services Group Ltd

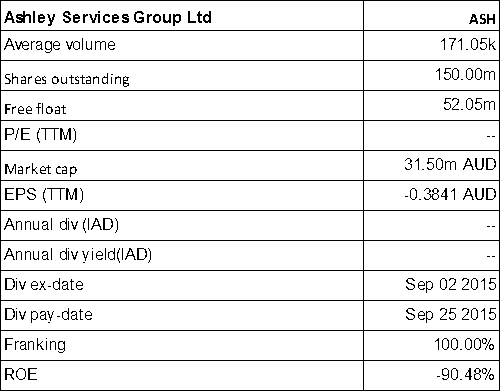

ASH Details

Weak results and Legal Proceedings against Vendor of Integracom:Ashley Services Group Ltd (ASX: ASH) has advised that 90,024,096 ordinary shares that were previously subject to voluntary escrow were released on 21

st August 2016. Moreover, there are legal proceedings filed in the Supreme Court of New South Wales against Holmes Management Group Pty Limited (Holmes), the vendor of the Integracom telecommunications training business acquired by ASH in August 2014. These proceedings relate to alleged breaches of warranties under the Unit Sale and Purchase Agreement for the acquisition.

The full year statutory results also remained weak with a slip of 7.6% in total revenue to $281m over prior corresponding period while the loss per share was of the order of 44.7 cents. Moreover, the statutory loss after income tax was $67m against $13.1m profit in FY 15. We give an “Expensive” recommendation on the stock at the current price of $0.20

ASH Daily Chart (Source: Thomson Reuters)

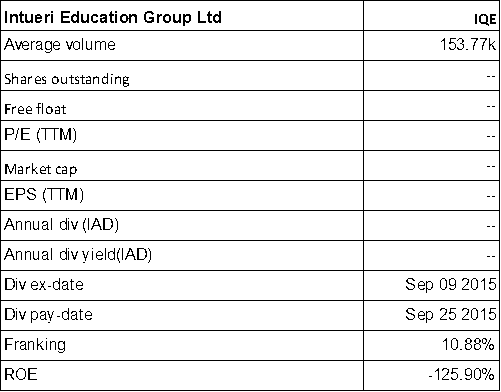

Intueri Education Group Ltd

IQE Details

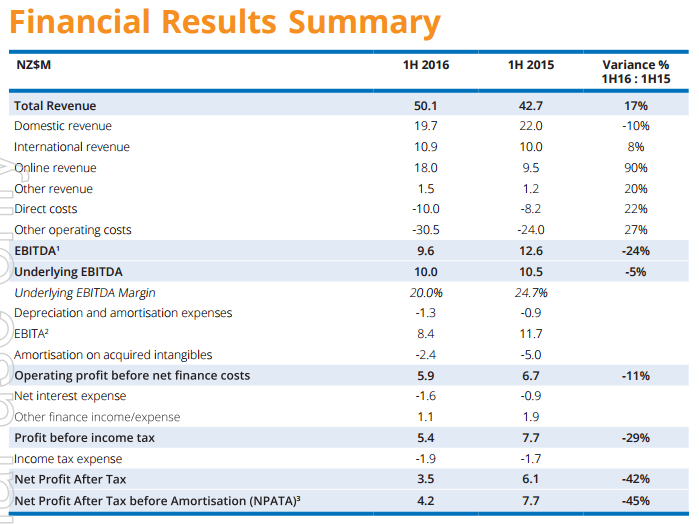

Weak guidance: Intueri Education Group Ltd (ASX: IQE) reported for 17% surge in total revenue in 1H 2016 over 1H 2015. However, underlying EBITDA fell to $10.0 million as compared to 1H15 of $10.5 million.

Result Summary (Source: Company Reports)

Moreover, the second half year is expected to be softer due to phasing of Australian Online revenue and slowing demand in International segment, while the full year EBITDA guidance is over $15 million, subject to receiving confirmation of final 2016 Vet Fee-Help funding cap. The stock has already fallen 14.29% in the last three months (as of August 29, 2016) and still we feel there is more downside. We give an “Expensive” recommendation on the stock at the current price of $0.29

IQE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...