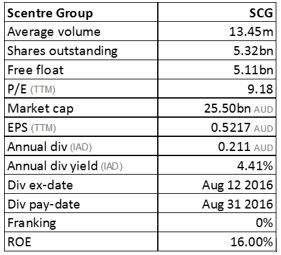

Scentre Group Ltd

SCG Details

Outlines good development pipeline: Scentre Group Ltd (ASX: SCG) enhanced its stake in Carindale to 52.8%. The group also put Auckland’s Westfield WestCity up for sale and expected to fetch up to $175 million. By selling the shopping centre, the group is reducing its exposure to New Zealand. In November last year, the group had sold 3 Westfield malls for $549 million. On the other side, the group divested $2.3 billion of assets that did not meet the group’s long-term strategy. Moreover, SCG jointly with Cbus Property has purchased the David Jones Market Street building in Sydney’s CBD for $360 million wherein the group’s share is $182.5 million.

.jpg)

Major developments (Source: Company Reports)

David Jones would continue to occupy the property till 2019 under lease agreements providing 4.5% rental return on acquisition price. Totally the company acquired $1.1 billion of high quality CBD and regional shopping centers.

The group’s over 80% of portfolio generates annual sales in excess of $500 million and over 70% of portfolio generates average specialty sales productivity in excess $10,000 per square meter. We recommend a “Hold” at the current market price of - $4.74

.PNG)

SCG Daily Chart (Source: Thomson Reuters)

Arena REIT No. 1

ARF Details

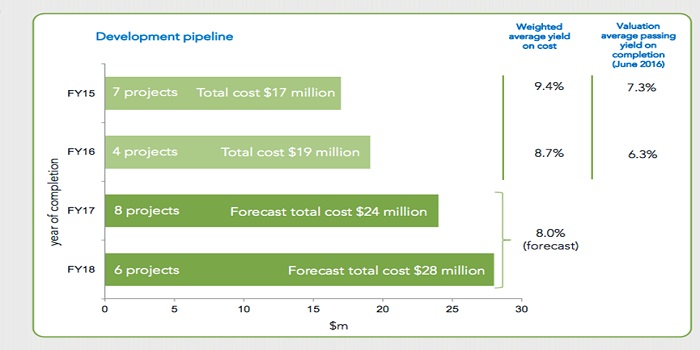

Project pipeline and dividend guidance: Arena REIT No. 1 (ASX: ARF) announced a distribution guidance of $0.117 per security for its fiscal 2017, representing a 7.4% rise over the $0.109 per security paid in 2016. For FY16, ARF generated an operating profit of $25.6 million, up 16% on a year on year (yoy) basis while statutory net profit was at $72.6 million, rising by 19% as compared to the prior corresponding periods.

Development Pipeline (Source: Company Reports)

The improvement was driven by $51.1 million increase in property valuation across Arena’s portfolio. Arena completed four development projects in FY16 at total costs of $19.1 million. The company has 14 projects in its development pipelines worth $52 million with all leases pre-commitment in place. The growth in rental income drove EPS by 9% in FY16. ARF payout ratio was stable at 98% distributing 10.9 cents per security.

After touching high in August, the stock is in correction mode for last one month and fell over 5.56% (as of September 28, 2016). We recommend a “Hold” at the current market price of - $1.97

.PNG)

ARF Daily Chart (Source: Thomson Reuters)

Charter Hall Retail REIT

CQR Details

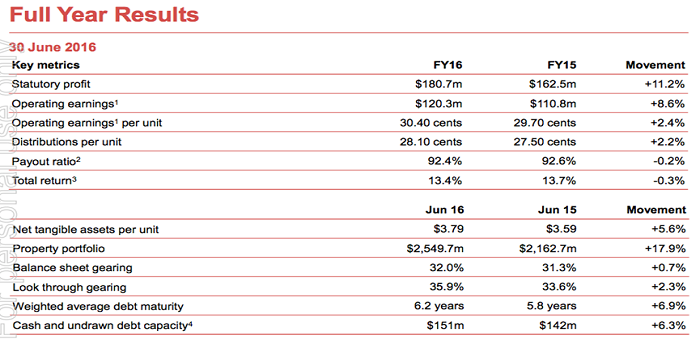

Acquisition and rise in portfolio:Charter Hall Retail REIT (ASX: CQR) completed an overall acquisition of $228 million in FY16 and registered a 17.9% rise in portfolio value to $2.55 billion. Occupancy rate was stable at 98%.

FY16 Annual result (Source: Company Reports)

The company is recycling its capital from non-core properties to larger, higher growth properties and has disposed-off two non-core properties for $20.3 million at a yield of 6.5%. Wesfarmers and Woolworths are their top tenants representing 50.7% of base rent.

The company declared a dividend of 14 cents per share. We recommend a “HOLD” on the stock at the current market price of - $4.22

.PNG)

CQR Daily Chart (Source: Thomson Reuters)

National Storage REIT

NSR Details

Acquisition of $630 million portfolio:National Storage REIT (ASX: NSR) reported that its affiliates trust has formed joint venture with major state pension fund to acquire the 66 property portfolio of iStorage for $630 million approx. The portfolio contains about 4.5 million square feet of rentable space in over 36,000 storage units across 12 states and 24 markets with occupancy rate of 86%. In June, the company inks $190 million for 29 properties in six states. It is also acquiring Kurnell and Moonah Central for total purchase consideration of about $20.75 million. The company raised $260 million to fund the acquisitions. For FY16, overall revenue increased 25% to 79.8 million and underlying earnings was at $29.2 million, up 20% on FY15. EPS was at 8.7 CPS. For FY17, the management guided underlying earnings of $45.5 - $46.5 million delivering EPS growth in the range of 5.8% - 8% on FY16.

The company declared a dividend of 4.4 cents per share for FY16. We rate the stock as a “Speculative Buy” at the current market price of - $1.61

NSR Daily Chart (Source: Thomson Reuters)

Stockland Corporation Ltd

.png)

SGP Details

Strong dividend payout:Stockland Corporation Ltd (ASX: SGP) reported a statutory profit of $889 million and an underlying profit of $660 million for FY16. The company has paid a dividend of 24.5 cents for FY16, reflecting about 86% of payout. RoE for FY16 stands at 11% which is up from 9.9% in FY15 while FFO per security comes to 31.1 cents. SGP’s retail portfolio has $681 million developments under construction. Logistic and Business parks account for 25% of portfolio and have over 330,000 sqm of leasing activity under active management.

We rate the stock as a “Hold” at the current market price of - $4.70

SGP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...