Rio Tinto Ltd

.png)

RIO Dividend Details

Enhancing iron ore production: Rio Tinto Limited (ASX: RIO) improved its global iron ore production by 12% over same quarter of 2014 to 86.1 mt in Q32015, driven by the enhanced iron ore mined capacity, productivity gains and Pilbara infrastructure expansion. Accordingly, RIO’s Global iron ore shipments increased by 17% yoy to 91.3 mt, and the company is on track to achieve full FY15 guidance. Meanwhile, Pilbara operations production improved by 11% yoy to 227.6 million tonnes (with Rio Tinto share of 185.1 million tonnes) during the first nine months of 2015. Improving Nammuldi operations coupled with several other productivity enhancement efforts led to these solid gains across most of the Pilbara operations sites. Bauxite production also depicted a decent performance during the third quarter wherein the third party shipments reached over 20 million tonnes during this year to date driven by the record production at Weipa. On the other hand, Mined copper production fell by 24% yoy to 115 kt during the period but Oyu Tolgoi was boosted by higher grades while Kennecott continued to focus on the east wall de-weighting and de-watering. Meanwhile, RIO agreed to sell its interest in the Bengalla thermal coal Joint Venture for $606 million in September to New Hope Corporation Ltd, to focus on its core assets.

.png)

Third quarter performance (Source: Company Reports)

Stock Outlook: The shares of RIO fell 15.11% in the last six months (as of November 04, 2015) impacted by falling iron ore prices and economic uncertainty. However, RIO is focusing to improve production efficiency, control costs as well as manage capital efficiently to offset the pricing pressure. Accordingly, RIO is targeting to enhance its cash flow to survive the commodity price pressure. RIO estimates its iron ore shipments to improve further driven by its Pilbara infrastructure expansion. The group forecasts its global iron ore shipments to be over 340 million tonnes (100 per cent basis), from its operations in Australia and Canada for the full year of 2015. The company also forecasts that global iron ore demand is expected to grow at a rate of about 2% a year to around 3 billion tonnes by 2030. The company expects to have emerging markets other than China playing a key role in the demand for iron ore. Particularly, the non-Chinese demand for steel is expected to surge by 65% in the period to 2030 with ASEAN economies and India contributing a lot. RIO stock delivered slight returns of 2.09% in the last four weeks, and has a decent annual dividend yield of over 5.86%. We recommend investors to BUY the stock at the current price of $50.15

BC Iron Ltd

.png)

BCI Dividend Details

Efforts to generate positive cash flow and offset iron ore price pressure: BC Iron Limited (ASX: BCI) and Fortescue Metals Group (FMG) recently agreed for a three month trial arrangement to vary the rail and port tariff paid to FMG, i.e., by changing the terms of the rail and port services agreement between the Nullagine JV (NJV) and The Pilbara Infrastructure Pty Ltd (FMG’s subsidiary). Management reported that given the current commodity prices volatility, the differed terms for rail and port charges would help manage the prices so that the group would be able to generate further positive cash flows from its NJV. As per the proposed terms for the next three months, the Tariff might decrease / (increase) by over US$0.50/wmt for each US$1/dmt change in the US$ CFR 62% Fe price below / (above) US$56/dmt. Primarily, tariffs change in either direction would vary based on drop in the iron ore price. Accordingly, BC Iron estimates to generate cost savings of over $2.3 million during the three month period. On the other hand, the group also gave the NJV road haulage contract to Qube Bulk (effective from December) and estimates to have over 30% to 35% decrease in total road haulage costs (inclusive of fuel and overheads). As per the September quarter of 2015 highlights, Bonnie Fines shipped from the NJV reached 1.40M wmt, wherein the group’s share is 1.06M wmt. NJV C1 cash costs declined by $5/wmt to $44/wmt (FOB) during the quarter while the group’s all-in cash costs fell by $6/wmt to $52/wmt. BCI also enhanced its cash by $4.1 million to $71.8 million as at the end of the quarter.

.png)

NJV September highlights (Source: Company Reports)

On the other hand, BCI stock plunged 56.45% (as of November 04, 2015) during this year to date impacted by the falling commodity prices. However, the group’s efforts to sustain its positive cash flow along with the cost control efforts drove the stock over 20% in the last four weeks alone. We recommend investors to HOLD the stock at the current price of $0.26

Arrium Ltd

.png)

ARI Dividend Details

Ongoing performance pressure: Arrium Ltd (ASX: ARI) reported that its sales and shipments were 2.09Mt and 2.20Mt, respectively, during the quarter ended on September 2015, and its average Platts market index price (62% Fe CFR) fell by US$3/dmt to US$55/dmt as compared to the June quarter. Average total cash cost of CFR China also fell by A$4.8/dmt to A$57.4/dmt as compared to the earlier quarter. The average price was only US$48 (A$66) a tonne for iron ore shipped during the September quarter. Meanwhile, the group intends to achieve an average cash breakeven iron ore price of ~US$47/dmt by fiscal year of 2016. On the other hand, the group produces a lower iron ore grade and with the falling iron ore prices, we believe that ARI would continue to face pressure in business despite its cost cutting efforts. Given the tough market conditions and slowdown in China, demand for higher grade iron ore is better against the lower iron ore grade.

.png)

September quarter highlights (Source: Company Reports)

ARI stock fell over 52.82% in the last six months (as at November 04, 2015) and we believe the negative momentum would continue even in the coming months, given the heavy competition from already established low iron ore grade producers like FMG coupled with challenging market conditions. Accordingly, we place an Expensive recommendation on the stock at the current price of 0.092

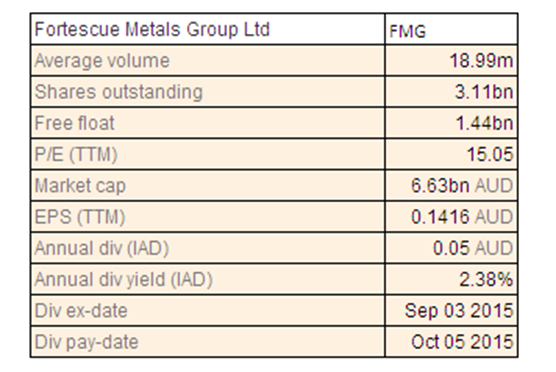

Fortescue Metals Group Ltd

FMG Dividend Details

Reduction in production costs: Fortescue Metals Group Limited (ASX: FMG) said that it has successfully lowered its production costs for seventh consecutive quarter in September 2015 quarter by 47% against prior corresponding period (pcp). Accordingly, the group was able to deliver solid operating cash flows during the quarter and hence repurchased over USD 384 million of debt on market (for an average price of 80 cents in the dollar realizing a pre-tax gain of $68 million) and even enhanced its cash balances to US$2.6 billion. FMG reported that its shipments reached 41.9mt with cash production costs (C1) of US$16.90 per wet metric tonne during the September 2015 quarter. The group achieved a price realization of 91% to US$50/dmt against the average 62% Platts price of US$55/dmt.

.png)

Cost Improvements (Source: Company Reports)

Stock Outlook: For FY16, Fortescue Metals issued a guidance of 165mt shipments and C1 cost of US$18/wmt will be updated during the release of the half year results. The group targets to achieve a production cost of US$15/wmt at an exchange rate of 0.72 by FY16. The group’s efforts of operating costs reductions lowered its C1 sensitivity to 18 cents per one cent movement in the exchange rate. FMG estimates a sustainable capex of US$330 million or US$2/wmt excluding vessel funding during FY16. Meanwhile, FMG’s Iron Bridge Stage 1 plant trials are ongoing with prospect developments subject to effective finishing of Stage 1 and joint venture approval. FMG shares recovered over 14.21% in the last four weeks (as of November 04, 2015) and we believe that the stock is trading at reasonable valuation with a P/E of 16.06x. Accordingly,

we recommend investors to “HOLD” the stock at the current price of $2.13

BHP Billiton Ltd

.png)

BHP Dividend Details

Enhancing assets and efficiency: BHP Billiton Limited (ASX: BHP) raised its iron ore production by 7% in the September quarter and is all set to meet full-year 2016 guidance. The production hit a record 61 Mt in the fiscal first quarter in support from a ramp-up of the Jimblebar mine in Western Australia. BHP also acquired 100% working interest on nine blocks in the Western Gulf of Mexico Lease while 17 are still subject to regulatory approval and also got approval for operational permits extension for Cerro Colorado till 2023. The group is developing four major projects worth of US$7.0 billion in Petroleum, Copper and Potash as of September 2015 quarter. On the other hand to offset the commodity prices pressure, BHP is undertaking cost reduction efforts in petroleum for Onshore US as well as Conventional businesses, and is on-track to meet its production targets with US$200 million less capital investment. BHP is also boosting its balance sheet and recently priced Eur 2.0 billion of subordinated fixed rate reset notes across two tranches, GBP600 million of subordinated fixed rate reset notes and USD 3.25 billion of subordinated fixed rate reset notes across two tranches, and is diverting these proceeds to cover its debts. Meanwhile, the group’s stock fell over 22.32% in the last six months (as of November 04, 2015) impacted by commodity prices’ volatility and demerger of South32 related costs. BHP Billiton and the Banjima people of Western Australia’s iron ore-rich Pilbara region have signed a deal with regards to 8263 square kilometres of the Banjima’s 10,000 square kilometres of land in the central Pilbara. The agreement seems to protect certain areas from mining and deals with the life of BHP’s on-going mining operations and future developments. We believe the group has a solid long term potential and the recent correction offers attractive entry to investors looking for solid dividend stocks. BHP has an outstanding dividend yield of 7.18%.

We give a BUY recommendation on the stock at the current price of $23.28

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...