Cedar Woods Properties Limited

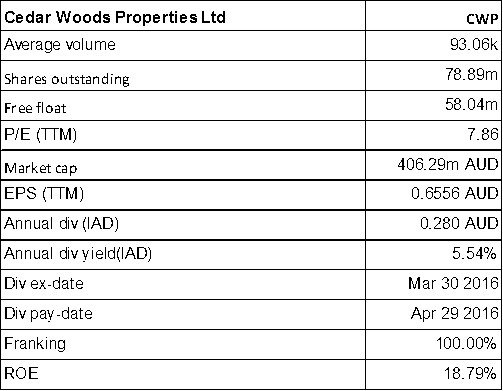

CWP Details

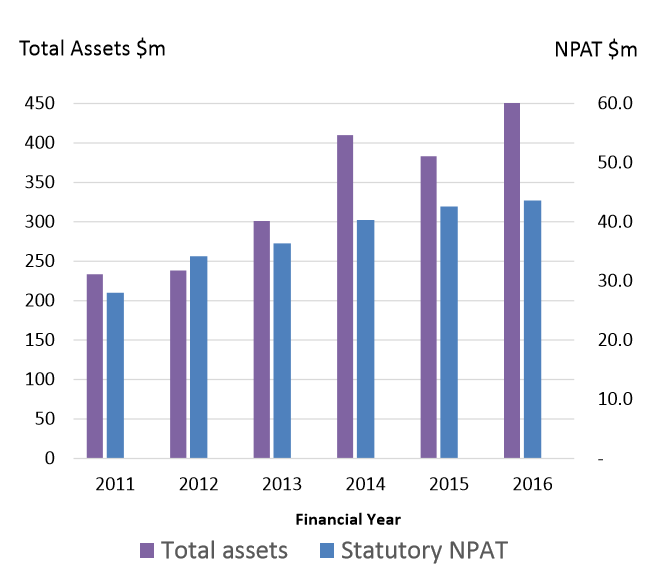

Consistent growth in NPAT and Dividends: Cedar Woods Properties Limited (ASX: CWP) announced its FY16 results entailing a consistent growth in NPAT (up 2.4% for the year to $43.6m) and dividends (up 1.8% for the year to 28.5 cents per share). The balance sheet is strong with $98.5m of finance facility headroom as at June 30, 2016.

Financial Performance (Source: Company Reports)

CWP has also been selected by Renewal SA for Port Adelaide redevelopment of up to 40 hectares. Both of them would work together for the six months to develop a master plan in consultation with the community. The State Government will then determine whether to accept CWP’s proposal. Moreover, the South Australian Government has approved the conditional sale of a 16.5-hectare site in Glenside, Adelaide to Cedar Woods for a price of $25.8 million plus GST. Meanwhile, the group got approval from its financiers to increase its corporate finance facility from $135 million to $175 million to provide funding for Glenside and future opportunities.

CWP stock has risen 27.27% in the last six months (as of August 24, 2016), and has a decent dividend yield while still trading at lower P/E. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $5.11

CWP Daily Chart (Source: Thomson Reuters)

GDI Property Group Ltd

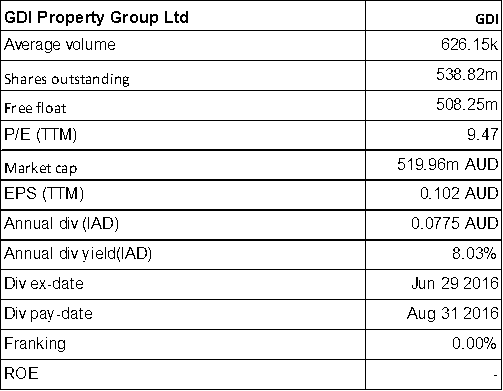

GDI Details

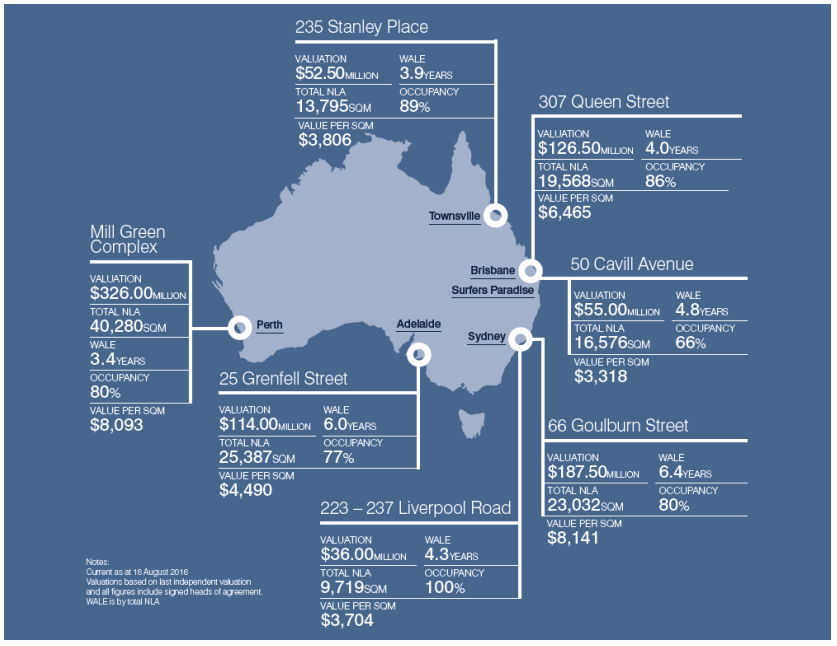

Drop in gearing: GDI Property Group Ltd (ASX: GDI) reported for full year FFO of 9.11 cents per security which is up 10.83% and the distribution of 7.75 cents per stapled security. At the same time, the absolute total return for the year has been 9.85%. Gearing has decreased to 32.2% from 35.6% as a result of investment transactions. GDI had earlier determined to hold over 45% interest in the Trust which is expected to add around $1.3 million to Funds from Operations in FY17, in addition to fees generated for managing the Trust. After the acquisition of the stake, GDI’s drawn debt would be $290 million, with undrawn debt of about $30 million. The group has also established GDI No. 42 Office Trust which owns two properties at Townsville and Ashfield Property.

Portfolio Overview (Source: Company Reports)

GDI stock has risen 13.53% in the last six months (as of August 24, 2016), and still the stock has a lucrative dividend yield while trades at a reasonable P/E. GDI is paying AUD 0.038 on August 31, 2016. Based on the foregoing, we give a “Speculative Buy” recommendation on the stock at the current price of $0.98

GDI Daily Chart (Source: Thomson Reuters)

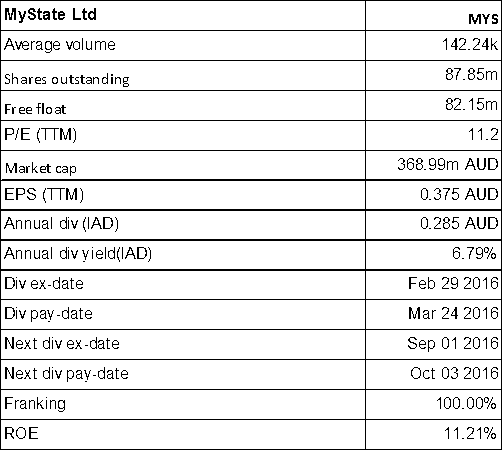

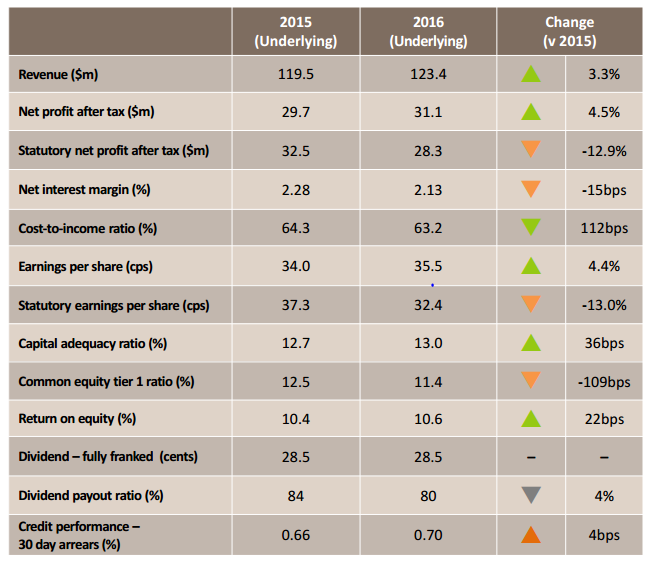

MyState Limited

MYS Details

Strong growth and plans to acquire La Trobe Financial:MyState Limited (ASX: MYS) reported 4.5% growth in underlying NPAT of $31.1m over the prior corresponding period (pcp) while the statutory NPAT slipped 12.9%. The underlying EPS growth was 4.4% which outperformed the sector. The underlying revenue jumped up 3.3% over pcp.

Financial Performance (Source: Company Reports)

Overall, MYS reported for a sound FY16 result and also intends to grow and expand via acquisitions and industry consolidation. The group earlier confirmed that it has held discussions with La Trobe Financial on a possible acquisition. Moreover, MYS has partnered with Rubik Financial for the transformation of the digital channels and customer experience offering. Trading at a solid dividend yield and reasonable P/E, we give a “Speculative Buy” recommendation on the stock at the current price of $4.28

MYS Daily Chart (Source: Thomson Reuters)

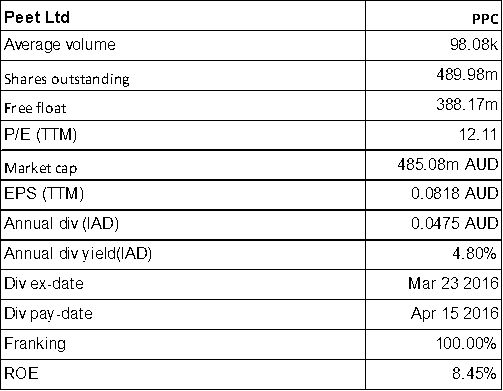

Peet Limited

PPC Details

Moving on growth track: Peet Limited (ASX: PPC) reported for strong performance with 11% jump in FY16 operating profit after tax of $42.6m. EPS has been up 5% to 8.7 cents per share. The company now has 2,426 lots as record contracts on hand which are valued at $546m. Though, the EBITDA dropped 3%, the overall performance has been on growth track with diversified pipeline of lots. The company’s outlook has been supported by market fundamentals and low interest rate. A new wholesale fund has been established by Peet and Supalai Public Company, a real estate developer listed on the Thailand stock exchange, with each being 50% co-investors. Peet would act as the development manager for the fund. Moreover, the wholesale fund has acquired a residential estate in Redbank Plains, Queensland, which is in development and which would be amalgamated with an adjacent property. PPC currently has under option to create a 1,100-lot residential master-planned community. The total acquisition price for the Properties is $37.45 million and the contract is unconditional, with the settlement expected to occur in September 2016. PPC is the development manager with the project expected to be developed out over six years, with an expected completion in late 2022.

Meanwhile, PPC stock has surged over 8.8% in the last three months (as of August 24, 2016), and still the stock has a decent dividend yield as well as is trading at a reasonable P/E. Accordingly, we give a “Buy” recommendation on the stock at the current price of $1.00

PPC Daily Chart (Source: Thomson Reuters)

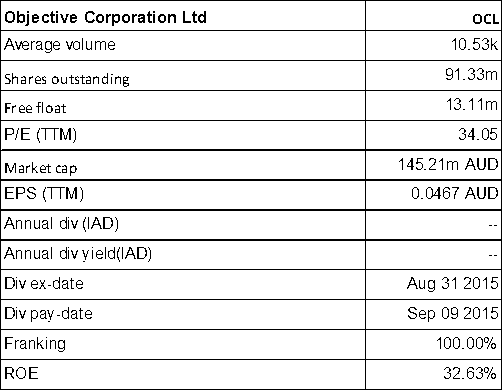

Objective Corporation Ltd

OCL Details

Contract with IBM and Defence: Objective Corporation Ltd (ASX: OCL) secured a new contract from IBM for delivery of a key component of the Australian Department of Defence’s End User Compute (EUC) Program and this has a value of US$1.9 billion. This Program is one of several initiatives designed to establish a dependable, secure and integrated Single Information Environment (SIE) to support Defence business and military operations.

The contract is worth in excess of $10 million to OCL and this amount spreads over FY17 and FY18. The company also acquired 100% stake in Onstream Systems Ltd in FY16. The stock has fallen 3.64% in the last one month (as at August 24, 2016). We put a “Speculative buy” at the current price of $1.61

OCL Daily Chart (Source: Thomson Reuters)

DisclaimerThe advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...