MyState Ltd

.png)

MYS Dividend Details

Attractive opportunity: MyState Limited (ASX: MYS) announced good financial results for the half-year ended December 31, 2015 with net profit after tax (NPAT) of $15.1 million, an increase of 1.5% over previous corresponding period (pcp). MYS also announced an interim dividend of 14 cents per share, representing payout ratio of 81% in line with previous dividends. The company continued its strong growth in loan book, increasing by 6.6% from June 30, 2015 to reach $3.8 billion.

.png)

Key metrics showing strong growth (Source: Company Reports)

This growth is double the Australian home loan system growth. Overall, the loan book has grown by 25% in the last 18 months indicating the possibility of boosting MYS’s bottom-line performance. The competitive scenario looks intense but the outlook for the Tasmanian economy is improving continuously, thus enabling a positive outlook for MYS.

The stock is down almost 15.58% in the past one year (as of March 24, 2016) placing at an attractive P/E and a decent dividend yield. Accordingly, we give a “Speculative Buy” at the current price levels of $4.28

MYS Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Dividend Details

Cost cutting initiatives to sustain the slowdown economic conditions: Australia and New Zealand Banking Group Ltd (ASX: ANZ) has recently announced unaudited cash profit of $1.85 billion for the three months ending December 31, 2015, an increase of 5% over the average of third and fourth quarters of FY15. The slowing of Asian economy partly resulted in direct impact since the group’s exposure in Asia is mainly short tenor. Therefore, the stock has fallen more than 34.89% (as of March 24, 2016) in the past one year. On the other hand, ANZ is focused on reducing costs with a 2.5% reduction in staff numbers and continues to reduce staff in various markets. Further to the Australian Securities and Investments Commission (ASIC) allegation against ANZ bank trading and bank bill swap rate, the company rejected the allegations. According to ANZ’s latest update, the company expects the total group credit charge to increase by at least $100 million over the $800 million estimate provided before in view of a small number of resources-related exposures. ANZ’s BDD charges may persist at such levels in 2H16 and probably in 2017. Thus, stabilization in the BDD charges is important while the sector’s aggregate exposure to resources looks to be manageable to some extent. However, impact may be seen in short to medium term.

ANZ has made various changes in its approach to wealth management in an attempt to simplify it. Meanwhile, the stock is not trading at expensive valuation and has a low price to earnings ratio (P/E). Despite the current challenges but positive long term expectations, we reiterate our “Buy” recommendation on this stock at the current price levels of $23.20

ANZ Daily Chart (Source: Thomson Reuters)

Westpac Banking Corp

.png)

WBC Dividend Details

Strong cash earnings: Westpac Banking Corp (ASX: WBC) announced its Consumer Bank and Business Bank update revealing strong performance. Consumer Bank, with 34% of Group revenue had a $7 billion revenue as of September 30, 2015 and one in every three Australians as customers. Its Business Bank has a revenue of $5 billion, 24% of Group revenue and is showing good improvement in deposit to loan ratio at 69.6%. The recent update of Westpac New Zealand also revealed good growth with a 6% increased cash earnings at $916 million. On the other hand, the weak outlook for the Australian economy in 2016 might pose pressure on its consumer bank business. The recent rally in the stock over 8.28% (as of March 24, 2016) in the past month also placed them at higher valuations.

Hence, we believe that the stock is “Expensive” at the current price levels of $29.93

WBC Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.png)

NAB Dividend Details

Strategic focus on core markets: National Australia Bank Ltd (ASX: NAB) revealed good numbers in its 2016 first quarter with unaudited cash earnings for continuing operations increasing by 8% to reach $1.7 billion over the pcp. The company had improved lending volumes and higher net interest margin (NIM). Improved asset quality for NAB resulted in 52% decrease in charge for Bad and Doubtful Debts (B&DDs) to $84 million. With a focus on core markets Australia and New Zealand, NAB completed the demerger and initial public offering (IPO) of Clydesdale/Yorkshire Bank (CYBG).

With a drop of almost 29.08% over the past year (as at March 24, 2016), NAB stock is priced at a low price to earnings ratio (P/E) and has an outstanding dividend yield. Accordingly, we recommend a “Buy” on this stock at current price levels of $25.62

.PNG)

NAB Daily Chart (Source: Thomson Reuters)

Commonwealth Bank of Australia

.png)

CBA Dividend Details

Below par financial performance: Commonwealth Bank of Australia (ASX: CBA) revealed subdued results for half year ended December 31, 2015 with a 2% increase in net profit after tax (NPAT) to $4.618 billion over the prior comparative period. The revenue fell by 4% to $21.924 billion and the company announced an unchanged interim dividend of $1.98 per share.

.png)

Decrease in Return on Equity (Source: Company Reports)

According to the latest Commonwealth Bank Business Sales Indicator (BSI), there is a clear slowdown in spending in the economy. We believe that the stock is “Expensive” at the current price levels.

.PNG)

CBA Daily Chart (Source: Thomson Reuters)

Bendigo and Adelaide Bank Ltd

.png)

BEN Dividend Details

Weak half year results: Bendigo and Adelaide Bank Ltd (ASX: BEN) announced weak results with income from operations for the half year ending December 31, 2015 down 0.6% to $781.6 million while the net profit after tax (NPAT) from ordinary activities was down 8.2% to $208.7 million.

.png)

Lending growth (Source: Company Reports)

The cash earnings per share saw a marginal increase of 1.7%. It is noted that BEN has been affected by price competition for mortgages and the low interest rate environment. Nonetheless, the stock of the company has increased by over 6.51% (as of March 24, 2016) over the past month and is trading at a premium. Thus, we believe that the stock is “Expensive” at the current price levels of $8.82

BEN Daily Chart (Source: Thomson Reuters)

Bank of Queensland Ltd

.png)

BOQ Dividend Details

Investment in improving processes: Bank of Queensland Ltd (ASX: BOQ) is facing representative proceedings filed against it in the Federal Court of Australia in New South Wales by Petersen Superannuation Fund Pty Ltd on behalf of certain customers over Sherwin scandal, which the bank intends to defend. BOQ is reshaping its organizational structure in line with its redefined strategy. To enable more flexible and efficient operating model, BOQ expects an investment requirement of about $15 million pre-tax, but also believes that it would deliver 100% return through cost savings within a year.

The company is aiming to reach a cost to income ratio of below 40% in the coming years. Meanwhile, BOQ stock has fallen by more than 12.42% (as of March 24, 2016) in the past three months placing them at reasonable P/E and a decent dividend yield. We believe that the stock is a “Buy” at these price levels of $11.95

BOQ Daily Chart (Source: Thomson Reuters)

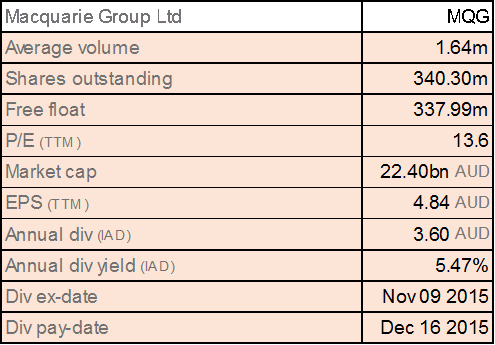

Macquarie Group Ltd

MQG Dividend Details

Uncertainty in market conditions: Macquarie Group Ltd (ASX: MQG) has announced the selling of 9.99% stake in Southern Cross Media Group Limited (ASX: SXL) to Nine Entertainment Co. (ASX: NEC) at a price of $1.15 per share. This follows the announcement by Australia of plans to deregulate the media sector. AFR Weekend recently claimed MQG to be one the world’s biggest junk bond investors, which the company is refuting. Lately, the Australian Securities and Investments Commission ordered MQG to overhaul its way of handling client money, ruling that the bank had breached the rules for a decade.

MQG also faces short term challenges such as weak market conditions, impact of foreign exchange and the cost of its continued conservative approach to funding and capital. Given, these negative conditions and sentiments, we believe that the stock is “Expensive” at the current price levels.

MQG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...