Aristocrat Leisure Limited

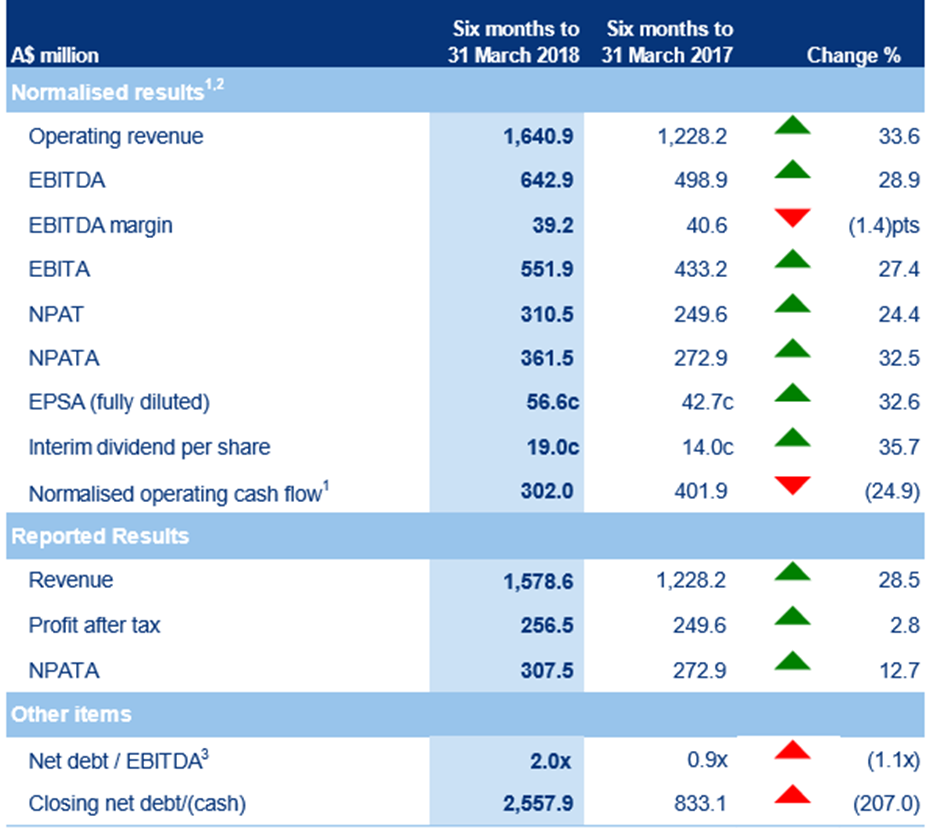

Decent Outlook: Aristocrat Leisure Limited’s (ASX: ALL) stock has risen 20.14% in three months as on July 24, 2018 as for 1H 2018 result entailed 36% growth in the normalised profit after tax and before amortization of acquired intangibles (NPATA) to $361.5 million. This also represents growth of 36% in constant currency, compared to the six months to 31 March 2017. The growth was driven by strong performance in the Group’s Americas and Digital businesses, including the recent acquisitions of Plarium and Big Fish, along with a further increase in performance in the ANZ region. Moreover, ALL expects double-digit NPATA growth to continue in FY18 compared to FY17. In 2018, ALL expects a 300 basis point reduction in its effective tax rate compared to the PCP. For land-based outright sales, ALL expects to defend market-leading share positions across key sale segments in North America, ANZ and International CIII segments. For land-based gaming operations, ALL expects increased investment in content and technology to expand its total install base and fuel growth in adjacencies. The company expects to maintain a market-leading average fee per day performance. In Digital segment, ALL is focusing on integration of acquisitions. The company also expects further growth in its social casino and social games business, with increased investment in user acquisition associated with the launch of new apps across all business units. In addition, ALL expects to increase D&D investment across both land-based and digital portfolios in absolute dollar terms, over the full year 2018, in order to defend and grow leadership positions across a much broader business, and pursue priority adjacencies in line with ALL’s growth strategy. Meanwhile, ALL stock is trading at a high P/E and its ROE has also been significantly high at 40.9% against industry median of 12.4%. The operating and gross margins at 29.6% and 60.7% for 2017 have also been up against industry standards. However, the stock is trading at a higher valuation and looks “Expensive” at the current price of $ 32.170.

1H 18 Financial Performance (Source: Company Reports)

Afterpay Touch Group Ltd

Fourth Quarter Business Update: Afterpay Touch Group Ltd.’s (ASX: APT) stock has risen 159.07% in three months as on July 24, 2018; and the company for the fourth quarter 2018, has reported 171% rise in the underlying sales to approximately $736m over Q4 FY17 and a 39% increase over Q3 FY18. Moreover, the company had launched U.S. business in mid-May 2018 and has posted over $11m of underlying sales in the first full month of June 2018. The company has signed over 400 retailer contracts and over 200 retailers are currently transacting on the platform, which include major millennial focused brands, URBAN OUTFITTERS (live since 16 May 2018) and REVOLVE (live since 9 July 2018). Additionally, for FY 18 the company expects Group Revenue and Other Income to be around $142m, FY18 Group EBITDA is expected to be in the range of $33m to $34m and FY18 Group EBTDA is expected to be in the range of $27m to $28m. This forecast is subject to audit. Meanwhile, APT stock was added to S&P/ASX 200 index, effective from 18th June 2018. The stock has a high gross margin at 77% for 2017 against industry median of 57.3%, while ROE is yet to outweigh the industry standard. Based on the foregoing and the high run-up while US expansion is expected to set the next leg of growth, we give a “Hold” recommendation on the stock at the current price of $ 14.750 (up 2.2% on July 25, 2018).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...