Ruralco Holdings Ltd

.png)

RHL Dividend Details

Diversified earnings base offset pressure from extended dry seasonal conditions: Ruralco Holdings Ltd (ASX: RHL) reported a revenue rise of 18% year on year to $1.6 billion in fiscal year of 2015 boosted by the full year impact of Total Eden and Frontier which added $210 million. The group’s gross profit rose by 19% yoy to $307.0 million driven by better volumes and livestock prices. As a result, RHL delivered a reported net profit after tax increase by 33% yoy to $14.1million in FY15 on the back of rising contribution from its agency business coupled with steady rural supplies business in spite of challenging market conditions. Meanwhile, RHL stock corrected over 9.89% in the last six months (as of December 22, 2015) on investors’ concerns over its performance due to volatile seasonal conditions in certain regions.

.png)

Underlying NPAT Bridge (Source: Company Reports)

On the other hand, the falling Australian dollar would drive its agricultural sectors involved in wool, grain, livestock and real estate. Moreover RHL is expanding its live export business to a two vessel model since January 2016 by opening new markets into China while ongoing Vietnam growth would contribute to the division’s performance. We remain bullish on this 4.95% dividend yield stock and reiterate our “BUY” recommendation at the current price of $3.27

RHL Daily Chart (Source: Thomson Reuters)

Spark New Zealand Ltd

.png)

SPK Dividend Details

Strengthening cloud services: Spark New Zealand Ltd (ASX: SPK) recently rose prices for some of its broadband and landline plans effective from February 2016, with ADSL and VDSL Broadband plans rising by $5 a month as a part of Commerce Commission decision to hike regulated Chorus line charges for copper broadband and landline services. While this move might pose a pressure over its competitive pricing to customer, Spark New Zealand has been focusing on data, mobile and ICT platform services and accordingly launched several products like Revera, Skinny, Bigpip, Lightbox, Qrious big data analytics, Putti apps, and Morepork. As a result, Spark New Zealand mobile revenue share surged 40% yoy driven by solid consumer growth for fiscal year of 2015. The group recently acquired Computer Concepts Limited (CCL), a South Island based IT infrastructure and professional services for $50 million to boost its cloud and platform IT services capabilities, enabling the group to further penetrate its market reach and offerings. Spark New Zealand also enhanced its capital position by offering up to $100 million unsecured, unsubordinated fixed rate bonds (Bonds) for institutional as well as New Zealand retail investors. This buyback has been successfully finished as per the recent update. SPK shares surged over 20.63% (as of December 22, 2015) in the last six months and trading at a P/E of 15.52x. The group has an outstanding dividend yield of 6.37%. We maintain our “BUY” recommendation on the stock at the current price of $3.09

SPK Daily Chart (Source: Thomson Reuters)

IMF Bentham Ltd

.png)

IMF Dividend Details

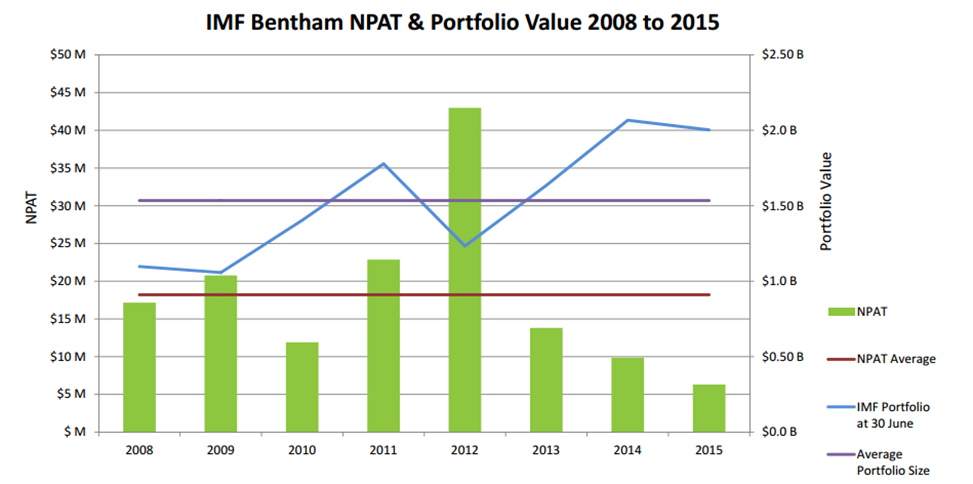

Strong portfolio value despite case losses: IMF Bentham Ltd (ASX: IMF) shares corrected over 37.14% during this year to date (as of December 22, 2015) as the group’s second half of 2015 was impacted by case losses, leading to its overall FY15 earnings pressure. However, IMF built a portfolio value of $2.1 billion (as of September 2015) and kept adding new cases of low average case size. The group is building strong Asian presence and even funded third case in Hong Kong Market. The group delivered a solid growth in US cases, which rose 31% of the investment portfolio since 2011. The company recently announced for funding of another case in the US with initial claim value of $115 million. The updates on funding of class action against Lehman Brothers Australia Ltd indicate a possibility of IMF receiving $39 million in further recoveries (subject to fruition) and the company is considering whether to bring the additional amount to account for the revenue for half year ending 31 December 2015.

NPAT and portfolio value (Source: Company Reports)

IMF has over 94% success rate on large number of cases and generated a return on investment of 158%. The group continues to win new cases and recently settled claims against Gunns Limited officers and directors and estimates to generate revenue over $4.9 million and a PBT of over $9.2 million. We reiterate our positive stance and a “Buy” recommendation on this 7.46% dividend yield stock at the current price of $1.32

IMF Daily Chart (Source: Thomson Reuters)

IOOF Holdings Ltd

.png)

IFL Dividend Details

Targeting growth via acquisitions: IOOF Holdings Limited (ASX: IFL) delivered a 41% yoy increase of underlying profit after tax for 2015 to $174 million for fiscal year of 2015, driven by better cash flows, SFG acquisition contribution as well as organic growth. IFL reported that the value of funds for its clients rose by 29% to $124 billion in FY15. IOOF Holdings also generated good underlying organic growth driven by its new products during the year coupled with rising service levels for clients. On the other hand, the shares of IFL fell over 2.27% in the last six months (as of December 22, 2015) due to allegations on the company while the group disapproved these claims against them. But, we believe that the group would be able to maintain growth track via acquisitions and organic growth. Hence, we remain bullish on this 5.8% dividend yield stock and reiterate our “BUY” recommendation at the current price of $9.13

.png)

IFL Daily Chart (Source: Thomson Reuters)

Wam Capital Ltd

.png)

WAM Dividend Details

Ongoing strong investment portfolio performance: WAM Capital Ltd (ASX: WAM) continued to generate a better return against the index with its investment portfolio raising by 3.5% in one month as of November, 2015 beating the benchmark S&P/ASX All Ordinaries Accumulation Index by 4.2% as the index decreased by 0.7% during the same period. Accordingly, the stock surged over 6.67% in the last six months (as at December 22, 2015), and we believe the positive momentum would continue in the coming months. The group has an advantage of keeping a flexible investment portfolio as the investment team sits on huge cash during tough market conditions, preserving the portfolio from uncertainty impacts.

Therefore, WAM has an average cash weighting of 38.1% and an average equity weighting of 61.9%. WAM is also trading at reasonable valuations and has a strong dividend yield of 6.76%. We recommend a “BUY” on the stock at the current price of $2.10

WAM Daily Chart (Source: Thomson Reuters)

Fantastic Holdings Ltd

.png)

FAN Dividend Details

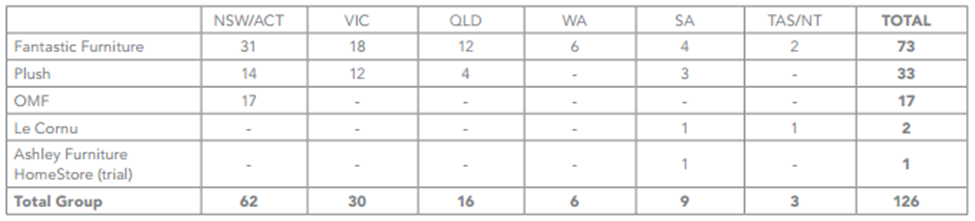

Strong Plush business: Fantastic Holdings Ltd (ASX: FAN) reported a 8.7% increase of like for like sales in Fantastic Furniture during fiscal year of 2015 boosted by strong second half of 2015 rise of 15.9%. Meanwhile the group’s Plush business delivered a strong like for like sales growth of 43.4% in FY15 wherein the second half witnessed an increase of 35.1% on year on year (yoy) basis, indicating a winning Plush’s simplified business model. Meanwhile, FAN reported a like for like sales increase of 12.8% during July 2015 and is expanding its production at Sofa Factory in China, and improving its supply chain through consolidation of products and direct shipping to Fantastic Furniture stores.

Fantastic Holdings Network as of June 2015 (Source: Company Reports)

Expansion with new stores is planned later in the second half of FY16 and Plush continues to focus on improving its product offering and in-store customer experience.

FAN intends to open more new stores at Far North Queensland while the company is continuously investing in its e-commerce platform to leverage the booming online opportunity. The shares of FAN delivered year to date returns of 21.80% (as of December 22, 2015) and we believe this positive momentum would continue in the coming months. Fantastic Holdings also has a good dividend yield. We reiterate our “Buy” recommendation on the stock at the current price of $2.15

.png)

FAN Daily Chart (Source: Thomson Reuters)

Automotive Group Holdings Ltd

.png)

AHG Dividend Details

Delivered strong shareholder returns: Automotive Group Holdings Ltd (ASX: AHG) had been rewarding its investors by generating a total shareholder returns of over 11% (includes capital growth and reinvestment of dividends) in the last twelve months (as of November 18, 2015) and more than 156% in the last five years. The group is undergoing restructuring efforts as well as divesting non-core assets to boost its cash flow in order to offset the tough retail market conditions. Meanwhile, AHG’s core Automotive division revenues improved by over 10% on a year over year basis to $3,883 million for fiscal year of 2015, boosted by better contribution of east coast and New Zealand markets. The group has a strong competitive market position and sells more than 110,000 new and used vehicles a year while generates over ~$1 billion p.a. of auto finance. AHG is making Greenfield dealerships additions and undertaking acquisitions and investments to sustain growth in the coming periods.

AHG’s opportunities (Source: Company Reports)

AHG also acquired Paceway Mitsubishi WA, Leo Muller CJD Qld and Hillcrest Mazda Qld to strengthen its performance and offerings. The latest update from the Australian Competition and Consumer Commission disapproving the proposed acquisition by GPC Asia Pacific Pty Limited (GPC) of the Covs Parts business from AHG, was in the news impacting the AHG’s shares.

With the stock surging over 10% in the last three months (as of December 22, 2015), we believe that the stock’s positive momentum would continue in the coming months. The group is also trading at a modest P/E while having a dividend yield of 5.01%. We reiterate our “BUY” recommendation on the stock at the current price of $4.40

Breville Group Ltd

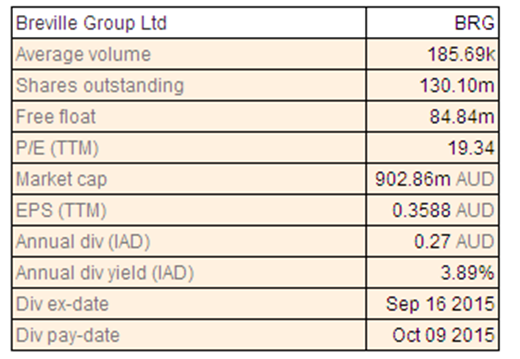

BRG Dividend Details

Recovering performance driven by its growth efforts: Breville Group Ltd.’s (ASX: BRG) Australia and New Zealand division revenues declined by 6.3% yoy during FY15 impacted by ERP implementation costs while discount department store retailers chose home brands against Group’s Kambrook/Ronson brands. As a result, the group’s overall revenues fell over 2.7% yoy to $527 million during fiscal year of 2015. On the other hand, BRG’s North America total revenue rose by 2.0% to $202.6 million with second half total revenue rising by 24.1% against prior corresponding period. Management reported that the group is trading on track with its expectations as of October 2015 but cautioned that the rising US dollar has been impacting business in some countries. Meanwhile, BRG stock surged over 22.16% in the last three months (as at December 22, 2015) and we believe that this positive momentum would continue given its constant investment in product development and marketing efforts coupled with its expanding product pipelines. We place a “HOLD” on BRG at the current levels of $7.00

BRG Daily Chart (Source: Thomson Reuters)

Cash Converters International Ltd

.png)

CCV Dividend Details

Strong online business: Cash Converters International Ltd (ASX: CCV) faced a class action claim while a writ was lodged against its brokerage fees from Jul 2009 to Jun 2013. The court also approved the NSW class action settlement. Moreover, the group terminated Kentsleigh/Cliffview agency agreement which led to an impact of over $29.6 million during FY15. As a result, the shares plunged over 50.49% (as of December 22, 2015) during this year to date and fell 29.86% in the last six months alone. On the other hand, CCV made a provision of $23 million for settlement of NSW Class Action and settled it during October 2015. CCV has built a strong online business platform and delivered a solid online cash advance volumes and personal loan volumes growth during FY15.

.png)

Ongoing strong online loan growth (Source: Company Reports)

Meanwhile, Emerchants signed a multiyear contract with CCV, wherein the group would leverage Emerchants customized prepaid debit cards to disburse cash advance loan funds for in store as well as online customers. CCV is trading at cheaper valuations with a relatively lower P/E. We reiterate our “BUY” recommendation on the stock at the current price of $0.51

CCV Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...