.png)

Stocks’ Details

Transurban Group

CAGR of 10.20% in Distribution: Transurban Group (ASX: TCL) is the owner, operator and developer of electric toll road as well as an intelligent transport system. The market capitalisation of the company stood at $43.07 Bn as on 4th February 2020. The company via a release advised the market that Transurban WGT Co Pty Ltd has received a document from the CPBJH Joint Venture regarding the West Gate Tunnel Project. It was mentioned that the D&C Subcontract has been terminated from the project based on a Force Majeure Termination Event.

For 1HFY20, the company reported a distribution amounting to 31.0 cents per stapled security. Moreover, during the span of five years, the company experienced a CAGR of 10.20% in distribution per share.

.png)

Distribution (Source: Company Reports)

What to Expect: For FY20, the company is expecting a distribution of 62 cents per share. For the near term, the company is focused on delivering on its key projects, maximising the performance of operations as well as enhancing customer offerings.

Stock Recommendation: During Q1 FY20, the company experienced a rise of 1.8% in average daily traffic along with growth achieved in all markets. TCL is available at EV/EBITDA multiple of 27.9x as compared to the industry median (Transport Infrastructure) of 28.3x on TTM basis. Hence, considering the company’s growth in dividends and primary focus on delivering key projects, we give a “Hold” recommendation on the stock at the current market price of $15.930 per share, up by 1.079% on 4th February 2020.

Accent Group Limited

Robust Performance in FY19: Accent Group Limited (ASX: AX1) owns and operates several footwear and apparel businesses. The market capitalisation of the company stood at $929.82 Mn as on 4th February 2020. On 19th February 2020, the company would be releasing its results for 1H FY20. During FY19, the company reported net profit after tax amounting to $53.8 million, reflecting a rise of 22.5%. EBITDA witnessed a rise of 22.5% and stood at $108.9 million.

During FY19, the company paid total dividends of 8.25 cents per share, which showcased a rise of 22%. Also, the company experienced a CAGR of 16.36% during FY15-FY19 in dividend payment. At the current market price of $1.755 per share, the Annual dividend yield of the company stood at 4.81% as compared to the industry average of 4.3% on TTM basis.

.png)

Dividend (Source: Company Reports)

Focused on Delivering Increased Shareholder Value: With the help of a strong balance sheet, sustainable sales and profit growth, the company continues to deliver increased shareholder value. The Board of the company is committed to deliver excess cash to shareholders and grow dividends over the coming years. The company added that future dividend payments would continue to align to net profit after tax generated in the relevant period.

Valuation Methodology: P/E based Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the span of the last ten financial years, the company has delivered total shareholder returns of 850%, or 25.3% per annum. Net margin of the company stood at 6.8% in FY19, reflecting YoY growth of 0.5%. This reflects that the company has improved its position for converting its topline into the bottom line. We have valued the stock using P/E based-relative valuation method and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, in the light of a strong balance sheet, sustainable sales and profit growth, and valuation, we maintain a “Hold “rating on the stock at the current market price of $1.755 per share, up by 2.332% on 4th February 2020.

Fortescue Metals Group Ltd

Increase in Shareholders Returns: Fortescue Metals Group Ltd (ASX: FMG) is involved in mining, processing, and transporting of iron ore. The market capitalisation of the company stood at $33.87 Bn as on 4th February 2020. The company recently announced regarding the Pilbara Generation Project with the worth of US$450 million. This project is the next stage of its Pilbara Energy Connect program. The company added that the Pilbara Generation Project complements the US$250 million Pilbara Transmission Project, which was announced in October 2019. This would also provide low-cost power to the energy efficient Iron Bridge Magnetite Project.

For Q2FY20, the company reported shipments of 46.4mt, reflecting a rise of 9% as compared to Q2FY19. This took 1HFY20 shipments to 88.6mt. Over the period of FY15-FY19, the company experienced a CAGR of 118.52% in the dividend. The following picture provides an overview of increased shareholder returns:

.png)

Shareholders Return (Source: Company Reports)

What to Expect: For FY20, the company is anticipating shipments to be at the upper end of 170 – 175mt and expects C1 costs to be in the range of US$12.75 – US$13.25/wmt on the back of strong performance in the 1H FY20.

Valuation Methodology: P/E based Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Return on equity of the company stood at 31.4% in FY19 as compared to the industry median of 12.3%. This reflects that the company has provided decent returns to shareholders against the broader industry. We have valued the stock using P/E based-relative valuation method and arrived at a target price, which is offering an upside of higher single-digit (in percentage terms). Hence, considering the company’s decent returns to shareholders, strong performance in 1H FY20, and decent outlook, we maintain a “Hold” rating on the stock at the current market price of $11.160 per share, up by 1.455% on 4th February 2020.

Telstra Corporation Limited

One-off Issue of Retention Rights: Telstra Corporation Limited (ASX: TLS) is engaged in the provisioning of telecommunications and information services. The market capitalisation of the company stood at $45.55 Bn as on 4th February 2020. The company, through a release announced that during FY19, it has made a one-off issue of 13,245,705 retention rights to eligible employees. During FY19, the company experienced a fall of 3.6% in total income and a decline of 21.7% in EBITDA. The decline in EBITDA has been due to the impact of the nbn, with Telstra absorbing around $600 million of negative recurring EBITDA headwind during FY19.

The Board of the company declared a fully franked total dividend of 16 cps, which reflects a return of more than $1.9 billion to shareholders. At the current market price of $3.820 per share, the annual dividend yield of the company stood at 2.61%.

Revised Guidance: For FY20, the company is expecting total income in the range of $25.3 to $27.3 billion as compared to the previous guidance range of $25.7 to $27.7 billion. The company is anticipating restructuring costs of around ~$0.3 billion.

.png)

Revised FY20 Guidance (Source: Company Reports)

Valuation Methodology: P/E based Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Gross margin of the company stood at 63.8% in FY19 as compared to the industry median of 61.0%. Net margin of TLS stood at 8.5% in FY19 against the industry median of 6.3%. During the span of one month and three months, the stock of TLS has provided returns of 6.69% and 8.81%, respectively. We have valued the stock using P/E based-relative valuation method and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering decent growth in margins and stock returns in the recent months, we maintain a “Hold” rating on the stock at the current market price of $3.820 per share, down 0.261% on 4th February 2020.

Smartgroup Corporation Ltd

Positive Financial Performance: Smartgroup Corporation Ltd (ASX: SIQ) is involved in salary packaging administration and fleet management services. The market capitalisation of the company stood at $874.16 Mn as on 4th February 2020. The company recently announced that Mitsubishi UFJ Financial Group, Inc has ceased to be a substantial holder in the company on 28th January 2020. On the financial front, the company reported positive financial performance in 1H FY19, wherein revenue stood at $125.8 million, reflecting a rise of 3% and NPATA stood at $40.5 million with a rise of 5%.

During 1H, the company declared a fully franked interim dividend amounting to 21.5cps with a rise of 5% and a fully franked special dividend of 20.0 cps, which was paid on 6th May 2019.

.png)

Dividend History (Source: Company Reports)

Focus Areas: The company continues to focus on increasing the adoption of digital channels and automation. The company remains focused on operational excellence as well as improving customer outcomes.

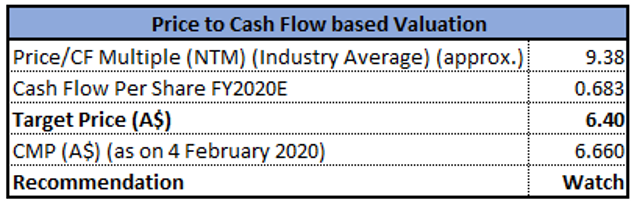

Valuation Methodology: P/CF based Multiple Approach

P/CF-Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Debt to equity multiple of the company stood at 0.28x in 1H FY19 as compared to the industry median of 0.32x. Gross margin and EBITDA margin of the company stood at 96.8% and 46.9% in 1H FY19, as compared to the industry median of 40.2% and 27.0%, respectively. We have valued the stock using P/CF based relative valuation method and arrived at a target price, which is offering correction of lower single-digit (in percentage terms). Hence, considering the expected correction in valuations, in combination with the full year 2019 earnings release, which has been scheduled to be released on 19th February 2020, we have a watch stance on the stock at the current market price of $6.660 per share, up 0.301% on 4th February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

.jpg)

Please wait processing your request...

Please wait processing your request...