.png)

Stocks’ Details

National Australia Bank Limited

RBNZ Restrict BNZ To Pay Ordinary Dividends Amid COVID-19 Crisis: National Australia Bank Limited (ASX: NAB), one of Australia’s leading bank, is involved primarily in banking services, credit and access card facilities, international banking, investment banking, wealth management services, leasing, housing and general insurance, funds management and custodian, trustee and nominee services. As at 6 April 2020, NAB had a market capitalization of around ~$46.61 billion. Recently, Reserve Bank of New Zealand (RBNZ) restricted its regulated banks including NAB’s wholly-owned subsidiary Bank of New Zealand (BNZ), to pay dividends on ordinary shares, regardless of a bank’s capital ratio, to further support the stability of the financial system during this period of economic uncertainty. NAB does not expect this restriction to have a material impact on NAB’s Level 1 capital position and its Level 2 capital ratio.

Q1FY20 Update: In the first quarter of FY20, NAB reported unaudited statutory net profit of $1.7 billion with cash earnings of $1.65 billion. As at 31 December 2019, the bank had a CET ratio of 10.6%, Leverage ratio (APRA basis) of 5.6%, and Net Stable Funding Ratio (NSFR) of 112%.

.png)

CET1 Ratio (Source: Company Reports)

Recent Update: NAB recently converted its 7.5 million Capital Notes (NCN) into fully paid ordinary shares and issued 35,140,972 fully paid ordinary shares in connection with the conversion at a price of $21.34 per share. On 23 March 2020, the bank announced that it has successfully completed the resale of all NAB Capital Notes. Following the resale, $750 million of NCN were converted into 35,140,972 fully paid ordinary shares in the hands of the nominated purchaser, adding approximately 18 basis points of Common Equity Tier 1 capital on a Level 2 basis. NAB recently became a substantial holder of Perenti Global Limited by holding 6.664% of the voting rights in the company.

Valuation Methodology: Price to earnings Multiple Based Relative Valuation

.png)

Price to Earnings Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: NAB is of the view that it is well-placed to provide the necessary support with strong capital and liquidity positions. The stock of NAB has corrected by 36.81% in the last three months and is trading near to its 52-week low price of $13.195, providing investors an opportunity for accumulation. At a current market price, NAB has an annual dividend yield of 10.63%. In FY19, NAB reported an efficiency ratio of 57.2% which is higher than the industry median of 53.7%. We have valued the stock using price to earnings valuation method and have arrived at a target price of lower double-digit upside (in % terms). For the purpose, we have taken peers like Bank of Queensland (ASX: BOQ), Westpac Banking Corp (ASX: WBC), Commonwealth Bank of Australia (ASX: CBA), etc. Considering, the bank’s strong capital and liquidity positions, current trading levels, and valuation, we give a “Buy” recommendation on the stock at the current market price of $16.470, up by 5.442% on 6 April 2020.

Bank of Queensland Limited (ASX: BOQ)

Withdrawal of FY20 Guidance Amid COVID-19 Crisis: Bank of Queensland Limited (ASX: BOQ) is one of Australia's leading regional banks which provide banking, financial and related services. On 30th March 2020, BOQ withdrew its FY20 guidance and outlook statements, due to the uncertainty surrounding COVID-19 impacts. However, BOQ remains focused on retaining the flexibility to respond to changing market dynamics. Through this period of disruption, BOQ intends to work with Federal government, State Governments and regulators to support its customers, employees and the wider community. BOQ is planning to release its H1 FY20 financial results 8 April 2020.

Strong Funding Position: BOQ’s capital position and funding remain strong, with a pro forma FY19 CET1 Ratio of 10.07%. BOQ believes that its funding position will be further enhanced by the provision of the RBA (Reserve Bank of Australia) term funding facility to support customers with new lending.

FY19 Results Highlights:In FY19, the bank’s statutory net profit after tax decreased by 11% from FY18 to $298 million, and cash return on equity reduced to 8.3%, with common equity tier one also lower at 9.04%. Over the year, the bank’s total lending grew by 937 million dollars, primarily driven by the Business Bank, with mortgages underperforming.

.png)

FY19 Results Summary (Source: Company Reports)

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation

.png)

Price to Earnings Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: BOQ currently has a strong balance sheet with solid capital and funding, and robust risk management. The stock of BOQ is currently trading near to its 52 weeks low price of $4.560, providing investors an opportunity for accumulation. We have valued the stock using price to earnings valuation method and have arrived at a target price of lower double-digit upside (in % terms). For the purpose, we have taken peers like Westpac Banking Corp (ASX: WBC), Commonwealth Bank of Australia (ASX: CBA) and National Australia Bank Ltd (ASX: NAB) etc. Considering the aforesaid facts, the bank’s strong capital position and its current trading levels, we give a “Buy” recommendation on the stock at the current market price of $5.070, up by 3.681% on 6 April 2020.

Steadfast Group Limited

Withdrawal of FY20 Guidance: Steadfast Group Limited (ASX: SDF) is a leading general insurance broker and an underwriting agency group in Australasia, with growing operations in Asia and Europe. On 25 March 2020, the company provided an update on COVID-19 impacts, wherein, it informed that in the first half of FY20 and in the first two months of second half, Steadfast Group has performed strongly. As a result of which, it expects FY20 results would be at the top end of FY20 guidance. However, due to the uncertainty around the COVID-19 impacts, the company has decided to withdraw its guidance for FY20.

H1FY20 Highlights: In the first half of FY20, SDF’s EBITDA grew by 27.5% to $108.9 million and its NPAT grew by 39.1% to $53.2 million. Over the period, the company’s underlying revenue increased by 29.6% to $414.4 million. In H1FY20, the company delivered 32% growth in gross written premium (GWP), driven by new Steadfast brokers and IBNA brokers joining the network, continued growth in authorised representative networks and organic growth of 6.5% across the portfolio.

.png)

Reconciliation of statutory NPAT to underlying NPAT (Source: Company Reports)

Valuation Methodology: P/E Multiple Based Relative Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the past six months, SDF’s stock price has declined by 34.79% on ASX. The stock is currently trading near to its 52 weeks low price of $2.320. In H1 FY20, SDF reported an EBITDA margin of 28.5%, higher than the industry median of 12.6%. We have valued the stock using price to earnings valuation method and have arrived at a target price with a correction of higher single-digit (in % terms). For the purpose, we have taken peers like IOOF Holdings Ltd (ASX: IFL), Challenger Ltd (ASX: CGF), Suncorp Group Ltd (ASX: SUN), etc. Considering the aforesaid facts and the uncertainty around the COVID-19 Impacts, we have a watch stance on the stock at the current market price of $2.330, down by 2.101% on 6 April 2020.

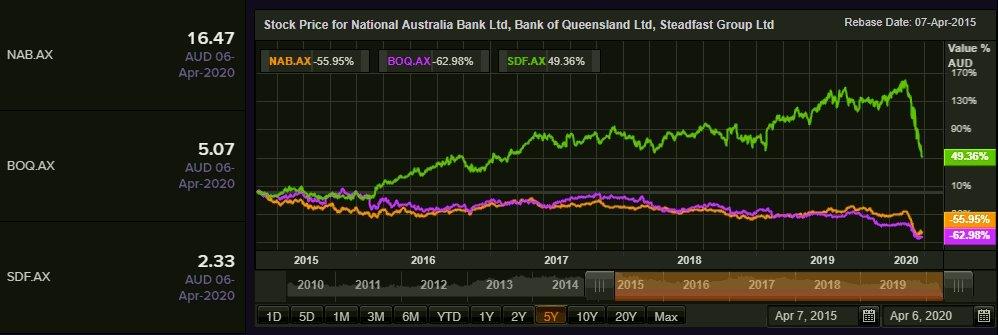

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...