Coca-Cola Amatil Ltd (ASX: CCL)recently reported a change in its segment reporting, which would be effective from January 1

st, 2014.The change in segment reporting is estimated to be approved during the August 20 board meeting, and would be implemented for the first half 2015 results which would be reported on the August 21

st, 2015. Investors should note the following changes in its reporting:

-

Alcohol & Coffee business: This segment will now constitute the Grinders coffee business, shifting from Australian Non-Alcohol Beverages. Alcohol business revenues would also be reported under this segment which is shifting from the Alcohol, Food & Services. Shane Richardson is the Managing Director for this Alcohol & Coffee business. Coca-Cola Amatil would not charge a corporate overhead to the segments, the corporate costs related to the Food and Services segment would be reported in a distinct segment. Indonesia’s Services business is consolidated into the Indonesian Non-Alcohol Beverage business, to streamline the parent company’s Coca-Cola acquisition of 29.4% equity interest in CCA Indonesia. Accordingly, this business would be shifting into Indonesian & PNG Non-Alcohol Beverage segment from Alcohol, Food & Services.

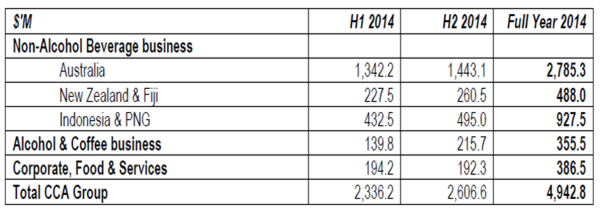

Coca-Cola Amatil’s full year results under new reporting segments (Source: Company Reports)

-

The group is introducing a new segment, Corporate, Food & Services which would include corporate assets and liabilities which were earlier reported under the segments. The segment would also comprise the assets and liabilities of the Food and Services businesses. Meanwhile, the assets and liabilities related to the Grinders and Alcohol is shifting to the Alcohol & Coffee segment. Indonesian Services business assets and liabilities is shifted to the Indonesia & PNG Non-Alcohol Beverage business from Alcohol, Food & Services.

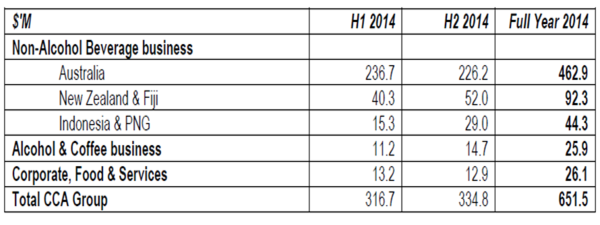

Coca-Cola Amatil’s EBIT before significant items under new reporting segments (Source: Company Reports)

Earlier Reporting Financial Highlights and Outlook

-

Coca-Cola’s 2014 fiscal results were lower than expected, as the total trading revenues reduced 1.9% to $4,942.8 million during FY14 from $5,036.4 million in FY13, impacted by Australian business as its revenues fell 3.9% on a year over year basis to $488 million. The total earnings before interest and tax witnessed more pressure falling 21.8% yoy to $651.5 million, affected from Australia and Indonesia & PNG segments which plunged 21.3% yoy and 65.2% yoy respectively. As a result, the group’s net profit after tax (before significant items) fell 25.3% to $375.5 million, as compared to 2013. But, the reported net profit after tax fell 240.6% yoy after the impact of significant item

CCL Daily Chart (Source - Thomson Reuters)

CCL Daily Chart (Source - Thomson Reuters)

-

Non-alcoholic beverages business represents 85.9% of the overall group’s revenues, with Australia contributing 66.7% of revenues while Indonesia contributes over 21.8%. But the Australian beverage business earnings reduced by 21.3% on a year over year basis, due to which the group undertook restructuring activities to gain its position back in the market. However, we believe that capturing further market share is quite challenging to CCL as Australian beverage business is a mature market with huge competition. The group’s Australian nonalcoholic beverages volumes also declined by 0.9% yoy in 2014, as consumers are preferring healthier substitutes with less sugar and calories. Accordingly, the group has improved its share in sports drinks by over four points enhanced by concrete marketing, while the energy drink share also rose by 5.5 points. Despite the group’s efforts in alternate healthier segments, their contribution to the overall business is relatively less and will not be able to offset the decline coming from the soft drinks business.

-

As a result, the shares of Coca-Cola Amatil have fallen 12.2% in the last three months as compared to 5.2% of the broader S&P/ASX 200, and delivered a negative year to date returns of 3.64%. Moreover, the group’s expansion efforts at CCA Indonesia might take another four to five years to offset the decline coming from its Australian business as CCA Indonesia is estimated to self-sustain its growth from operating cash flow by 2020. Tough market conditions, rising wages and weakening Rupiah might delay the Indonesian growth and its ability to generate positive cash flow hurting the stock further. Investors need to be cautious while investing in CCL in this challenging environment in Australia and obscure outlook on the group’s potential Indonesia traction. Despite the recent correction, CCL’s valuations looks expensive, and the stock is trading at a P/E of 25.2x relatively higher value as compared to its industry peers. Based on the foregoing, we reiterate our “Expensive” recommendation to the stock at the current levels of $8.54.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...