.png)

Stocks’ Details

Newcrest Mining Limited

Update on Joint Venture Exploration:Newcrest Mining Limited (ASX: NCM) is involved into the development, exploration, mining and sale of gold. The market capitalisation of the company stood at ~A$26.28 Bn as on 2nd August 2019. Recently, NCM has noted an announcement made by Encounter Resources Ltd in relation to joint venture exploration activities. It was mentioned that Newcrest is sole funding exploration activities throughout a series of joint ventures in the Tanami and West Arunta Provinces.

Heritage surveys have been wrapped up at Watts, Selby and Lewis joint ventures in June 2019.Newcrest-funded exploration activity, including Reverse Circulation and diamond drilling, would be completed within the period from August to November 2019. Additionally, Encounter Resources Ltd is completing initial validation activities at Phillipson Range and reclaiming 100% ownership. The following picture provides an overview of the key numbers for June 2019 quarter.

.png)

Gold Production and AISC (Source: Company Reports)

Future Prospects: The company’s approach to growth includes organic growth and greenfield exploration, early entry partnerships with explorers and M&A. However, it would be considered when there will be an opportunity to create value via application of strong and unique technical capabilities.

Stock Recommendation:The company reported a gross margin and EBITDA margin of 26.8% and 41.4% in 1H FY19 against the industry median of 41.6% and 34.6%, respectively. It posted a net margin of 13.7% for the same time period as compared to the industry median of 13.0%. Coming to the stock’s past performance, it had provided returns of 16.49% and 47.23% in the time period of one month and three months, respectively. As per ASX, the stock of Newcrest Mining Limited is trading closer to 52-week higher levels of $36.79 with PE multiple of 58.24x. Hence, considering the above-stated facts and current trading levels, we advise the investors to avoid the stock at the current market price of $36.660 per share (up 7.193% on 2nd August 2019), and wait for better entry levels.

Treasury Wine Estates Limited

Caution on Wine Australia Export Data:Treasury Wine Estates Limited (ASX: TWE) is into the international wine business having a portfolio of luxury, premium, and commercial wines. The market capitalisation of the company stood at ~A$12.61 Bn as on 2nd August 2019.Recently, the company has noted the release of Wine Australia export data for the March 2019 quarter. The company reiterated its caution against using the data set as a direct read through to TWE’s trading performance. It was also mentioned that the use of short-term trade export and import data might not provide a true picture of the company’s underlying trading performance in the Asia region as the Wine Australia export data does not consider key structural differences in the TWE’s business model, the premium mix of the company’s portfolio, nor variability in its export shipment profile. The following picture provides an idea of the company’s total assets and total liabilities:

.png)

Balance Sheet for 1H FY19 (Source: Company Reports)

What to Expect: The company mentioned that the changes in US route-to-market are going well and are on track. The company is expecting EBITS growth rate of around 15% to 20% for FY20, which is in accordance with consensus. However, it reiterated guidance for around 25% reported EBITS growth in FY19.

Stock Recommendation: Treasury Wine Estates Limited reported return on equity of 6.2% in 1H FY19 as compared to the industry median of 5.8%, which represents that TWE is giving feasible returns to its shareholders against the broader industry. It posted a current ratio of 2.55x in 1H FY19 in comparison to the industry median of 1.52x. This implies that Treasury Wine Estates Limited is well-placed to address its short-term obligations. With respect to the stock’s past performance, it generated returns of 12.98% and 1.52% in the time span of one month and three months, respectively. Hence, considering the above-stated facts and decent outlook, we give a “Buy” recommendation on the stock at the current market price of A$17.410 per share (down 0.741% on 2nd August 2019).

Sydney Airport

Traffic Performance for June 2019:Sydney Airport (ASX: SYD) is a large-cap company with the market capitalisation of ~A$19.05 Bn as on 2nd August 2019. Recently, the company, via a release dated 19th July 2019 updated the market with traffic performance for June 2019. The company stated that the number of international passengers travelling through Airport in June rose by 1.1% to 1.3 million passengers on a pcp basis.

There was a decline of 1.6% to 2.1 million in domestic passengers due to capacity reductions in combination with subdued load factors.Adding to that, it was mentioned that over 3.4 million passengers in June 2019 have passed through Sydney Airport, reflecting a fall of 0.5% on June 2018. The company reported revenue and net operating receipts of $1,584.7 Mn and $860.9 Mn in FY18 and it posted EBITDA amounting to $1,282.6 Mn.

.png)

Traffic Performance (Source: Company Reports)

Future Aspects:The company expects to begin paying cash income tax from CY 2022. Additionally, the future cash tax payments would give rise to franking credits and these would be distributed to eligible investors. The company is expecting distribution of 39 cents per stapled security in 2019. It provided guidance in relation to capital expenditure for 2019-2021 of $0.9Bn -1.1Bn.

Stock Recommendation: The company reported a net margin of 23.4% in FY18 against the industry median of 28.1%. The return on equity stood at 103.3% as compared to the industry median of 10.7%, which represents that the company is providing better returns to its shareholders. Recently, the company notified that it will release 1HFY19 results on 15 August 2019 before market open.

On the stock performance front, it witnessed a rise of 7.29% and 13.46% in the time span of one month and three months, respectively. As per ASX, the stock is trading closer towards the 52-week high price of $8.690, which increases the probability for a correction in the near term. Hence, considering the above-stated facts and current trading levels, we give an “Expensive” rating on the stock at the current market price of A$8.680 per share (up 2.844% on 2nd August 2019).

Bank of Queensland Limited

Disclosures of Basel 3 Pillars: Bank of Queensland Limited (ASX: BOQ) is in the business of providing banking and financial related services. Recently, the bank, via a release dated 26th July 2019 announced Basel III Pillar 3 disclosures. The bank stated that its capital management strategy is targeting to ensure that adequate capital levels are maintained in order to protect deposit holders. Adding to that, it was mentioned that its capital is measured and managed in accordance with Prudential Standards issued by the Australian Prudential Regulation Authority (or APRA). The capital management plan of the bank is updated annually and submitted to the Board of the bank for approval. The CET1 capital ratio of the bank stood at 8.9% as at 31st May 2019 in comparison to 9.3% as at 28th February 2019 and it posted total capital ratio of 12.3% as at 31st May 2019.

Additionally, the Board of the bank has set the CET1 capital range to be between 8.25% and 9.5% and the Total Capital target range to be between 11.75% and 13.5%. The following picture provides an idea of financial performance of the bank:

.png)

Profit Results (Source: Company Reports)

What to Expect: As per the Chairman’s half year letter, the bank has undertaken a conservative approach to managing the bank by maintaining high risk standards. The bank is making significant improvements in its lending processes and digital platforms which would be delivering better outcomes for its customers.

Stock Recommendation: The bank’s cash net interest margin stood at 1.94% in 1H FY19, which can be considered at decent levels. The efficiency ratio of the bank stood at 55.3% in comparison to the industry median of 60.5%. Coming to the stock performance, it produced returns of -2.75% and 3.49% in the time span of one month and three months, respectively. Hence, considering the above-stated facts and decent outlook, we give a “Buy” recommendation on the stock at the current market price of A$9.190 per share (down 0.863% on 2nd August 2019).

Suncorp Group Limited

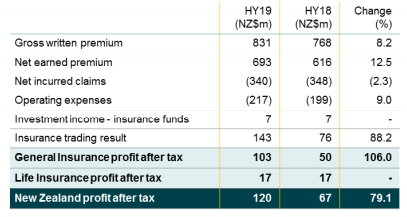

Resolution for Shareholders:Suncorp Group Limited (ASX: SUN) is into the provisioning of banking, insurance, wealth and other financial solutions to the retail, corporate and commercial sectors. The market capitalisation of the company stood at ~A$17.48 Bn as on 2nd August 2019. Recently, the company via a release dated 26th July 2019 announced shareholder resolutions for the AGM. The company is going to conduct its Annual General Meeting on 26th September 2019, wherein the company will present the following resolution to shareholders:

1. Amendment to the Constitution (Special Resolution)

2. Fossil Fuel Exposure Reduction Targets (Contingent/ Advisory Resolution)

In another update, the company with the help of a release confirmed that it received a representative proceeding filed in the New South Wales Supreme Court against its wholly owned subsidiary Suncorp Portfolio Services Limited.The following picture provides an idea of the company’s performance:

Financial Performance (Source: Company Reports)

Future Prospects: The company has a diversified General Insurance and Life business, along with prominent market positions which can attract the attention of market players. SUN has a well-established program for addressing regulatory change and it holds a positive outlook with strong reinsurance protection and clear strategies to leverage key relationships and grow its business.

Stock Recommendation: The company posted an asset-to-equity ratio of 7.30x in 1H FY19 against the industry median of 4.72x. With respect to the stock’s past performance, it produced returns -0.67% and 2.19% in the time span of three months and six months, respectively. Hence, considering the above-stated facts and current trading levels, we maintain our “Hold” recommendation on the stock at the current market price of A$13.390 per share (down 0.52% on 2nd August 2019).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...