.png)

Stocks’ Details

Bubs Australia Limited

Strong Growth Trajectory: Bubs Australia Limited (ASX: BUB) is engaged in the manufacturing of infant milk formula. The market capitalisation of the company stood at $406.21 Mn as on 26th February 2020. The company recently released its results for 1H FY20, wherein, it stated that it experienced a solid growth trajectory during the period. The company reported gross revenue amounting to $28.75 million with a rise of 37% over 1H FY19. This growth has been primarily driven by Bubs® Infant Formula, which delivered the most material improvement with a gross profit margin of 41% against 28% in June 2018.

Moreover, the company has inked a new supply agreement with Woolworths. The company expects that this contract will be beneficial for domestic revenues. As per the terms of the agreement, all three stages of Bubs Organic® Grass Fed Infant Formula are to be ranged nationally in 700 stores of Woolworths.

.png)

Financial Overview (Source: Company Reports)

Future Aspects: Bubs is well-positioned to continue to grow its top-line in 2H FY20 on the back of a robust balance sheet with cash reserves of $39.1 million and a strong inventory position to fulfill future demand.

Valuation Methodology:P/BV Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Bubs is focused on pursuing its strategic goals for delivering profitable and scalable sustainable growth. It is continuously focused on operational and capital management as well as improving profit margins. We have valued the stock using P/BV- based relative valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering the solid growth trajectory in 1H FY20, the recent agreement with Woolworths and focus for the future, we give a “Buy” recommendation on the stock at the current market price of $0.705 per share, down by 2.759% on 26th February 2020.

Woolworths Group Limited

Sales and Earnings Growth in all Businesses: Woolworths Group Limited (ASX: WOW) is engaged in food, general merchandise and specialty retailing via chain store operations. The market capitalisation of the company stood at $52.78 Bn as on 26th February 2020. For 1HFY20, all businesses of the company managed to deliver sales and earnings growth despite a volatile trading environment. Sales of the group from continuing operations witnessed a rise of 6.0% and EBIT from continuing operations before significant items surged by 11.4%.

The Australian Food segment of the company witnessed EBIT growth of 8.0%, primarily as a result of strong sales growth. The company reported a profit for the first time since FY16 in BIG W with EBIT amounting to $50 million. This has been fueled by sales growth of 2.8% in a challenging market, along with improved category mix and good cost control.

.png)

Reported 1H FY20 Results (Source: Company Reports)

Outlook: The company is optimistic about its plan in 2H FY20 despite a slow start to Q3 due to a volatile consumer and natural environment. The company is expecting higher food inflation in Australian and New Zealand Food.

Stock Recommendation: Gross margin and EBITDA margin of the company stood at 29.1% and 6.3% in FY19 as compared to the industry median of 26.2% and 5.8%, respectively. Debt to equity multiple of the company stood at 0.30x in FY19 against the industry median of 0.42x. Return on equity of the company stood at 14.4% in FY19 as compared to 13.3% of the industry median. The company has an EV/Sales multiple of 0.9x as compared to the industry median (Consumer Non-Cyclicals) of 1.8x on TTM basis. Therefore, in light of decent margins against the industry, deleveraged balance sheet and returns to shareholders, we maintain a “Hold” rating on the stock at the current market price of $40.730 per share, down by 2.676% on 26th February 2020.

Michael Hill International Limited

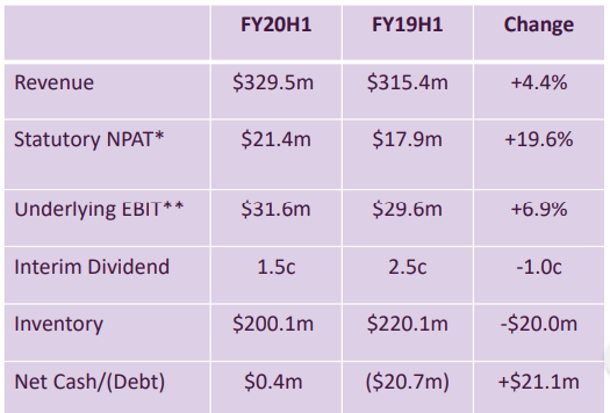

Improvement in EBIT: Michael Hill International Limited (ASX: MHJ) is engaged in the retail sale of jewellery and related services in Australia, New Zealand and Canada. The market capitalisation of the company stood at ~$221.03 Mn as on 26th February 2020. The company has recently appointed Richard Amos as the Company Secretary. The company reported statutory net profit after tax amounting to $21.4 Mn for 1H FY20 (26 weeks ended 29th December 2019) with a rise of 19.6%. During the same time period, underlying earnings before interest and tax pre-AASB 16 Leases stood at $31.6 million, reflecting an improvement of 6.9%. This improvement has been driven by a rise in Group operating revenue and targeted reduction in costs.

Financial Overview (Source: Company Reports)

Productivity Growth for FY20: With respect to Canada, the company would continue to focus on the productivity growth of the retail segment over the remainder of FY20 and beyond. The company is also focused on business and retail fundamentals, including the new incentive scheme, productivity, digital-first, etc.

Stock Recommendation: Over a period of 6 months, the stock generated positive returns of 16.33%. At the end of 1HFY20, the company stood in a strong financial position along with disciplined cost management, debt-free position as well as lower inventory levels. The Board of the company declared an unfranked interim dividend amounting to 1.5 cps. Thus, considering the strong financial position and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $0.580 per share, up by 1.754% on 26th February 2020.

Apollo Tourism & Leisure Ltd

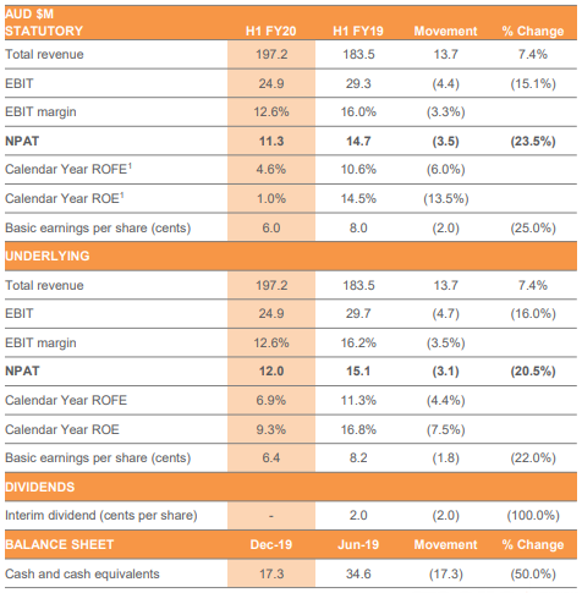

Growth in Revenue during 1H FY20: Apollo Tourism & Leisure Ltd (ASX: ATL) is involved in the sale and renting of recreational vehicles. The market capitalisation of the company stood $49.33 Mn as on 26th February 2020. For 1HFY20, the company reported revenue amounting to $197.2 Mn with a rise of 7.4% over pcp. This growth has been achieved despite the global events, which are impacting the RV industry. Underlying net profit after tax stood at $12.0 Mn, delivering a solid result amidst weaker market conditions. This reflects that the company is moving in the right direction after a transitional financial year.

Financial Metrics (Source: Company Reports)

NPAT Guidance for FY20: The company would be reporting a loss in 2HFY20 as a result of current challenging and uncertain trading conditions, which have been caused by the bushfires, Coronavirus (COVID-19), as well as ongoing margin pressure on RV sales. However, for FY20, it is expecting Underlying NPAT in the ambit of $8 Mn - $9 Mn.

Stock Recommendation: The company stated that during FY20, it will focus on the expansion of retail sales outlets in the USA and will continue to integrate acquisitions and implement growth strategies, going forward. During the span of one month and three months, the stock of ATL has corrected 30.26% and 33.75%, respectively. Therefore, considering the impact of global events on the upcoming results and correction in stock, we have a watch stance on the stock at the current market price of $0.340 per share, up by 28.302%, taking cues from the release of 1HFY20 results. We suggest investors to wait for further catalysts to drive the stock.

Comparative Price Chart (Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

.jpg)

Please wait processing your request...

Please wait processing your request...