.png)

Stocks’ Details

Bubs Australia Limited

Major Supply Agreement with Coles for Organic Formula: Bubs Australia Limited (ASX: BUB) offers a great range of organic baby food, goat milk infant formula products, the adult goat milk powder products, and fresh dairy products. As on 07 May 2020, the market capitalization of the company stood at $532.28 million. The company has recently entered an agreement with Coles Supermarkets Australia, wherein it will distribute Bubs Organic® Grass Fed Infant Formula to 482 supermarkets. This will support portfolio-wide growth in the company’s domestic volume.

Record Quarterly Revenue: The company demonstrated the strength of its business model during the third quarter ended 31 March 2020. It delivered positive operating cash flow of $2.3 million with record quarterly revenue of $19.7 million.

.png)

Quarterly Cash Flows (Source: Company Reports)

What to Expect: The company remains agile and can quickly respond to this fast-moving situation, with operating flexibility from its vertical supply chain and strong balance sheet position. BUB is fully focused on ensuring that its integrated supply chain is responsive to the increased demand.

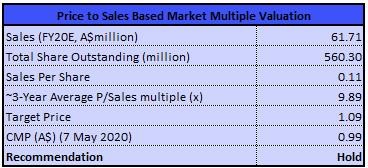

Valuation Methodology: Price to Sales Based Market Multiple Valuation (Illustrative)

Price to Sales Based Market Multiple Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of BUB gave a return of 30.14% in the last three months and a return of 42.86% in the past one month. During 1H20, gross margin of the company stood at 13.6%, and current ratio of the company was 3.03x. The company is upholding a solid supply chain with minimal disruption to its manufacturing operations. Considering the decent returns from stock, strong financial position, and modest outlook, we have valued the stock using Price to Sales based market multiple valuation method and have arrived at a target price with an upside of high single-digit (in percentage terms). Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $0.990, up by 4.211% on 7 May 2020.

Synlait Milk Limited

Decent Increase in Revenue: Synlait Milk Limited (ASX: SM1) is a dairy manufacturer focused on supplying higher value dairy products to leading milk-based health and nutrition companies. As on 7 May 2020, the market capitalization of the company stood at $1.17 billion. During 1H20, the company witnessed a growth of 22% in sales of consumer packaged infant formula and reported an increase of 19% in revenue to $559 million. In the same time span, EBITDA was in line with 1H19 and stood at $67.6 million, with NPAT of $26.2 million.

.png)

1H20 Financial Highlights (Source: Company Reports)

Synlait Uniting against COVID-19: During the times of global pandemic, SM1 is operating as an essential service. It has been entrusted with a responsibility to help feed New Zealanders. The company is not facing any operational impact and is managing risks through strong relationships with raw material suppliers and logistics partners. The company has progressed well on its material customer opportunities which are expected to diversify the company’s portfolio and will fill up new facilities. SM1 has a strong customer pipeline and has made strong progress towards its long-term strategy.

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

.png)

EV/EBITDA Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of SM1 gave a negative return of 4.39% in the past one month. During 1H20, gross margin of the company stood at 14.8%, and net margin was 4.7%. Considering the decent financial performance, the resilience of the business in an uncertain environment and modest outlook, we have valued the stock using EV/EBITDA multiple based illustrative relative valuation approach and arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $6.650, up by 1.682% on 07 May 2020.

Coles Group Limited

Decent Increase in Quarterly Sales: Coles Group Limited (ASX: COL) is an Australian retailer of fresh food, groceries, household goods, liquor, fuel, and financial services via stores and online. As on 7 May 2020, the market capitalization of the company stood at $20.44 billion. The company has recently released its quarterly results for the period ended 29 March 2020 wherein it reported an increase of 12.9% in total sales to $9.2 billion. In the same time span, the company introduced over 260 ‘Own Brand’ products and refreshed websites across all three Liquor banners. This delivered a growth of 34% in online sales growth.

.png)

Growth in Quarterly Sales (Source: Company Reports)

Future Expectations and Growth Opportunities: The company has seen an increase in basket size, which was partially offset by a decline in transactions driven by social distancing measures. In the coming period, COL expects an elevated cost base because of the additional investment and increased sales of liquor. The company expects gross operating capex to be in the range of $750 million to $850 million.

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of COL gave a return of 2% on the YTD basis. During 1H20, Return on Equity of the company stood at 16.6%, higher than the industry median of 9.3%. This indicates that the company is well managing the capital of its shareholders and is capable of generating profits internally. Considering the returns, decent financial performance, and positive outlook, we have valued the stock using the price to cash flow multiple based illustrative relative valuation approach and arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $15.230, down by 0.587% on 7 May 2020.

Myer Holdings Limited

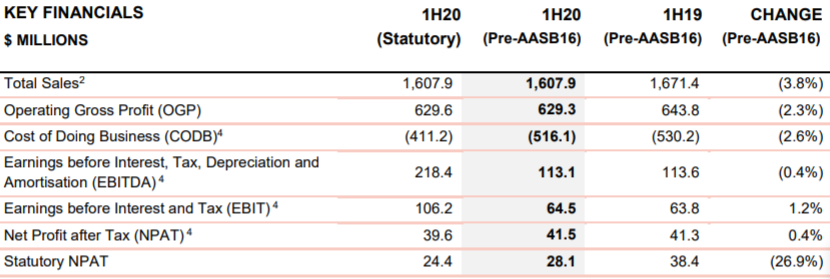

Solid Result Despite Macro Headwinds: Myer Holdings Limited (ASX: MYR) operates a portfolio of 66 department stores across Australia. As on 7 May 2020, the market capitalization of the company stood at $156.04 million. During 1H20, total sales of the company stood at $1.607.9 million, and online sales went up by 25.2% to $168.2 million. In the same time span, operating gross profit margin increased by 62 basis points to 39.14% and the cost of doing business went down by 2.6% to $516.1 million. The reduction in costs reflects simplification of the business, including the enhanced in-store staffing model, reduced store occupancy and improved processes.

1H20 Financial Highlights (Source: Company Reports)

Future Expectations: The company has a clear plan to address the underperformance in women’s wear. It has various opportunities which are likely to improve productivity and further reduce costs, particularly in the areas of store occupancy, factory to customer and fulfilment for both stores and online. The company is operating through its online stores and has performed strongly since the closure of physical stores. MYR is anticipating that the current challenging environment will continue in the second half, and the ongoing impact of coronavirus on store traffic remains uncertain.

Stock Recommendation: As per ASX, the stock of MYR gave a return of 35.71% in the past one month and is trading close to its 52-weeks’ low level of $0.083. During 1H20, EBITDA margin of the company witnessed an improvement over the previous half and stood at 7.8%. In the same time span, ROE of the company stood at 5%. On TTM basis, the stock is trading at an EV/Sales multiple of 0.7x, lower than the industry median (Consumer Cyclicals) of 1.2x. Considering the current trading levels, returns in the past one month, lower EV/Sales multiple, and positive outlook, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.20, up by 5.263% on 07 May 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...