.png)

Stocks’ Details

Woolworths Group Limited

Strong Sales Momentum Across the Group: Woolworths Group Limited (ASX: WOW) is engaged in retail operations across Australian Food, Endeavour Drinks, New Zealand Food, BIG W and Hotels. The AGM and EGM of the company are to be held on 16th December 2019. The company has recently declared the results of its first quarter, wherein it stated that the Group sales from the continuing operations went up by 7.1% to $15.9 billion. In Australian Foods, growth in sales was mainly driven by the success of Lion King Ooshies, Discovery Garden and the continued growth in Online sales. However, in Endeavour Drinks, both BWS and Dan Murphy’s delivered comparable growth across all key categories. Growth in the Apparel category and the new brand platform led the growth in Big W sales.

.png)

First Quarter Sales (Source: Company Reports)

Transformation Update of Endeavour Group: The company released a release about the Endeavour Group transformation update, in which it was mentioned that restructure is the first stage of Endeavour Group Transformation. This involves an internal reorganisation through which assets and liabilities relating to the WOW Drinks Business, as well as WOW’s 75% ownership interest in ALH will be transferred into a distinct legal entity within Woolworths Group to create Endeavour Group. Following the restructure, WOW will seek to complete the ALH Merger, post which Endeavour Group will be 85.4% owned by WOW and 14.6% owned by Bruce Mathieson Group. The company intends to separate the newly formed Endeavour Group from Woolworths Group by way of a demerger or other value accretive alternative.

What to Expect: The company expects opportunities to unlock value for its customers and shareholders in FY20 despite an uncertain consumer environment and input cost pressures. It stated that improved fresh experience, renewals and range localisation will support the sales growth in Australian Food. It was added that there are expectations of a reduction in losses as turnaround of BIG W continues and the unprofitable stores are closed.

Stock Recommendation: As per the ASX, stock of WOW gave a return of 34.07% on YTD basis and a return of 8.53% in the last 3 months. The stock of WOW is trading close to the 52-week higher levels. During FY19, EBITDA margin of the company stood at 6.3%, higher than the industry median of 5.8%. ROE of the company stands at 14.4% as compared to the industry median of 13.3%. Thus, considering the higher returns, High ROE and EBITDA margin, we recommend to “Hold” the stock on the current market price of $39.080, up by 1.401% on November 22, 2019.

Treasury Wine Estates Limited

Appointment of CEO: Treasury Wine Estates Limited (ASX: TWE) is an international wine business with a portfolio of luxury, premium and commercial wines. Recently, Mr. Clarke has been granted 335,557 performance rights under the F20 Long Term Incentive Plan.The company has recently announced that Michael Clarke intends to retire from the role of Managing Director and Chief Executive Officer in the first quarter of fiscal 2021, and that Tim Ford will be appointed to the role of CEO, effective from the retirement of Mr Clarke.

Significant Increase in Revenue: In the recently held AGM of the company, the top management of the company stated that Net Sales Revenue increased by 17% over the prior year to $ $2,831.6m and Group EBITS increased by 25% to $662.7 million, delivering a five-year CAGR growth of 30%. Owing to strong financial results in FY19, TWE was pleased to declare a fully franked final dividend of 20 cents per share, which brings the total dividend for F19 to 38 cents per share, up 19% on the prior year.

.png)

Net Sales Revenue (Source: Company Reports)

Stock Recommendation: The company reaffirmed the guidance for reported EBITS growth for FY20 and expects it to be between 15% to 20%. It also expects that global category fundamentals will remain attractive, particularly at premium price points in the coming future. As per the ASX, the stock of TWE gave a return of 30.79% in the past one year and a return of 10.33% in the last one month. During the year, net margin of the company stood at 14.6%, higher than the industry margin of 8.3%. This indicates that the company is efficiently managing its costs and is able to convert its revenue into profits. Considering the EBIT growth guidance, higher net margin, high returns, expectation that global category fundamentals would be attractive, and decent five-year CAGR in Group EBITS, we recommend a “Hold” rating on the stock at the current market price of $18.690, up by 0.809% on November 22, 2019.

Coca-Cola Amatil Limited

Improvement in Free Cash Flow: Coca-Cola Amatil Limited (ASX: CCL) is one of the leading bottlers and distributors of non-alcoholic and alcoholic ready-to-drink beverages. The company declared a dividend of 25 cents per share on ordinary fully paid shares, which was paid on October 9, 2019. For the half year, the company reported a revenue growth of 5.2% and statutory earnings before interest and tax (EBIT) of $273.5 million, up 4.7%. The company’s free cash flows improved by $86.2 million from $129m in HY18 and in HY19, the figure stood at $215.2 million in HY19. This was mainly due to the increased interest income, reduction in tax payments in Australia, decrease in working capital, offset by the impact of resin pre-payments in Indonesia and reduced capital expenditure.

.png)

Free Cash Flow (Source: Company’s Report)

What to Expect: CCL’s Australian Beverages business is well-positioned for growth in the upcoming year with the completion of the additional $10 million of investments in its Accelerated Australian Growth Plan. CCL also expects to deliver growth in New Zealand & Fiji, Papua New Guinea and Alcohol & Coffee in line with the shareholder value proposition. It also expects an EBIT loss of approximately $12 million in Corporate & Services. The company is targeting a medium-term dividend payout ratio of over 80%. However, the group capex has been anticipated to be around $250 million in 2019 and $300 million in 2020.

Stock Recommendation: As per the ASX, the stock of CCL gave a return of 3.91% in the past 3 months and a return of 11.83% in the past one month. The stock of CCL is trading close to its 52-week higher levels. Current ratio of the company stands at 1.53x, higher than the industry median of 1.49x. This indicates that the company is sufficiently liquid and is capable to pay off its liabilities with its current assets.In terms of valuation, the stock is trading at a P/E multiple of 27.870x. On the backdrop of high returns, high current ratio along with the modest outlook, we give a “Hold” rating on the stock of CCL at the current market price of $11.440, up by 0.351% on November 22, 2019.

The A2 Milk Company Limited

Synlait and A2M Extend Supply Agreement: The A2 Milk Company Limited (ASX: A2M) is a premium branded dairy nutritional company focused on products containing the A2 beta-casein protein type. Recently, Synlait Milk Limited renegotiated the aspects of its comprehensive manufacturing and supply arrangements with The a2 Milk Company. It was also added that the changes reinforce the companies’ long-term partnership. As per the release, the supply agreement for a2 Platinum® and other nutritional products, which was announced on July 3, 2018, provided for the minimum term of 5 years, with the rolling 3-year term from August 1, 2020.

The primary components of revised agreement include: 1) a two-year extension to the term of the agreement, effectively providing for the new minimum term to, at the earliest, 31 July 2025, 2) an increase in volume of the nutritional products over which Synlait already has exclusive supply rights, 3) increased committed production capacity from Synlait, and 4) pricing terms which reflect commitment on the part of both companies to an ongoing market-competitive pricing regime. The company in its recent AGM stated that the revenue and EBITDA of the company went up to NZ$1,304.5m and NZ$413.6m from NZ$922.7m and NZ$283m in FY18, respectively. This increase resulted the basic EPS to rise to $39.3 cents from $27 cents in FY18.

.png)

Financial Performance (Source: Company Reports)

What to Expect: The company anticipates strong revenue growth across key regions, supported by brand and marketing investment in China and the US and the development of both capability and infrastructure to support in-market execution. A2M also expects its EBITDA margin to be in between 29-30% and the gross margin is expected to benefit from the improvement in price yield and reduction in COGS (cost of goods sold). For 1H20, it anticipates revenue to be in the range of $780 million to $800 million.

Stock Performance: As per the ASX, the stock of A2M gave a negative return of 7.53% in the past 6 months but a positive return of 14.20% in the past one month. The stock is trading towards its 52-week high of $17.300. During the time span from FY15 to FY19, the company witnessed a CAGR growth of 70.37% in revenue and a CAGR growth of 90.32% in gross profit over the same period. EBITDA margin of the company stands at 32.3%, higher than the industry median of 12.5%. During the year, ROE of the company stood at 42.8% as compared to the industry median of 12.8%.

Considering the CAGR growth in revenue and gross profits, high ROE and EBITDA margin, modest outlook and decent financial performance, we recommend a “Buy” rating on the stock at the current market price of $13.990, up by 1.157%, on November 22, 2019.

Metcash Limited

Increase in EPS to 22.6 Cents: Metcash Limited (ASX: MTS) is a wholesaler to independent retailers in food, grocery, liquor, hardware and automotive industries. The company has recently announced that 7-Eleven will not be renewing the current supply agreement with MTS following its conclusion on 12 August 2020. Total Convenience annual sales of the company to 7-Eleven are ~$800m, comprising predominantlylower margin tobacco sales.In the recently held AGM of the company, the top management stated that the Board determined to pay a final dividend of 7.0 cents per share, bringing total dividends for the year to 13.5 cents per share. During the year, Underlying profit after tax for the year went down by 3% to $ $210.3m, but underlying earnings per share increased by 1.8% to 22.6 cents, reflecting the benefit of the share buy-back.

.png)

Financial Performance (Source: Company Reports)

What to Expect: The company aims to cut the costs by offsetting the impact of inflation. While the market remained highly competitive, there was a continued improvement in the sales trajectory through the first quarter of FY20.

Stock Recommendation: As per the ASX, stock of MTS gave a return of 18.91% on YTD basis and a return of -0.35% in the past one month. During the time span from FY15 to FY19, the company witnessed a CAGR of 4.24% in gross profit. During the year, ROE of the company stood at 15%, higher than the industry median of 13.3%. Considering the returns, CAGR in gross profit, high RoE and decent outlook, we recommend a “Buy” rating on the stock at the current market price of $2.830, down by 6.908% on November 22,2019, owing to non-renewal of current supply agreement with 7-Eleven.

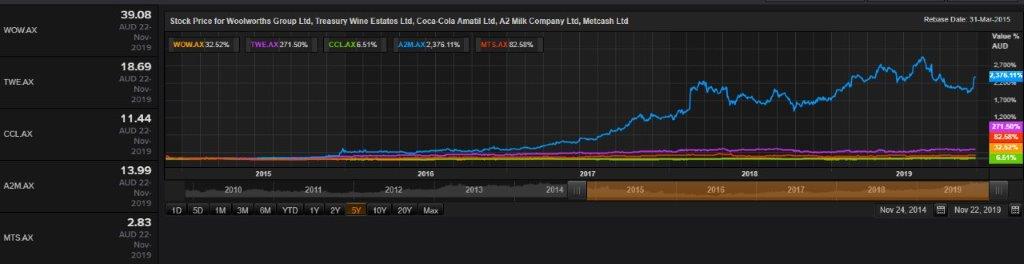

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...