CSL Limited

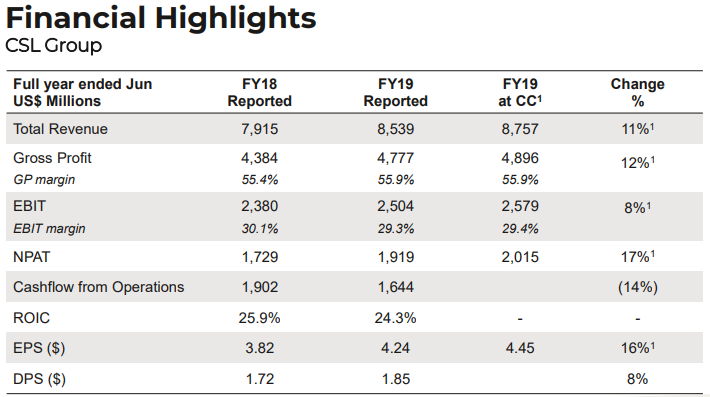

Decent Growth in NPAT:CSL Limited (ASX: CSL) is in the business of research, manufacturing, development, marketing and distribution of biopharmaceutical and allied products. The market capitalisation of the company stood at ~A$112.73 Bn as on 16th October 2019. When it comes to financial performance, the company stated that FY19 has been a strong year with reported net profit after tax of $1,919 Mn with a rise of 17% at CC basis and revenue witnessed an increase of 11% at CC basis. This primarily implies (1) continued strong growth in immunoglobulin and albumin therapies, (2) high patient demand for specialty products Haegarda & Kcentra,and (3) successful evolution of the haemophilia therapies portfolio.

On the operational front, the company stated that its largestfranchisee, the immunoglobulin portfolio, has been performing well, with sales growth of 23% and 22% in Privigen® and Hizentra®, respectively.CSL added that its business of Seqirus influenza vaccines has been delivering on strategy and is well-positioned in the market place with a production process innovation and differentiated product portfolio. In the second half of FY19, the Albumin sales into China made a strong resurgence. The global albumin sales witnessed a growth of 15% against the prior year. The following picture depicts an idea of dividend dates for the financial year 2020:

Key Dividend Dates (Source: Company Reports)

What to Expect: The company stated that the demand for its plasma and recombinant products continues to be decent. It anticipates to again outpace the market in growing the plasma collections and plan to open approximately 40 new collection centers in FY20. It added that Seqirus is anticipated to continue to perform well and deliver in accordance with the prior guidance, benefiting from product differentiation and process improvement. The company expects net profit after tax for FY20 to be in the ambit of around $2,050 Mn - $2,110 Mn at a constant currency basis, which represents a growth in the range of 7-10% in comparison to FY19. This growth considers the one-off financial headwind of transitioning to a new model of direct distribution in China. The company’s focus for the long-term revolves around the strategic pillars, i.e., (1) people and culture, (2) growth, (3) efficiency, and (4) public health.

As previously announced in June, the company would be transitioning to a direct distributor model in China, taking the distribution into line with its global operating model for major markets. This will have a one-off financial effect on FY20 albumin sales, which are anticipated to reduce by around $340 Mn - $370 Mn.

Stock Recommendation:The asset to equity ratio of the company stood at 2.35x in FY19 as compared to the industry median of 1.61x. On the valuation front, the company has a price to cash flow per share of 46.44x against the industry average of 29.39x. Moreover,it reported a higher EV/EBITDA of 27.7x and P/E of 41.12x as compared to the industry average of 3.6x and 12.6x, respectively, exhibiting that the stock is extremely overvalued. Coming to the stock’s performance, it produced returns of 12.21% and 27.03% in the time period of three months and six months, respectively. As per ASX, the stock of CSL made a 52-week high of $253.830 on 16 October 2019 and is trading close to it. Hence, in light of aforesaid facts coupled with stretched valuation and current trading levels, we advise investors to closely watch the stock at the current market price of A$253.000 per share (up 1.856% on 16th October 2019) and wait for better entry levels.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...