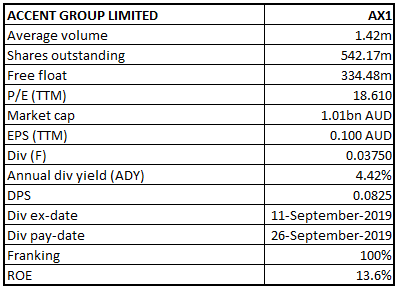

Accent Group Limited

AX1 Details

Robust Growth from the Digital Segment: Accent Group Limited (ASX: AX1) operates in the footwear and apparel businesses across the Australia and New Zealand region.

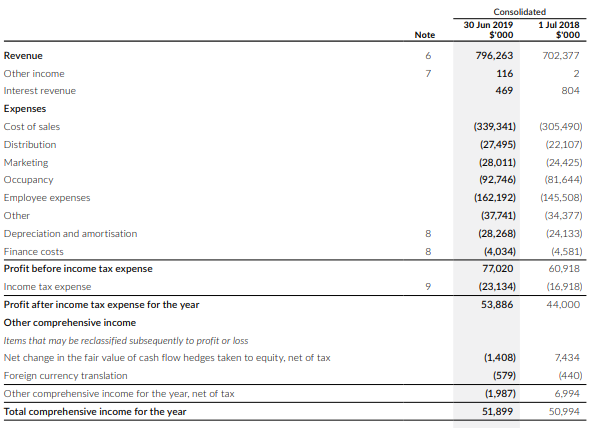

FY19 Operational Highlights for the Period Ended 30 June 2019: AX1 announced its full-year results, wherein the company reported revenue of $796.263 million as compared to $702.377 million in FY18, aided by strong sales performance from Vans, Dr Martens, Merrell and CAT. The company reported EBITDA at $108.853 million, up 22.5% on y-o-y basis. NPAT during the year came in at $53.886 million, up 22.5% on y-o-y basis. Digital Sales grew by 93% on y-o-y basis, comprising 15% of the total revenue. AX1 delivered an improvement in gross margin by 130 bps at 56.1%, reflecting improvement across vertical brand and product penetration, followed by margin improvement from The Athlete’s Foot (TAF). During FY19, the company opened 54 new stores, refurbished 32 stores and closed 21 stores, depicting a network of 479 stores at the end of FY19. Property, plant and equipment increased to $86.167 million from $74.664 million in FY18 due to significant investment across new stores and new digital infrastructure.

FY19 Income Statement Highlights (Source: Company Reports)

Guidance: As per the FY20 guidance, the company is expecting low single-digit LFL growth, including strong-digital growth. The company is expecting growth from TAF corporate stores. The business also expects gross margin to be in-line with FY19, driven by underlying improvement through vertical brand penetration and exclusive brands, offset by the impact of currency.

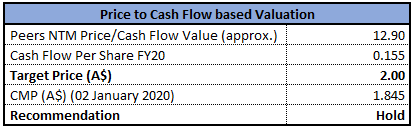

Valuation Methodology: Price to Cash Flow Multiple Approach

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock is quoting at $1.845 with a market capitalization of ~$1.01 billion. The stock has generated returns of 11.01% and 35.64% in the last three months and six months, respectively. At the current market price, the stock is quoting at the upper band of its 52-week trading range of $1.125 and $1.950. With the openings of new stores, AX1 is generating strong cash conversion with an average store payback of less than 18 months. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., Price to Cash Flow Multiple and arrived at a target price of higher single-digit upside (in % terms). Looking at the current trading levels, price movement, growing digital sales, gross margin improvement and valuation, we recommend a “Hold” rating on the stock at the current market price of $1.845, down 1.072% as on 02 January 2020.

AX1 Daily Technical Chart (Source: Thomson Reuters)

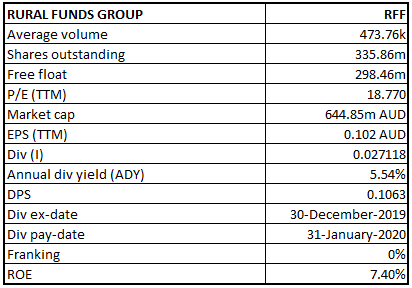

Rural Funds Group

RFF Details

FY20 AFFO Payout Ratio forecasted at 77%: Rural Funds Group (ASX: RFF) is engaged in the leasing of agricultural properties and equipment. Recently, Rural Funds Management Limited (ASX: RFM) confirmed the sale of the RFF’s poultry assets to ProTen Investment Management Pty Ltd as trustee for ProTen, which was announced on 28 October 2019.

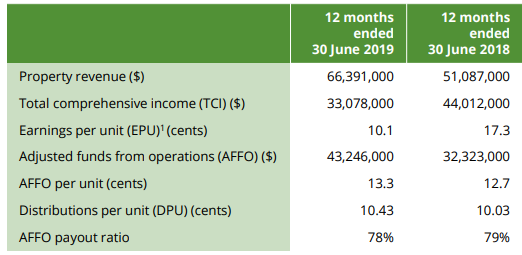

FY19 Highlights for the Period Ended 30 June 2019: RFF announced its full-year results, wherein the company reported Property revenue at $66.391 million, up 30% on y-o-y basis, aided by the inclusion of JBS transactions, acquisitions, development capital expenditure, and lease indexation. The company reported total comprehensive income (TCI) at $33.078 million, down from $44.012 million in FY18 on account of $18 million non-cash revaluation decrements on interest rate swaps. The company reported an increase in adjusted total assets of $222 million on account of acquisitions, capex and revaluations of almond orchards, vineyards and water entitlements. The business reported a 7% y-o-y growth in the Adjusted Net Asset Value (NAV) per unit, aided by independent revaluations of almond orchards, vineyards and water entitlement.

FY19 Performance Highlights (Source: Company Reports)

Guidance: In FY20, the company expects distributions per unit (DPU) amounting to 10.85 cents, consistent with 4% annual growth target and representing a forecast payout ratio of 77%.

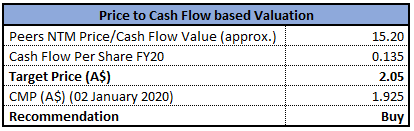

Valuation Methodology: Price to Cash Flow Multiple Approach

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of RFF is quoting at $1.925 with a market capitalization of ~644.85 million. The stock is quoting at the upper band of its 52-weeks trading range of $1.360 and $2.420. The stock has generated a mixed return of 13.27% and -16.52% in the last three months and six months, respectively. The company continues to oversee and manage existing assets, including capex and developments while pursuing new acquisitions with the potential for productivity development. Considering the aforesaid facts, we have valued the stock using one relative valuation metric i.e. Price to Cash Flow Multiple and arrived at a target price of higher single digit upside (in % terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price $1.925, up 0.26% as on 02 January 2020.

.jpg)

RFF Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...