Dell Technologies Inc.

.png)

DELL Details

Stellar Quarterly Growth to aid Business Prospect: Dell Technologies Inc. (NASDAQ: DELL) provides customers with the industry’s broadest and most innovative technology and services portfolio spanning from edge to core to cloud.

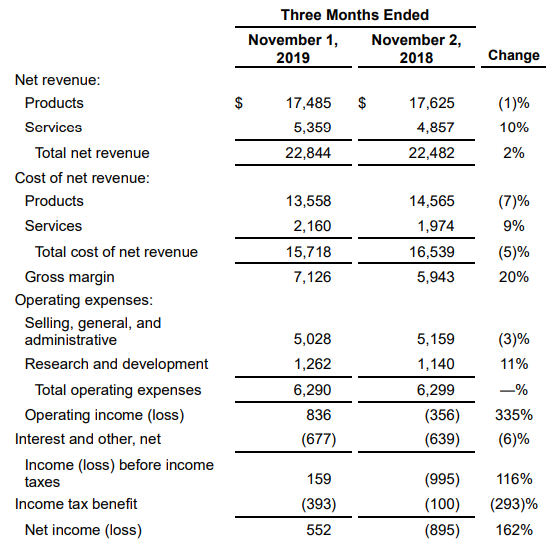

Q3FY20 Operational Highlights for the period ended 01 November 2019: DELL announced its quarterly reports, wherein the company reported total net revenue of $22,844 million, up 2% on y-o-y basis. Net income, during the quarter, came in at $552 million as compared to a loss of $895 million. During the quarter, the company reported adoption of cloud services with recent customer wins in the logistics, transportation, financial, communications and retail sectors. Infrastructure Solutions Group reported revenue of $8,390 million, up 6% on y-o-y basis, while the operating income stood at $996 million as compared to $935 million in previous corresponding quarter, depicting a growth of 10% on y-o-y basis. Growth was driven by strong demand in data protection and industry leading HCI business. Client Solutions Group reported a total revenue of $11,410 million as compared to $10,905 million in the previous corresponding period, driven by double-digit revenue growth in commercial desktops and workstations. Operating income from the above segment came in at $739 million as compared to $447 million in Q3FY19. The company reported net revenue from VMware at $2,483 million, up 11% on y-o-y basis. The segment reported an operating income at $717 million as compared to $768 million. During the quarter, the company reported strong demand growth in data protection and within the industry leading HCI business.

Q3FY19 Income Statement Highlights (Source: Company Reports)

Guidance: For FY20, the company expects revenue of $91.5 billion to $92.2 billion on GAAP basis, while operating income is likely to come in the range of $2.9 billion to $3.1 billion. Diluted EPS is expected within the range of $5.83 to $5.98.

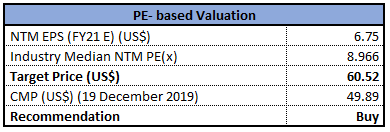

Valuation Methodology:Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

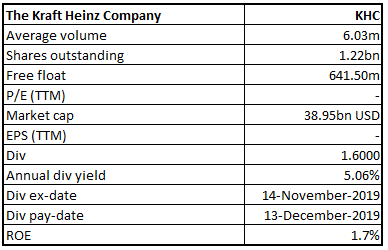

Stock Recommendation: The stock of DELL is quoting at $49.89 with a market capitalization of $36.79 billion. The stock has generated negative returns of 5.9% and 8.30% in the last three months and six months, respectively. Currently, the stock is quoting at the lower band of its 52-week trading range of $42.02 to $70.55. The company reported decent profitability, driven by working capital discipline and generated $1.6 billion of adjusted free cash flow. The group is optimistic about the long-term business as the company is consistently innovating and delivering comprehensive end-to-end IT solutions. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., price to earnings multiple and arrived at a target price of lower double-digit (in % terms). Looking at the recent price movement, current trading levels, business prospect, strong demand for its products, etc., we recommend a ‘Buy’ rating on the stock at the current market price of $49.89, up 0.22% as on 19 December 2019.

.jpg)

DELL Daily Technical Chart (Source: Thomson Reuters)

The Kraft Heinz Company

KHC Details

Reported Improved Quarterly Bottom-line: The Kraft Heinz Company (NASDAQ: KHC) manufactures and distributes food and beverage products, including condiments and sauces, cheese and dairy, meals, meats, refreshment beverages, coffee, and other grocery products across the world.

Q3FY19 Operational Highlights for the period ended 30 September 2019: KHC announced its quarterly results, wherein the company reported net sales at $6,076 million as compared to $6,389 million. The company reported net income of $898 million as compared to $619 million in the previous corresponding year. Income from United States came in at $4.36 billion, down 1.6% on y-o-y basis, driven by price increases across several product categories. The business reported EBITDA from the US segment at $1,155 million, down 1.8% on y-o-y basis on account of unfavorable volume/mix that more than offset higher pricing and favorable timing of marketing expenses. Within the Canada segment, the company reported net sales at $415 million, down 21.1% on y-o-y basis. The business reported 2.1 growth in volume/mix on account of increased promotional support in cheese and pasta sauce, as well as a partial recovery of retail inventory levels in certain categories. The EMEA segment reported net sales of $612 million as compared to $634 million, depicting a de-growth of 3.5% on y-o-y basis.

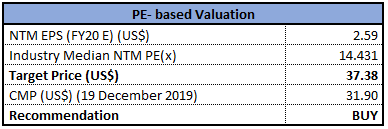

Valuation Methodology:Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

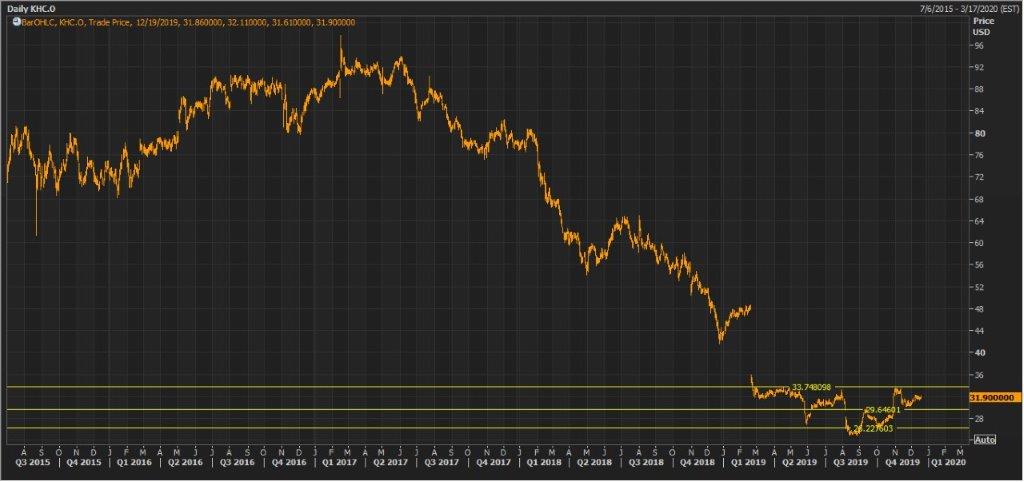

Stock Recommendation: The stock closed at $31.90, with a market capitalization of ~$38.95 billion. 52-week trading range for the stock stands at $24.86 and $48.66. The stock has delivered a positive return of 13.3% and 2.47% in the last three months and six months, respectively. Considering the aforesaid facts, we have valued the stock using one relative valuation, i.e., PE-based multiple and arrived at a target price of lower double-digit (in % terms). Looking at the current price movement, trading levels and business prospects, we recommend a ‘Buy’ rating on the stock at the closing price of $31.90, up 0.47% as on 19 December 2019.

KHC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...