GPT Group

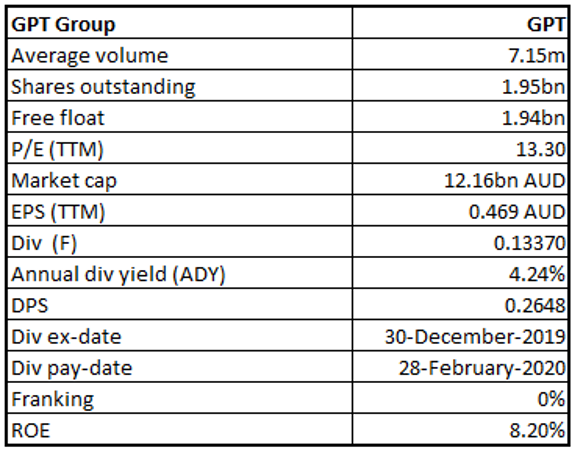

GPT Details

GPT Rides on Strategic Initiatives Amid Low Wage Growth:GPT Group (ASX: GPT) is one of Australia’s largest diversified property groups, which is involved in owning and managing retail portfolio, along with a portfolio of office and logistics property assets across Australia.

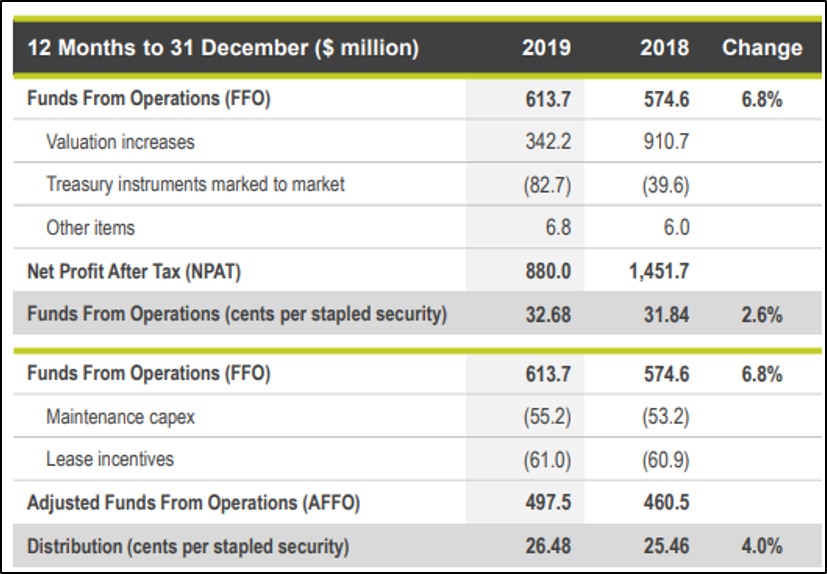

FY19 Financial Highlights for the Period Ended 31 December 2019: The company has recently declared its annual results for the year ended 31 December 2019. The company’s Funds From Operations(FFO) grew by 6.8% and came in at $613.7 million. FFO per security grew by 2.6% on a year over year basis, which has been adjusted for the effect of the capital raising. Net Profit After Tax for FY19 came in at $880 million, a decline of 39.4% on a year over year basis, primarily due to lower valuation gains.Distribution per security for the period stood at 26.48 cents, which represented an increase of 4% year over year.

FY19 Financial Highlights (Source: Company Reports)

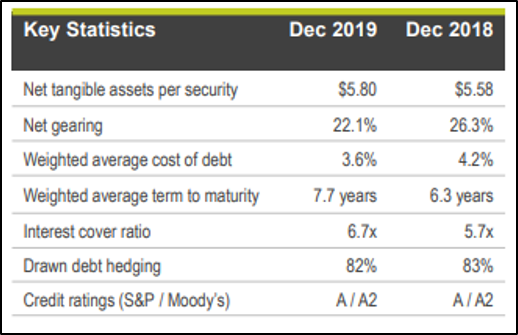

Capital Management Highlights: At the end of FY19, the company reported net tangible assets per security at $5.80 and net gearing at 22.1% followed by weighted average cost of debt of 3.6%. Total Return for the 12-months period was 8.7%.

Key Metrics (Source: Company Reports)

Key Growth Strategies: During the period, the company completed its Placement and Security Purchase Plan of ~$867 million. The move was taken to fund the Group’s development pipeline and to acquire 25% stake in Darling Park 1 & 2 and Cockle Bay Wharf. The company alsosecured a 33.4-hectare logistics development site at Kemps Creek for $100 million, along with a 32.8-hectare logistics development site at Truganina, Melbourne for $34 million.

Outlook: GPT group now forecasts to deliver FFO per security growth and Distribution per security growth of 3.5% for FY20. Going forward, the company expects to benefit from strong tenant demand on the back of logistics purchases and expansion completions.Nonetheless, the company’s retail sector is witnessing headwinds, on the back of low wage growth. However, low interest rates and ongoing investment demand are likely to continue to support asset valuations.

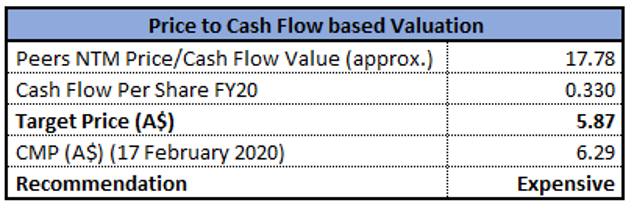

Valuation Methodology:P/CF Based Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:As per ASX, the stock is trading close to its 52-week high of $6.500. The stock gave a positive return of ~10% on a year-to-date basis. The stock has a market cap of ~$12.16 billion with a PE multiple of 13.3x and an annual dividend yield of 4.24%. We have valued the stock using P/CF based relative valuation method, and for the said purpose, we have considered peers like Dexus (ASX: DXS), Charter Hall Group (ASX: CHC) and Charter Hall Retail REIT (ASX: CQR), to name few. Therefore, we have arrived at a target price with a downside of single-digit (in percentage terms). Considering the valuation, and current trading levels, we give an “Expensive” rating on the stock at the current market price of $6.29 per share, up 0.801% as on 17 February 2020.

GPT Daily Technical Chart (Source: Thomson Reuters)

Stockland Corporation Limited

.png)

SGP Details

Growth in Residential Communities & Strategic Implementation are Key Positives: Stockland Corporation Limited (ASX: SGP) is engaged in owning, developing and managing real estate assets in Australia. On 3rd February 2020, the company announced that Robyn Elliott, Chief Innovation, Marketing and Technology Officer of the company, has resigned from the position, effective from the end of February.

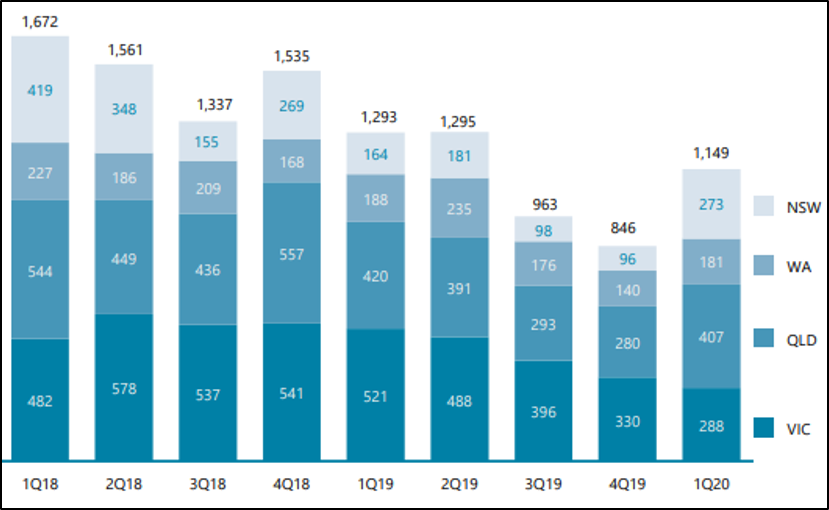

1QFY20 Key Takeaways for the Period Ended 30 September 2019: During the period, the company recorded its sharpest quarterly result in the residential communities, completing relatively above expectations with 1,149 net deposits taken, as compared to 846 net deposits taken in the previous quarter. The results reflected improving market conditions with 9.7% year over year rise in net reservations. The company remains on track to deliver more than 5,000 settlements in FY20, containing ~500 town homes.

Net deposit for 1QFY20 (Source: Company Reports)

What to Expect: For FY20, the company remains on track to focus on execution of its strategies. The group is expecting funds from operations (FFO) per security to be flat in FY20. Under the residential segment, operating profit margin is projected to be about 19%. Under retirement living, the company focuses on driving efficiency and enhancing returns in the portfolio. Under commercial property, comparable FFO growth is likely to be around 1%.

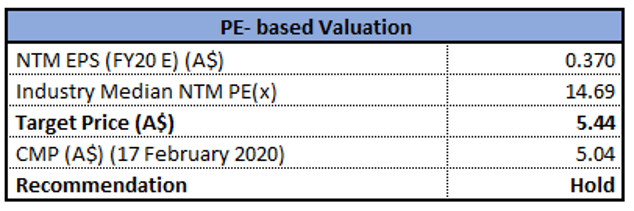

Valuation Methodology:P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week high of $5.24. The stock gave a return of 36.31% in the past one year. The stock has a market cap of $11.99 billion with an annual dividend yield of 5.49% and a P/E multiple of 38.69x. Considering the returns, trading levels, and decent growth opportunities, we have valued the stock using one relative valuation method, i.e., Price to Earnings multiple. For the purpose, we have taken the peer group – Scentre Group (ASX: SCG), Vicinity Centres (ASX: VCX), Charter Hall Retail REIT (ASX: CQR), to name few, and arrived at a target price offering higher single-digit upside (in % terms). Hence, we recommend a “Hold” recommendation on the stock at the current market price of $5.040, up by 0.199% on 17th February 2020.

SGP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...