.png)

Stocks’ Details

Spark New Zealand Limited

Chairman’s Address to Shareholders:Spark New Zealand Limited (ASX: SPK) is in the business of telecommunication services. The market capitalisation of the company stood at A$7.42 Bn as on 7th November 2019. The Chairman of the company addressed the shareholders and stated that the operating revenues of SPK stood at $3.5 billion in FY19, which were flat on YoY basis, due to offset of growth markets by expected declines in legacy voice and managed data and network products. It was also stated that FY19 has been a successful year for its mobile business. It significantly outperformed its mobile market competitors, securing more than 60% of total market growth in service revenue and connections, primarily fueled by growth in higher-value unlimited plans. The following picture provides an idea of results for the 12 months ended 30th June 2019:

.png)

Financial Results (Source: Company Reports)

Future Guidance:The Chairman of the company communicated that SPK has a strong platform for the year ahead. The company is expecting EBITDAI in the range of $1.1 Bn to $1.12 Bn and has given the dividend guidance of 25 cps (at least 75% imputed) for FY20.

Stock Recommendation:From April 2020, Spark Sport would be the official rights partner for all New Zealand Cricket matches played in New Zealand, with TVNZ joining as the free-to-air partner for a selected number of T20 International and Super Smash matches. Net margin of the company stood at 11.6% in FY19 against the industry median of 7.8%, representing SPK’s better capabilities to convert its top-line into the bottom-line in comparison to the broader industry. Return on equity of the company stood at 27.7% as compared to the industry median of 6.2%. This implies that the company has provided better returns to shareholders against the peer group.

On the stock’s performance front, it delivered a return of 6.39% and 17.15% in the time period of three months and six months, respectively. Therefore, considering the company’s outperformance in FY19, decent outlook, expansion of sport offering, decent net margins and respectable RoE, we maintain a “Hold” rating on the stock at the current market price of A$4.110 per share, up 1.733% on 7th November 2019.

SkyCity Entertainment Group Limited

Fire at NZICC:SkyCity Entertainment Group Limited (ASX: SKC) is in the business of gaming entertainment. The market capitalisation of the company stood at A$2.39 Bn as on 7th November 2019. Recently, the company through a release dated 23rd October 2019 announced that a fire broke out at its site New Zealand International Convention Centre in Auckland. Later, the company stated that the fire is now under control and the NZICC site has now been handed back to Fletcher Construction, though access remains restricted as safety and structural assessments and investigations into the cause of the fire are completed.

When it comes to FY19 performance, the company experienced solid performance from the local businesses, which was supplemented by the growth in IB turnover. The group experienced a growth of 1.9% in normalised NPAT to $173 million. However, the key drivers for the results mainly were (1) Stable performances from Adelaide (on a like-for-like basis) and Hamilton, (2) Impact of Asset sale programme. The below picture provides an idea of movement in net hedged debt:

.png)

Net Hedged Debt (Source: Company Reports)

What to Expect:For FY20, the domestic and international economic environment is likely to remain challenging with continuing cost pressures. The company anticipates achieving some growth in normalised EBITDA of the group vs like-for-like FY 2019 comparative. SKC added that the major projects are expected to complete by the end of 2020 in Auckland and Adelaide.

Stock Recommendation:In FY19, the company rolled out an offshore online casino in partnership with the Gaming Innovation Group, which could help the company in expanding its business. On the valuation front, as per ASX, the stock of SKC is trading at a price to earnings multiple of 17.46x in comparison to the industry median of 18.3x on TTM basis. In addition, SKC has a price to cash flow multiple of 10.7x against the industry median of 12.4x on TTM basis. When it comes to the stock’s past performance, it generated a return of 4.39% in the last one year and 10.53% on YTD basis. Thus, considering annual dividend yield of 5.31%, returns in the last couple of months, and entry into new partnerships, we give a “Buy” recommendation on the stock at the current market price of A$3.550 per share, down 0.56% on 7th November 2019.

National Australia Bank Limited

A Look at FY19 Results:National Australia Bank Limited (ASX: NAB) is one of the leading banks in Australia with a market capitalisation of A$80.15 Bn as on 7th November 2019. Recently, the bank has released its results for FY19 in which there was a decline of 4.2% in revenues, and it posted a net interest margin of 1.78%, a decline of 7 bps. However, excluding customer-related remediation, revenue witnessed a rise of 1.1%, primarily reflecting growth in the lending business, partly offset by lower margins. It was mentioned that the transformation of the bank is delivering productivity benefits, allowing NAB to absorb higher spend to strengthen the compliance and control environment while also investing in its business.

.png)

Drivers of Cash Earnings (Source: Company Reports)

What to Expect:The bank stated that the Australian economic growth has slowed and is anticipated to remain below trend in 2020 and 2021, while New Zealand growth has slowed to a modest level. The bank is now over two years into its three-year transformation. NAB's $1.5 billion targeted additional investment over three years is delivering better outcomes for all its stakeholders

Stock Recommendation:As at 30th September 2019, group common equity tier 1 ratio stood at 10.38%, reflecting a rise of 18bps from September 2018. The asset quality of the bank remains sound. While Australian housing arrears increased further, loss rates for this portfolio remain low at 2 basis points. NAB declared a fully franked final dividend amounting to 83 cps, at the company tax rate of 30%, which is to be payable on 12th December 2019. On the valuation side, the stock of NAB is trading at a price to book multiple of 1.5x as compared to the industry average of 2.9x on TTM basis. It has EV to EBITDA multiple of 3.3x against the industry average of 17.1x on TTM basis. As per the ASX, the stock of NAB is trading towards its 52-week higher levels. After experiencing a challenging FY19, the bank was capable to manage the cost savings of $480 million in full year, which allowed the bank to absorb ongoing investment in better products and services. Therefore, considering cost savings, transformation program, sound financial parameters, decent NII growth in FY 2019, we maintain a “Hold” rating on the stock at the current market price of A$28.420 per share, up 2.23% on 7th November 2019.

Macquarie Group Limited

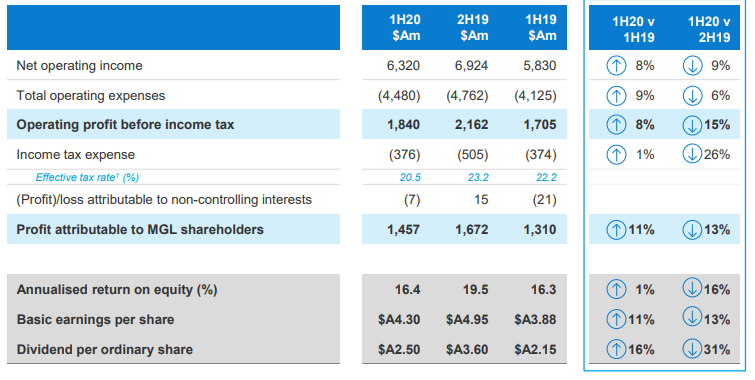

Rise in NPAT:Macquarie Group Limited (ASX: MQG) is a non-operating holding company for consolidated entity and a providerof financial services such as banking, financial, advisory, investment and funds management services. For the half-year ended 30th September 2019, the company reported a net profit after tax attributable to ordinary shareholders of $A1,457 Mn, with a rise of 11% as compared to 1H FY19. The key personnel of the company stated that 1H results outline the benefits of the business and geographic diversity of the Group, with increased client activity throughout many of its business lines and favourable market conditions throughout the Commodities and Global Markets platform.

First-Half Results (Source: Company Reports)

Future Aspects:The Group’s short-term outlook remains subject to a range of factors, primarily including (1) The conduct of period-end reviews and the completion rate of transactions, (2) market conditions, (3) the impact of foreign exchange. The Group currently anticipates the FY20 result to be slightly down on FY19.

Stock Recommendation:The Bank Group APRA Basel III Common Equity Tier 1 capital ratio stood at 11.4% at 30 September 2019. When it comes to valuation, the stock of MQG is trading at a price to book multiple of 2.4x as compared to the industry median (Financials) of 1.3x on TTM basis. Also, MQG is trading at a price to earnings multiple of 14.64x against the industry median of 13.6x on TTM basis. The stock of MQG witnessed a rise of 13.28% in the time period of three months and 26.77% on YTD basis. Currently, the stock is inching towards its 52-week higher levels. Hence, considering the expectation of FY 2020 results to be lower than FY 2019, current trading levels and valuation parameters, we give an “Expensive” rating on the stock at the current market price of A$136.610 per share, up 0.856% on 7th November 2019.

Treasury Wine Estates Limited

Tim Ford, COO, Expected to Replace Michael Clarke, CEO in 2021:Treasury Wine Estates Limited (ASX: TWE) is involved in grape growing and sourcing; wine production, marketing, sales and distribution. Recently, the company’s director Michael Anthony Clarke acquired 52 shares at a value of $17.37 per share. In another update, the company announced that Michael Clarke intends to retire from the role of Managing Director and Chief Executive Officer in the first quarter of fiscal 2021, providing approximately one year’s notice. The Board of TWE also announced that Tim Ford, Chief Operating Officer, would be appointed to the role of CEO, effective from the retirement of Mr Clarke in the first quarter of fiscal 2021, which reflects the company’s strong succession planning.

FY19 Financial Highlights (ended on June 30, 2019):Net sales revenue increased by 16.6% on a reported currency basis to $2,831.6 Mn. NPAT and EPS increased by 16% to $419.5 Mn and 18% to 58.4 cents per share, respectively. The Board of Directors declared a fully franked final dividend of 20 cps.

FY19 Income Statement (Source: Company Reports)

What to expect:The company has reiterated F20 guidance of reported EBITS growth of around 15% to 20%. F20 full-year underlying cash conversion is expected to be in-line with FY19.

Stock Recommendation:TWE’s share generated a positive YTD return of 19.62%. Its EBITDA margin and net margin for FY19 stood at 26.1% and 14.6%, better than the industry median of 18.9% and 8.3%, respectively, implying decent fundamentals. Its RoE for FY19 stood in-line to the industry median of 11.7%. Its current ratio for FY19 stood at 2.45x, better than the industry median of 1.47x. Hence, considering outstanding FY19 top-line and bottom-line performance, decent profitability margins, FY20 guidance, we recommend a “Hold” rating on the stock at the current market price of $17.890 per share, up 1.879% on November 7, 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...