.png)

Stocks’ Details

Computershare Limited

Higher Recurring revenues & Cost Cutting Initiatives are Key Positives: Computershare Limited (ASX: CPU) is engaged in offering investor services, employee share plan services, business services, and technology services. The company recently announced that two of its Directors named Christopher John Morris and Simon David Jones, acquired 33,330 and 3000 ordinary shares, respectively.

1HFY20 Key Financial Highlights: During the six months ended 31st December 2019, the company reported revenue of US$1,141.7 million, an increase of 1.2% year over year. EBITDA for the period came in at US$338.7 million, up 2.2% on pcp. Recurring revenues for the period represented 78.3% of total revenues during the period, which more than offset the declines in event-based revenues. NPAT for the period stood at US$157.8 million, depicting a decreased of 16.9% year over year. The Board declared an interim dividend of AU 23 cents per share, payable on 19th March 2020. During the period, the company remained on track to carry on with its long-term growth strategies and strengthen its competitive position in the market.

.png)

Key Financial Metrics (Source: Company Reports)

What to Expect: The company anticipates EPS for FY20 is expected to go down by ~5% in constant currency. For 2HFY20, the company expects EPS of to be ~1.5 cents per share greater than 2H19 Management EPS. Implementing the long-term strategies to enhance the business quality and boost recurring revenues will remain a key focus area.

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation

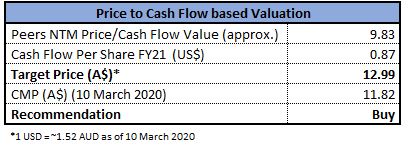

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of ~27.78% over a period of six month and is currently trading close to its 52-week low level of $10.920. The stock of CPU is having a market capitalization of $6.17 billion, with an annual dividend yield of 4.03%.In 2HFY20, the company expects added impact from the new US Issuer Services business. We have valued the stock using Price to Cash Flow based relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like ASX Ltd (ASX: ASX), Challenger Ltd (ASX: CGF), Suncorp Group Ltd (ASX: SUN), to name few. Hence, we give a “Buy” recommendation on the stock at the current market price of $11.82, up 3.593% on 10 March 2020.

Bravura Solutions Limited

BVS Rides on Higher Segmental Revenues: Bravura Solutions Limited (ASX: BVS) is involved in providing software products and services to the Funds Administration and Wealth Management sectors. Recently, the company announce that Peter Mann has disposed 29,072 fully paid ordinary shares for a consideration of $5.78 per share. In another update, the company stated that BlackRock Group, a substantial holder of the company, has increased its voting power from 6% to 7.08%.

1HFY20 Key Financial Highlights for the Period Ended 31st December 2019: During the period, revenue stood at $135.1 million, an increase of 6% year over year. Excluding the contribution from acquisitions, revenue reported a rise of 3% on pcp. NPAT for the period went up by 21% and came in at $19.8 million. The company declared an interim dividend of 5.5 cents per share, representing a payout of 68% of NPAT. The Wealth management business witnessed an increase of 1% in 1HFY20. Revenue of the Funds Administration segment grew by 19%, obtaining advantages from higher licence fees due to expansion on the client front.

.png)

1HFY20 Key Metrics (Source: Company Reports)

Outlook: In FY20, the company expects NPAT growth to be in the mid-teens (excluding the impact of acquisitions). Acquisitions are likely to make a further contribution of ~ $3m of FY20 NPAT. The Wealth Management business offers significant opportunities from new clients and continued project activity.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation

.png)

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 22.29% and 20.7% over a period of 3 months and 6 months, respectively. The stock of the company is currently trading below the average of its 52-week trading level of $3.73 and $6.27. The stock of BVS is having a market capitalization of $942.77 million, with a P/E multiple of 24.97x.We have valued the stock using Price to cash flow based relative valuation method. For the purpose, we have taken the peer group - Hub24 Ltd (ASX: HUB), EML Payments Ltd (ASX: EML), Pushpay Holdings Ltd (ASX: PPH), to name few, and arrived at a target price of lower double digit upside (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $3.91, up 1.034% as on 10 March 2020.

Link Administration Holdings Limited

Geographical Benefits & Business Diversification are Key Positives: Link Administration Holdings Limited (ASX: LNK) is engaged in providing technology-enabled administration, securities registration and asset services to clients globally. The company recently stated that Michael Carapiet, Director of the company, acquired two 50,000 fully paid ordinary shares for a total consideration of $220,000, each. In another recent update, the company announced that Vanguard Group, a substantial holder of the company has increased its voting power from 5.003% to 6.014%. As per the company’s recent update, till now it has bought back 3,222,175 shares for a consideration of around around $17.84 million.

1HFY20 Results for the Period Ended 31st December 2019: The company generated revenue amounting to $624 million, down 4% year over year. Operating EBITDA and NPAT went down by 11%, each, respectively. The management declared an interim dividend of 6.5 cents per share (fully franked). The company remains on track to make good progress by executing its strategic plan and maintaining a robust medium to long term outlook. 1HFY20, indicates geographic benefits as well as business diversification, helping the company to offset the current headwinds in its UK and RSS business.

.png)

Key Financial Metrics (Source: Company Reports)

What to Expect: For FY20, the company expects operating NPATA to be at least $160 million and is confident about its medium-term outlook. Operating EBITDA for the year is expected to be ~10% lower than previous year. In addition, the company expects revenue from Retirement & Superannuation Solutions (RSS) to be in the band of $480 million - $500 million.

Valuation Methodology: P/CF Multiple Based Relative Valuation

.png)

P/CF Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM- Next Twelve Months

Stock Recommendation: Over a period of 6 months, the stock gave negative returns of 28.62% and is currently trading very close to its 52-week low level of $3.71. The stock of LNK is having a market capitalization of $2.12 billion, with a P/E multiple of 13.26x.Considering the strategic initiatives in 1HFY20, current trading level and a decent outlook, we have valued the stock using P/CF based relative valuation method and for the purpose, have taken the peer group - Computershare Ltd (ASX: CPU), Suncorp Group Ltd (ASX: SUN), and Perpetual Ltd (ASX: PPT). We have arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $4.160, up 4.261% on 10 March 2020.

IRESS Limited

Revenues up 10% Year Over Year: IRESS Limited (ASX: IRE) is a technology company that offers software related products to the financial services industry. The company recently stated that Trudy Joy Vonhoff, Director of the company, acquired 11,000 indirect ordinary shares for a total consideration of $132,555.14. In another update, the company announced that it will distribute a dividend of $0.30per share, with a payment date of March 20, 2020.

FY19 Financial Highlights for the Period Ended 31 December 2019: In FY19, the company reported group revenue of $508.9 million, up 10% year over year and reported NPAT amounted to $65.1 million, up 2% on pcp. The year over year increase in revenues was on the back of strong underlying performance in the United Kingdom and Australia along with QuantHouse acquisition.It also reported strong fundamentals with a cash conversion rate of 87% and recurring revenue rate of ~90%. In FY19, the company declared a final dividend of 30 cents per share (40% franked).

.png)

FY19 Key Highlights (Source: Company Reports)

What to Expect: In FY20, the reported Segment Profit is expected to grow between 3% and 8% ($156 million - $164 million). Non-operating costs in FY20 is expected to be in the range of $3 to $6 million, indicating higher investments in the UK and cost related to business integration.

Valuation Methodology:P/BV Multiple Based Relative Valuation

.png)

P/B Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM- Next Twelve Months

Stock Recommendation: As per ASX, the stock is currently trading close to its 52-week low level of $10.51. The stock of IRE is having a market capitalization of $1.92 billion, with a P/E multiple of 28.94x.Considering the above mentioned factors, we have valued the stock using P/B based relative valuation method and for the purpose, have taken the peer group - AP Eagers Ltd (ASX: APE), WiseTech Global Ltd (ASX: WTC), Carsales.Com Ltd (ASX: CAR), to name few. We have arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $11.38, up 3.737% on 10 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...