Stocks’ Details

Bank of Queensland Limited

Improved Lending Process to Aid Business Prospects:Bank of Queensland Limited (ASX: BOQ) operates in banking, financial and related services. Recently, the company reported regarding the change of Director’s interest, wherein one of its Directors named George Frazishas acquired 143,214 Performance Award Rights and 50,000 Ordinary Shares.

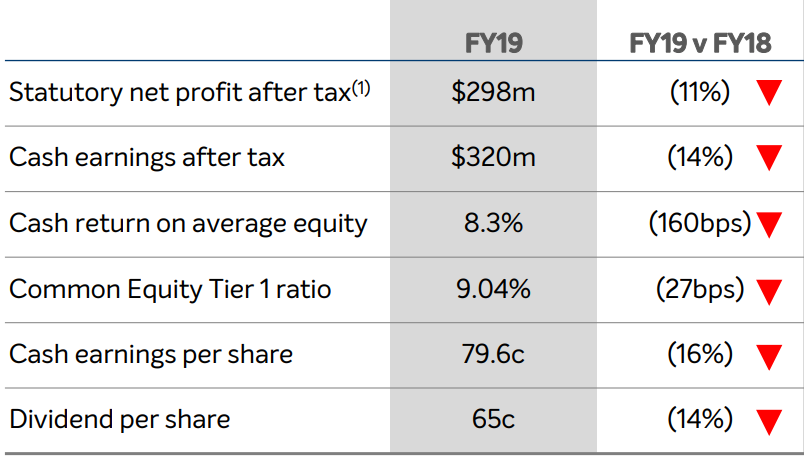

FY19 Operational Highlights for the Period ending 31 August 2019: BOQ declared its FY19 financial results, wherein it posted net interest income at $961 million, mildly lower as compared to $965 million in the previous financial year. Statutory net profit after tax stood at $298 million, down 11% on y-o-y basis.The company reported cash earnings after tax at $320 million as compared to $372 million in FY18. Common Equity Tier 1 ratio, during the year, stood at 9.04%, while cash return on average equity stood at 8.3%. The bank reported a yoy reduction of five basis points in its net interest margin, with most of the reduction evident in the first half.

FY19 Operational Highlights (Source: Company Reports)

Guidance: BOQ expects that FY20 non-interest income contribution from insurance to remain consistent with the second half of 2019. The Management highlighted that the bank is well-positioned for ‘unquestionably strong’ FY20 and is awaiting clarification from the regulator on the revised risk weighting framework, which is due to be implemented in 2022. For customers of the retail bank, the new mobile app and digital banking platform is under development with a phased rollout planned and a pilot commencing in the first half of 2020. The bank also expects improvements across the number of lending processes and lending volumes in FY20.

Valuation Methodology:Price to Book Value Based Approach

Price to Book Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

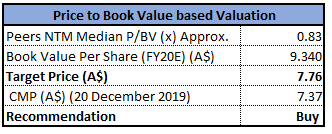

Stock Recommendation: The stock of BOQ is trading at $7.370, with a market capitalization of ~$3.28 billion. The stock has generated negative returns of 23.61% and 22.81% in the last three months and six months, respectively. The stock is currently trading at the lower band of its 52-week trading range of $7.110 - $10.770. The business is investing in modernising technology infrastructure and digital platforms. The Management is looking for better accountability for achieving better outcomes for all stakeholders through simplification of the business and improvement in productivity and address costs. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., price to book value multiple and arrived at a target price of lower single-digit (in % terms). Looking at the current trading levels, valuations and business prospects, we recommend a “Buy” rating on the stock at the current market price of $7.370, down 0.54% as on 20 December 2019.

Webjet Limited

Strong FY20 Guidance Driven by Organic Growth: Webjet Limited (ASX: WEB) operates a full range of online travel booking service for flights, hotels, car hire, cruises, tours. Recently, the company informed that Macquarie Group Limited is ceased to be a substantial shareholder.

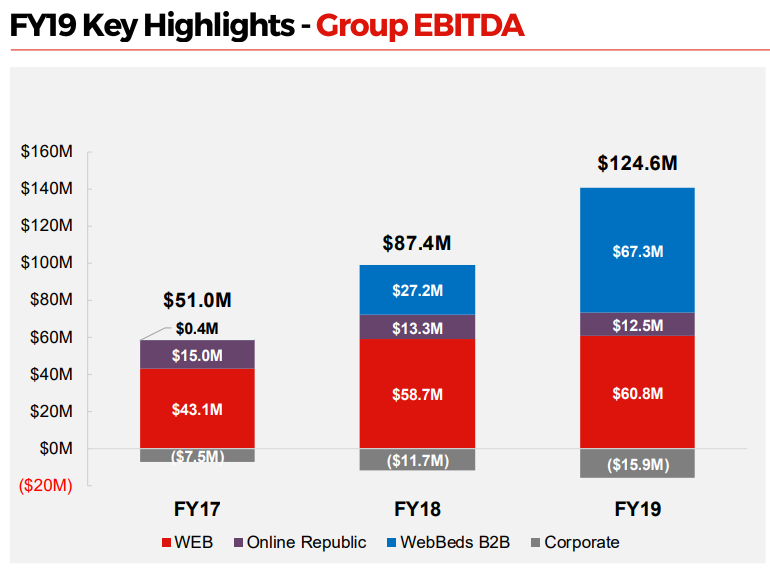

FY19 Operational Highlights for the Period Ended 30 June 2019: In FY19,the company reported revenue of $366.4 million, up 26% on y-o-y basis. The company posted EBITDA at $123.1 million, up 43% on y-o-y basis, while the EBITDA margin stood at 33.6% during FY19. The company reported NPAT of $60.3 million, up 45% from FY18. Bookings from WebBeds and Webjet OTA segments stood at 3.444 million and 1.565 million as compared to 2.277 million and 1.549 million, respectively, in FY18. The company reported EBITDA from WebBeds and Webjet OTA at $67.3 million and $60.8 million, representing a y-o-y growth of 148% and 4%, respectively. Within the Online Republic segment, the business reported improved TTV margins of 10.5% as compared to 10.1% in FY18, aided by the company’s focus on higher margin through profitable bookings.

Segment-wise FY19 EBITDA (Source: Company Reports)

Guidance: The company expects FY20 underlying EBITDA between the range of $157 to $167 million, depicting growth in the range of ~26% - ~34% over FY19. The company expects H1FY20 EBITDA at ~$80 million, driven by 25% organic EBITDA growth, and 1% to 5% growth from Webjet OTA. As per the management guidance, corporate costs are expected to increase by 5% - 10% on y-o-y basis. The company expects the FY20 operating cash conversion rate within 95% - 110%.

Valuation Methodology:Price to Earnings Based Approach

Price to EarningsBased Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

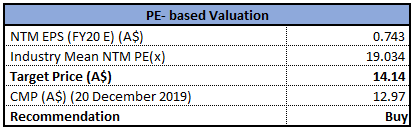

Stock Recommendation: The stock is quoting at $12.970, with a market capitalization of ~1.75 billion. The stock has generated returns of 9.57% and -14.30% in the last three months and six months, respectively. At the current market price, the stock is quoting at the lower band of its 52-week trading range of $9.980 to $17.190. WebBeds has become one of the largest and fastest-growing businesses, which has delivered $2.2 billion TTV and $67.3 million EBITDA, while the OTA business is delivering profitable growth in a tough domestic travel market in FY19. Considering the aforesaid facts, we have valued the company, using price to earnings based relative valuation method and arrived at a target price of high single-digit upside (in% terms). Looking at the stock price movement, current trading levels, business scenario and improved financials, we recommend a ‘Buy’ rating on the stock at the current market price of $12.970, up 0.232% as on 20 December 2019.

Japara Healthcare Limited

Expects Strong FY20 Cash flow aided by RAD Inflows: Japara Healthcare Limited (ASX: JHC) develops, operates and owns residential aged care homes. Recently, the company informed that it would release its half-yearly results for the period ended 31 December 2019 on 28 February 2020.

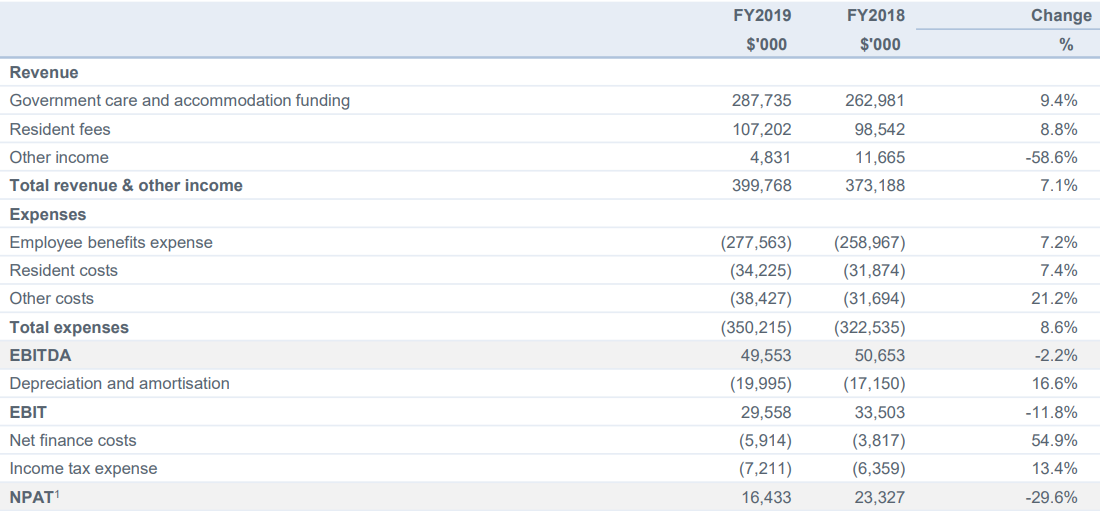

FY19 Highlights for the period ended 30 June 2019: JHC declared its financial results, wherein the company reported total revenue of $399.8 million, up 7.1% on y-o-y basis, aided by contribution of Riviera Health acquisition. The company reported recurring EBITDA of $49.6 million, up 2.5% from FY18. JHC reported NPAT at $16.4 million, down 29.6% on y-o-y basis on account of lower non-recurring earnings and higher depreciation and interest expense. The average underlying occupancy of the business stood at 93% in FY19. During the year, the company added 303 new places, which include three new homes. During FY19, the company reported net expenditure on land and construction at $99.4 million.

FY19 Income Statement Highlights (Source: Company Reports)

Outlook: As per the FY20 guidance, the company expects EBITDA to be in the range of 5% to 10%, lower than FY19. The company will focus on the delivery of its developments with over 300 net new places, which are expected to be opened in FY20. The company expects strong cash flow, aided by RAD inflows and underpinned by higher bed contract prices.

Stock Recommendation: The stock of JHC is trading at $0.990 with a market capitalization of ~$288.63 million. The stock is trading at the lower band of its 52-week trading range of $0.970 to $1.550. The stock has generated negative returns of 7.69% and 15.29% in the last three months and six months, respectively. Japara has continued to invest in greenfield and brownfield developments to underpin future earnings growth while the existing portfolio also continues to deliver mature home RAD inflows. Considering the aforesaid facts, we have valued the company using PE multiple based relative valuation method and arrived at a target price of single-digit upside (in % terms). Looking at the recent price movement, current trading levels, decent FY20 guidance and business prospects, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.990, down 8.333% as on 20 December 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...