.png)

Stocks’ Details

BlueScope Steel Limited

Digital Transformation & Increasing Shareholder’s Value are Key Positives: BlueScope Steel Limited (ASX: BSL) is engaged in the manufacturing of steel and has a market capitalisation of $6.38 Bn as on 26 February 2020. The company recently announced that it has bought back a total of 35,475,187 shares at the total consideration of ~$448,608,301 pursuant to its daily share buy-back notice.

1HFY20 Key Highlights for the Period Ended 31 December 2019: Sales revenue from continuing operations decreased by 8% on pcp, to $5,861 Mn. Underlying EBITDA for the period decreased by 47% to $564.3 Mn, mainly due to lower sales from North Star BlueScope Steel. Underlying EBIT for the period decreased by 64% to $302.4 Mn. Reported net profit after tax for the period decreased by 70% to $185.8 Mn. Return on Invested Capital decreased from 24.9% in 1HFY19 to 8.4% in 1HFY20. Net debt at the end of the period stood at $46.9 Mn as compared to net cash of $127.5 Mn at the end of first half of FY19. The company declared an interim dividend of 6 cents per share for 1HFY20.

.png)

1HFY20 Key Financial Metrics (Source: Company Reports)

Outlook: As per the release, the company remains on track to meet customers need and drive performance by focussing on transforming the business particularly through digital technology and actively addressing climate change. The company expects underlying EBIT for 2HFY20 to be in line with 1HFY20 figure of $302.4 million. The company is focused on generating returns above its cost of capital for creating value for its shareholders.

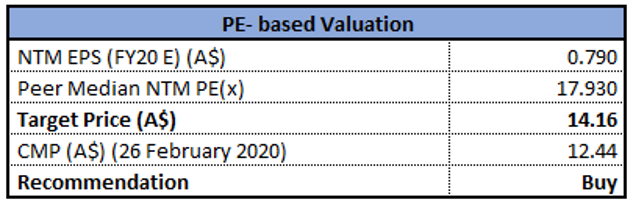

Valuation Methodology:P/E Based Valuation

P/E Valuation Multiple (Source: Thomson Reuters)

Stock Recommendation: The stock posted a positive return of ~2.35% in the past six months and is currently trading below the average of its 52-week low and high of $10.305 and $16.17, respectively.As per ASX, the stock of VRT hasprice to earnings multiple of 11.38x, and an annual dividend yield of 1.11%. Considering the above factors, we have valued the stock using P/E based relative valuation method and for the purpose, we have taken the peer group - Sims Ltd (ASX: SGM), James Hardie Industries PLC (ASX: JHX) and CSR Ltd (ASX: CSR), to name few. Therefore, we have arrived at a target price of lower double-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $12.44, down 1.426% as on 26 February 2020.

Steadfast Group Limited

Revenues up ~29.6% Year Over Year: Steadfast Group Limited (ASX: SDF) is mainly involved in the provision of services to Steadfast Network brokers, distribution of insurance policies, and related services. Recently, the company announced that it will distribute a dividend of $0.0360 per share, with an ex-date of March 02, 2020 and payment date of March 26, 2020.

1HFY20 Financial Highlights: During the half year ended 31 December 2019, the company reported underlying revenue of $414.4 million, up 29.6% on prior corresponding year. Underlying EBITA for the period amounted to $108.9 million, representing an increase of 27.5% on pcp. Underlying NPAT stood at $53.2 million, up 39.1% on prior corresponding year. During the period, the company reported underlying EPS of 6.26 cents per share, increasing 29.7% on the previous year. The company declared a fully franked interim dividend of 3.6 cents per share. Gross written premium for the Steadfast Network was reported at $3.9 billion, representing an increase of 32% on the prior corresponding period.

.png)

1HFY20 Financial Results (Source: Company Reports)

FY20 Guidance: In FY20, the company expects underlying EBITA in the range of $215 million - $225 million. Underlying NPAT for the year is expected to be in the range of $100 million - $110 million. In addition, growth in underlying diluted EPS is expected in the range of 10% - 15%.

Valuation Methodology: P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated a negative return of ~2.2% in the past 5 days and is currently trading towards its 52 weeks high level of $4.1. As per ASX, the stock of SDF has a price to earnings multiple of 29.86x, and an annual dividend yield of 2.26%. During FY19, debt to equity ratio of the company stood at 0.34x as compared to the industry median of 0.17x. Notably, the company also notified that the IBNA transaction and the PSF Rebate Acquisition will impact the statutory NPAT in FY20. Considering the above factors, we have valued the stock using P/E based relative valuation approach and have arrived at a price correction of lower double-digit (in percentage terms). For the said purposes, we have considered AUB Group Ltd (ASX: AUB), Medibank Private Ltd (ASX: MPL) and Challenger Ltd (ASX: CGF) as peers. We are of the view that all the positives have been factored in the current levels. Therefore, we suggest investors to book profits and recommend a “Sell” rating on the stock at the current market price of $3.79, down by 3.562% on 26 February 2020.

Nine Entertainment Co. Holdings Limited

EBITDA for 1HFY20 Increased a Whopping 41% Year Over Year: Nine Entertainment Co. Holdings Limited (ASX: NEC) is involved in broadcasting and program production throughout Free to Air television along with metropolitan radio networks in Australia. The market capitalisation of the company stood at $2.75 Bn as on 26 February 2020. Recently, the company announced that it will distribute a dividend of $0.050per share, with an ex-date of March 05, 2020 and payment date of April 20, 2020.

1HFY20 Highlights for the Period ended 31 December 2019: The company recently announced that revenue in 1HFY20 came in $1,182.5 million, up 67% year over year. Group EBITDA stood at $250.8 million, up by 41% year over year. Statutory net profit from continuing operations declined 41% year over year and came in at $101.9 million. The company has also declared an interim dividend of 5 cents per share, flat year over year.

.png)

1HFY20 Key Highlights (Source: Company Reports)

Outlook: The company is anticipating the FTA market to experience a decline of 5% in the second half of 2020. As a result, FY20 pro forma group EBITDA is expected to be in line with FY19 pro forma EBITDA of $423.8 million.

Valuation Methodology:P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week low and high of $1.580 and $2.13, respectively. As per ASX, the stock has a PE multiple of 9.24x and an annual dividend yield of 6.19%, indicating a decent opportunity for accumulation. During the year, EBITDA margin improved from 18.8% in FY18 to 19.1% in FY19. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as Seven West Media Ltd (ASX: SWM), MNF Group Ltd (ASX: MNF), QMS Media Ltd (ASX: QMS), etc. We have arrived at a target price with an upside of lower double-digit (in percentage terms). Therefore, considering the above-mentioned factors, we give a “Buy” recommendation on the stock at the current market price of $1.72 per share, up by 6.502% on 26 February 2020, due to decent 1HFY20 results.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...