WiseTech Global Limited

Stellar Growth Across Each Segment: WiseTech Global Limited (ASX: WTC) provides software solutions to the logistics industry globally. The company is engaged in the development and implementation of software solutions which tracks storage of goods and its movement information. WTC operates in three segments, namely Recurring On-Demand, Recurring OTL (One-Time-Licence) maintenance, and OTL & support services.

Recently, WTC informed about the change in interest of the company’s director Christine Holman. He acquired 3,000 ordinary shares at an average price of $32.67 per share. Post this change, his current holdings stood at 8,717 ordinary shares.

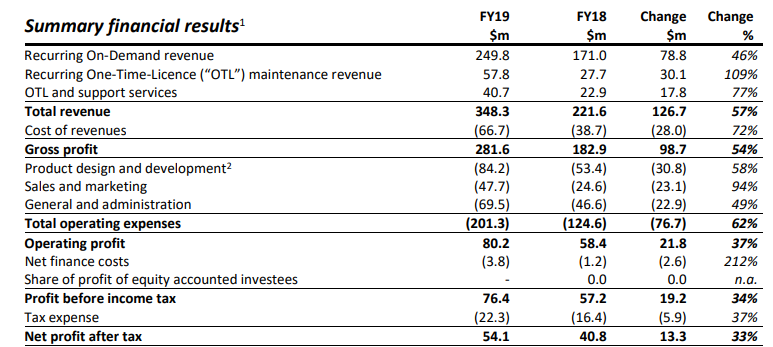

FY19 Financial Highlights:WTC came up with its FY19 results for the year ended 30 June 2019 wherein, the company posted a rise of 57% (y-o-y) in top-line and ~33% increase in bottom-line at $54.1 million. Operating profitduring the period stood at $80.2 million, up 37% on prior corresponding period. Revenue from existing customers grew by $46.8 million as compared with $32.1 million FY18 while WTC added revenue of $7.7 million as compared to $12.5 million in FY18 from new customers. Existing and new customer growth included $9.2 million of positive foreign exchange movements. Income from customers on acquired platforms increased by $72.2 million, up over 200% on y-o-y, which included $69 million from 29 acquisitions, completed during FY18 and FY19. Product designing and development stood unchanged at ~24% of total revenue while the company reported R&D expense at 32% of total revenue as compared with 34% in FY18. The company reported a lower customer attrition rate, at below ~1%, during FY19.

FY19 Financial Highlights (Source: Company Reports)

Revenue from Recurring On-Demand segment constituted ~72% of total revenue in FY19 as compared to 77% in FY18. Recurring OTL maintenance, and OTL & support services posted a rise of ~109% and ~77%, respectively. During FY19, the company was able to achieve a gross margin of ~81% as compared with 83% in FY18, reflecting efficient commercialization of flagship product CargoWise One.

Outlook:The management cited that transition of the acquired businesses will take time to build out the commercial foundation with WTC and henceforth, revenue growth from acquisitions are likely to remain flat or negative in coming years. The company expects its FY20 revenue to be around $440-$460 million while EBITDA is likely to come in at $145-$153 million.

Stock Recommendation:At the current market price of $36.850, the stock is trading at a higher price to earnings multiple of 208.640x. 52-week trading range for the stock stands at $14.885 - $37.550 and the stock is trading close to the upper band of its 52-week trading range. The stock has generated stellar returns of ~50.92% and ~83.18% in last three months and six months, respectively. The stock has moved up ~10.90% in the last five trading sessions on account of strong FY20 guidance. Currently, the stock is available at EV/Sales multiple of 31.5x on TTM basis against industry median of 4.5x. Gross margin for WTC came in at 80.9%, below the industry median of ~86.6%, while net profit margin at ~15.5% was slightly below the industry median ~15.9%. Considering the ratio metrics, valuations, and recent price movement, we are of the view that the stock is currently trading at higher valuations. Hence, we recommend an ‘Expensive’ rating on the stock at the current market price of $36.850 per share, down 0.217% on 02 September 2019.

Altium Limited

Double Digit Revenue Growth in FY19: Altium Limited (ASX: ALU) is a multinational software corporation, headquartered in San Diego, California. The company focuses on electronics design systems for 3D PCB design and embedded system development.

With a market update on 23 August 2019, ALU announced about the issue of additional fully paid ordinary shares of 454,253. The company will issue the above-stated number of shares in two installments - 138,256 Shares @ $8.49 per share and 315,997 Shares @ $NIL consideration to fulfil vesting Employee Performance Rights.

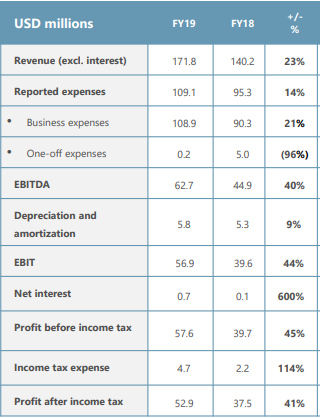

FY19 Financial Highlights:During FY19, the company reported decent revenue growth of 23% (y-o-y) at $171.8 million. Net profit of the company came at $52.9 million, up 41% on FY18, aided by a 13% growth in subscription at 43,600 subscribers. EBITDA came in at $62.72 million, up 40% pcp while EBITDA margin improved at 36.5% from 32% in FY18. Cash and cash equivalent increased ~54% at $80.53 million at the end of the period. The company reported strong performances across the US and EMEA with revenue growth of 14% and 20%, respectively. ALU reportedan increase of~27% in Altium Designer seats while it sold more than 8,000 new licenses. In revenue terms, Octopart delivered a rise of 49% while Board and Systems’ top line grew by 17% to US$126.8 million. ALU saw outstanding sales growth from the Chinese market at ~37% y-o-y.

FY19 Financial Highlights (Source: Company Reports)

Outlook:As per the Management guidance, FY20 revenue is targeted at US$200 million, followed by higher EBITDA margin higher floor of 37% (excluding the impact of the new leasing standard). The management forecasted to reach its halfway mark of 50,000 subscribers as early as 2020.

Stock Recommendation:The stock of ALU closed at $36.810 on 02 September 2019. The 52-week trading range for the stock stands at $19.730 and $38.490. The stock has delivered stellar returns of 70.15% and 29.93% on YTD and in one year, respectively and is currently, trading close to the higher band of its 52-week trading range.The stock is available at an EV/Sales multiple of 19.1x on TTM basis against its industry median of 4.5x. Annualised dividend yield for the stock stood at 0.92% as compared to 1.8% of the industry median. Considering the aforesaid factors and valuation, we believe that the stock is priced at expensive valuations. Hence, we give an “Expensive” recommendation on the stock at the current market price of $36.810, up 0.109% as on 02 September 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...