Suncorp Group Ltd

.png)

SUN Dividend Details

Operational challenges in General Insurance Business: Suncorp Group Ltd (ASX: SUN) stock plunged over 20.68% in the last six months (as of February 05, 2016) as the group’s General Insurance margin were under pressure during the six months ended on December 2015 due to $4 billion natural hazard events impact and falling Australian dollar. Management reported that their underlying Insurance Trading Ratio (ITR) would also be affected by $75 million rise in the natural hazards allowance, more than expected loss in Commercial Insurance, rising claims frequency in Compulsory Third Party (CTP) insurance in NSW as well as decrease in investment yields. Accordingly, ITR is forecasted to be about 10% in the six months ended on December 2015. Nonetheless, SUN expects these to be short term challenges which the company is poised to overcome.

.png)

Suncorp Group simplification and de-risking efforts (Source: Company Reports)

On the other hand, SUN is making optimization efforts which would lead to around $170 million of benefits in 2018. More insights will be revealed soon in the awaited financial results for the six months ended December 31, 2015. The heavy correction in SUN has however placed the stock at cheaper valuation which is trading at a reasonable P/E. The group also has a strong dividend yield. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $11.39

SUN Daily Chart (Source: Thomson Reuters)

Flight Centre Travel Group Ltd

.png)

FLT Dividend Details

Focusing on acquisitions to drive growth: Flight Centre Travel Group Ltd (ASX: FLT) has been making acquisitions and investments to drive growth in future. The group made an agreement with Professional Performance Systems Pty Ltd (PPS, which owns BYOjet.com) to acquire 70% stake currently and own entire stake by fiscal year of 2018. Flight Centre Travel also acquired StudentUniverse.com which is a youth and student travel specialist, for USD 28 million. With these two acquisitions, FLT would further strengthen its presence in the online travel segment. Flight Centre is also targeting Asian growth apart from its domestic growth, and accordingly acquired 40% stake at Worldwide Aviation Services, a Malaysian based corporate travel business which has an annual revenue of $250,000. On the other side,

FLT stock delivered returns of 12.38% in the last six months (as of February 05, 2016). Still, the stock is trading at reasonable P/E and has a decent dividend yield. We believe FLT stock could deliver further positive momentum and accordingly, we recommend investors to “HOLD” the stock at the current price of $38.50

.PNG)

FLT Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Dividend Details

Strong dividend yield: The shares ofAustralia and New Zealand Banking Group Ltd (ASX: ANZ) corrected over 26.06% in the last six months (as of February 05, 2016) impacted by the slowdown in China, tough market conditions and the group’s efforts to comply with APRA standards. On the other hand, ANZ was able to deliver over 20% increase in profits in Greater China region during 2015. The bank has strong domestic operations, as well as generated an overall cash profit increase of 80% to $7.2 billion in 2015 as compared to $3.9 billion in 2007.

.png)

Australia and New Zealand Banking Group’s performance (Source: Company Reports)

Australia and New Zealand Banking Group reported over 150,000 new retail customers in Australia in 2015. ANZ also enhanced Common Equity Tier 1 capital to 9.6% in 2015 against 4% in 2007, to comply with the APRA standards.

ANZ also has a strong balance sheet with robust loan-deposit ratio. Meanwhile, investors seeking for long term value stocks at bargain opportunity could consider adding ANZ to their portfolio as the bank is trading at reasonable valuation with a low P/E and an outstanding dividend yield. Accordingly, we reiterate our “BUY” recommendation on the stock at the current price of $24.09

.PNG)

ANZ Daily Chart (Source: Thomson Reuters)

REA Group Ltd

.png)

REA Dividend Details

Profit uplift and market leader position in domestic operations: REA Group Ltd (ASX: REA) delivered robust growth in all financial metrics for half year ended December 31, 2015 (i.e., half year 2016) with revenue surging by 20% and EBITDA growth of 29% over half year 2015. REA’s profit in the six months to December 31 surged 28% to $121 million on the prior corresponding period. The group’s realestate.com.au site has built a strong market presence in Australia and claims of having highly engaged property audience, and has witnessed more than twice the number of visits of number 2 site. REA reported that the average monthly visits on realestate.com.au surged by 33% to 42.7 million during the September quarter.

.png)

Half year 2016 financial performance (Source: Company Reports)

This result was the outcome of the revenue growth from Australian portals. The company also delivered a 21% yoy revenue increase to $146 million during the September of 2015 quarter driven by its strong ongoing rising volumes in the Australia market, while EBITDA from core operations surged by 30% yoy to $82 million. While having a strong foundation in the domestic markets,

REA is also eyeing Asian market opportunity for further potential growth and accordingly acquired iProperty Group. REA stock surged over 13.73% (as of February 05, 2016) in the last six months. We believe that the stock has positive momentum and accordingly recommend investors to “HOLD” the stock at the current price of $49.36

.PNG)

REA Daily Chart (Source: Thomson Reuters)

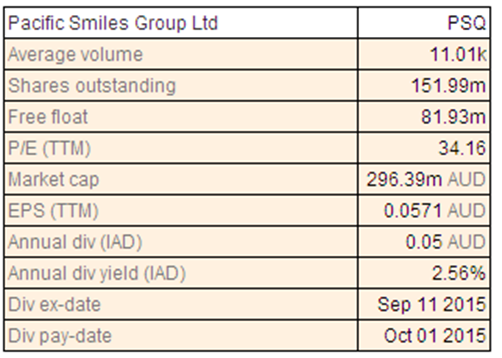

Pacific Smiles Group Ltd

PSQ Dividend Details

Strong operating cash flow and increasing dividends: Pacific Smiles Group Ltd (ASX: PSQ) shares corrected 12.56% in the last six months (as at February 05 2016). The company is set to release its half year results ended December 31, 2015 on February 19, 2016. Year 2015 appeared to be a significant year for the group with results for the financial year ended 30 June 2015, exceeding the pro forma earnings forecast provided in the prospectus for the Initial Public Offering. Pro forma net profit after tax was $ 9.7 million, up 31.9% on the previous year and up 8.8% over the forecast in the prospectus. The fully franked dividend of 3.33 cents per share was paid for the year and the total ordinary dividend declared for the year was 5 cents per share fully franked which represented 78% of pro forma net profit after tax and a 25% increase on the previous year. In addition, a pre-IPO special dividend of 1.6 cents per share was also paid. The group is leading the way in Australia with branded network approach to the dental services industry, the group now has 51 dental centres throughout eastern states and territories of mainland Australia and provides fully serviced surgeries to independent dentists who choose to practice from one of the dental centres.

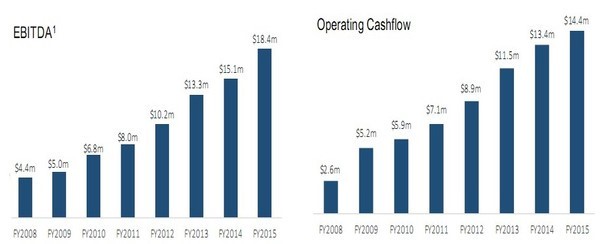

EBITDA and Operating Cashflow (Source: Company Reports)

Pro forma EBITDA was $ 18.2 million, up 25% over the previous year and exceeding the prospectus by 4.6%. Patient fees across the dental centre network was $ 121.4 million, up 26.6% over the previous year and 1.5% below prospectus forecast, while the same centre patient fees grew by 4.3%. The balance sheet remains very strong with $ 15.2 million of net cash and the network expansion continues to accelerate with the opening of eight new dental centres compared to four in the previous year.

At the end of the year, the company had 49 centres in total. We are optimistic about the growth prospects and the future of this group and would rate the stock as a “SPECULATIVE BUY” at the current price of $1.88

PSQ Daily Chart (Source: Thomson Reuters)

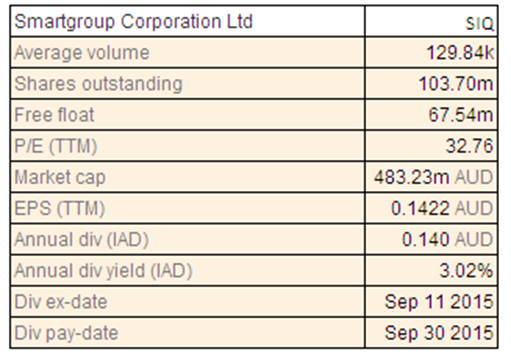

Smartgroup Corporation Ltd

SIQ Dividend Details

Expanding service capabilities through acquisitions: Smartgroup Corporation Ltd (ASX: SIQ) shares surged 29.18% in the last three months but corrected about 11.11% in the last one month (as at February 05, 2016). SIQ has completed the acquisition of Trinity Management Group assets for an initial payment of $1.7 million. Based on this, the company indicated for pro-forma forecast calendar year 2016 (CY16) revenues of $3 million and EBIT of $1.2 million. The group also had provided a trading update for the period ending 31 December 2015 and the update is preliminary and subject to the year-end audit and sign off. The group expected to report CY15 revenue growth (~$ 90 million) of 24% over the previous year; CY15 EBITDA growth of 46% (~$ 36 million) over the previous year; CY15 NPATA of $ 26 million, which is a 49% increase on the previous year and CY15 NPATA per share of $ 0.25, which is a 46% increase on the previous year. These figures are unaudited and excluding any impact of the Advantage Salary Repackaging acquisition, including a one-off after-tax acquisition expense of $ 0.8 million to be booked in the second half of 2015. Advantage Salary Packaging acquisition opportunity consisted of expanding Public Benevolent Institutions (PBI) footprint to a broader segment of the outsourced salary packaging market, including charities and aged care, the potential to grow novated leasing offerings under group ownership, a good cultural fit and alignment with management.

The key terms of the acquisition entailed an agreement to acquire 100% of Advantage Salary Packaging for $ 60.8 million (revenues of $ 14.7 million and EBITDA of $ 10.3 million). Given the ongoing efforts, we believe to adopt a wait and watch approach and thus recommend “HOLD” at the current price of $4.56

SIQ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...