Spark New Zealand Ltd

.png)

SPK Dividend Details

Growth in Mobile market revenue: Spark New Zealand Ltd (ASX: SPK) recently provided the financial results for the six months to 31 December 2015 with total operating revenue and other gains dropping by 4.1% to $1,723 million in H1 FY16. However, the underlying total operating revenues and other gains rose by 1.6%, i.e., by $27 million, after re-basing for changes from earlier divestments, changes to the way regulated access charges for Spark Wholesale are billed and the acquisition of CCL Group. FY15 return to EBITDA growth has been witnessed in H1 FY16. SPK’s Mobile and IT Services revenue growth exceeded decline in fixed legacy. The company is now positioning itself as #1 in Mobile revenue share which is driven by 12% revenue growth. SPK’s financial year 2016 guidance with reported EBITDA is estimated to record a 0-3% growth from $962 million recorded in financial year 2015.

.png)

Performance (Source: Company reports)

Capital expenditure is assumed to be around $380 million compared to $418 million in financial year 2015. Dividends per share is forecasted at 22 cents per share and an additional special dividend of 3 cents per share. This is in comparison to 20 cents per share paid in financial year 2015. With a solid dividend yield, we remain bullish on the stock and rate a “BUY” at the current share price of $3.04

SPK Daily Chart (Source: Thomson Reuters)

Village Roadshow Ltd

.png)

VRL Dividend Details

Accretive acquisition growth: Village Roadshow Ltd (ASX: VRL)continues to drive growth through acquisitions and recently acquired 80% of the U.K based Opia business for GBP 24 million (adjusted for surplus cash, with deferred consideration payable if future earnings targets are met), with existing senior management of Opia retaining 20% holding. The acquisition of Opia is expected to be earnings accretive and to contribute positive cash-flow to VRL from acquisition date and synergies from the combined Edge/Opia businesses are expected to generate incremental revenue.

.png)

Yearly Financial summary (Source: Company reports)

Opia’s EBITDA is expected to be approximately GBP 6 million per annum in the first full year of acquisition and VRL’s share of this will be 80%. The net profit after tax contribution from Opia in the first full year of consolidation is expected to be approximately GBP 2.6 million (A$5.8 million). VRL also has a decent dividend yield. Based on the foregoing, we give the stock a “BUY” at the current share price of $6.53

.png)

VRL Daily Chart (Source: Thomson Reuters)

Super Retail Group Ltd

.png)

SUL Dividend Details

Restructuring efforts to revamp growth: Super Retail Group Ltd (ASX: SUL) reported a net profit for the financial year 2015 attributable to shareholders of $81.1 million compared with $108.4 million in the previous year representing a reduction in earnings per share from 55.1 cents to 49.4 cents.

This result was adversely impacted by the company's decision to undertake significant restructuring activities to address performance issues in a number of the smaller businesses.However, during the year the company generated a strong cash flow with net cash flow from operating activities of $182 million, an increase of $14.8 million on the previous period. Looking ahead, the company plans to open a total of 30 new stores in the current financial year with estimated capital expenditure in 2015/16 at $100 million with the major portion being on new and refurbished stores. SUL has a good dividend yield and we issue a “BUY” on SUL at the current share price of $10.14.

SUL Daily Chart (Source: Thomson Reuters)

Retail Food Group Ltd

.png)

RFG Dividend Details

New stores and strong outlook: Retail Food Group Ltd (ASX: RFG) entered 2016 on a positive note with the commissioning of its 2,500

th outlet. Moreover, management stated that its continued network expansion was being driven by high demand for innovative retail concepts in the domestic market as well as strong international growth.

.png)

Strong Dividend Returns (Source: Company reports)

In its recent trading update, the company provided its financial year 2016 outlook stating it is on track to achieve first half 2016 underlying net profit after tax growth of 25% while on a like for like basis, the prior comparable period increase will be 35%. The Company has also reaffirmed FY16 guidance of 20% underlying NPAT growth on FY15. With a strong dividend yield, we rate the stock a “BUY” at the current share price of $4.50

RFG Daily Chart (Source: Thomson Reuters)

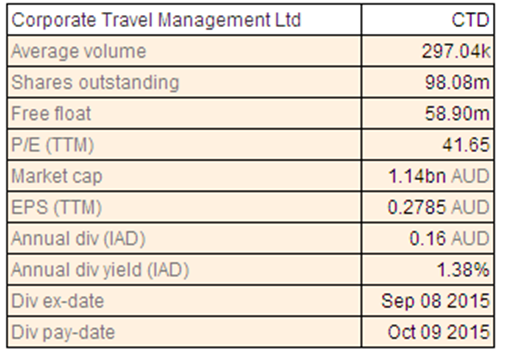

Corporate Travel Management Ltd

CTD Dividend Details

Focusing on the US market:Corporate Travel Management Ltd (ASX: CTD) is strengthening its US market penetration and accordingly acquired Montrose Travel from Los Angeles area, California which is a major travel company. With this move, CTD would be operating in 19 cities in the USA while the group’s North America’s Total Transaction Value is expected to reach over $1 billion by this year on an annual basis. Moreover, the group generated a solid fiscal year of 2015 performance, wherein its underlying EBITDA rose by 70% year on year (yoy) to $49.1 million, better than its upgraded guidance of >$48 million. CTD’s half of the profits growth was organic and the company reported a solid revenue growth in all of its regions. As a result, CTD delivered a full year dividend increase of 33% to 16 cents fully franked during the year.

On the other hand, the shares of CTD fell over 9.3% during this year to date (as of February 18, 2016) on investor’s concerns over the current tough market conditions’ impact on the group’s performance. However, we believe that CTD’s ongoing penetration in domestic and international markets would continue to generate growth in the coming months. Accordingly, we give a “HOLD” recommendation on this stock at the current price of $11.68

CTD Daily Chart (Source: Thomson Reuters)

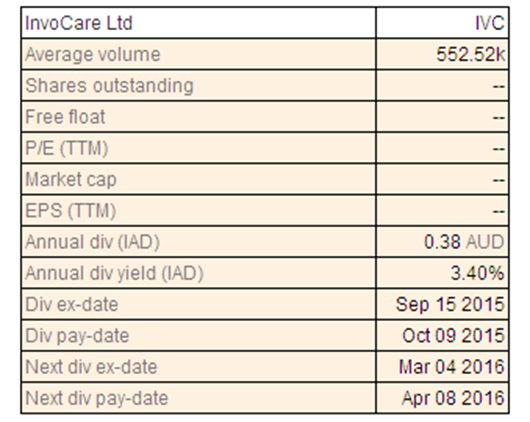

InvoCare Ltd

IVC Dividend Details

Higher valuations:InvoCare Ltd.’s (ASX: IVC) FY15 total sales of $436m rose by 5.7% yoy. The operating earnings after tax (excluding asset sales and undelivered prepaid contract impacts) rose by 6.9% to $49.4 million for the full year against $46.2 million in the previous year. This increase was mainly contributed from Australia and Singapore segments. Margin improvement in Australia was driven by continued focus on costs. Funeral case volumes jumped up by 2.7% over the prior corresponding period (pcp) while the operating expenses rose 6.7% over the pcp. The performance is, however, also subject to the death rate which in turn is dependent on ageing population and respective medical assistance. Despite the results and the recent correction, the stock is trading at relatively expensive valuations with an unreasonable P/E. Accordingly, we issue an “Expensive” recommendation on this stock at the current price.

IVC Daily Chart (Source: Thomson Reuters)

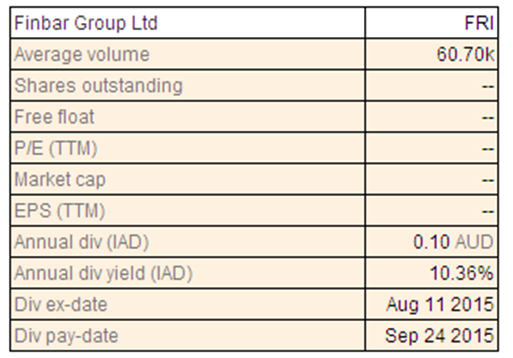

Finbar Group Ltd

FRI Dividend Details

Ongoing project developments:Finbar Group Ltd (ASX: FRI) stock plunged over 27.86% (as of February 18, 2016) in the last one year impacted by the investors’ concerns on the group’s performance due to ongoing slowdown in the global markets. However, the group continued to build its development pipeline to generate long term growth. Finbar won Palmyra joint venture project worth over $109 million wherein Finbar’s share is 50%. Marketing for this project is expected to start this year. FRI also got the development approval for South Perth, which has over 42 apartments with 1,800 square meters of commercials. This project’s end value is over $50 million while the marketing is expected to start by May 2016. Finbar Group received development approval for Belmont Project which has 194 apartments and two commercial lots.

Belmont Project’s marketing is estimated to start by the first half of 2016 and construction is expected to start by 2017. Meanwhile, the recent correction in FRI placed the stock at very cheaper valuations with a lower P/E. Finbar has an outstanding dividend yield. Based on the foregoing, we reiterate our “BUY” recommendation on the stock at the current price of $0.92

FRI Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...