Stocks’ Details

Domino's Pizza Enterprises Limited

Reopening of Stores: Domino's Pizza Enterprises Limited (ASX: DMP) is a food retailer, which operates a pizza chain comprising franchisee owned and company-owned corporate stores. The market capitalisation of the company stood at ~$5.42 billion as on 17th June 2020. In a recent update related to COVD-19, the company stated that its stores in all operating markets continue to adapt to changes in customer behaviour, community expectations, various support measures as well as local trading conditions. From the first week of April 2020, the company’s stores in France have started reopening progressively. As of now, around 70% of stores have reopened in France.

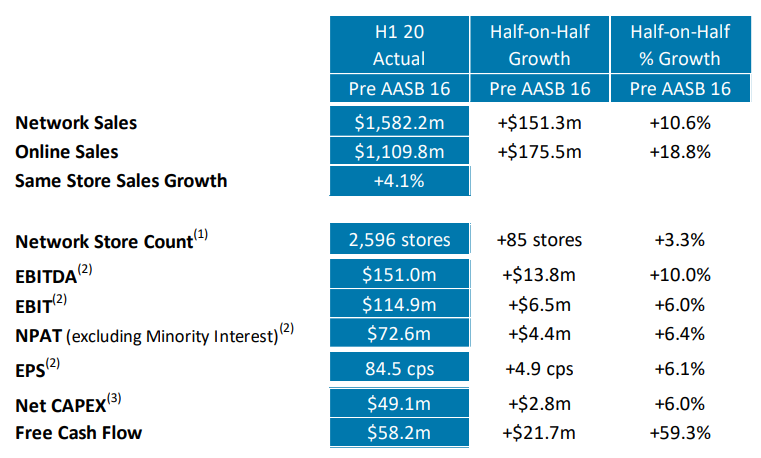

During 1H FY20, the company reported a rise of $151.3 million to $1.58 billion in sales. Over the past five years, DMP's sales have been more than doubled and online sales more than tripled. DMP is on track to surpass $3 billion in global food sales during FY20.

Key Sales Number (Source: Company Reports)

Opening of New Stores: Over the medium term, the company expects net capex in the range of $60 - $100 million per year. The company also expects the opening of new stores in the upcoming period.

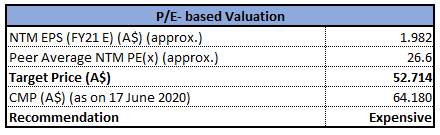

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: The company added that the COVID-19 pandemic has presented short-term uncertainty for some franchisees, which would delay the opening of stores that were planned for FY20. Moreover, store openings in FY21 are likely to be dependent on local market conditions relating to COVID-19.

Stock Recommendation: DMP possesses a strong balance sheet, with significant headroom on its committed debt facilities and covenants. Domino’s has no committed short-term debt, with committed debt facilities due for renewal in 1H FY23.We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with the correction of low double-digit (in percentage terms). For the purpose, we have taken peers such as Woolworths Group Ltd (ASX: WOW), Wesfarmers Ltd (ASX: WES) and Collins Foods Ltd (ASX: CKF). The stock of DMP is trading closer to its 52-week high level of $66.960. Thus, it can be said that the stock of DMP is overvalued at current trading levels. Hence, considering the current trading levels and expected correction, we give an “Expensive” rating on the stock at the current market price of $64.180 per share, up by 2.165% on 17th June 2020.

Woolworths Group Limited

Pricing of Senior Unsecured Notes: Woolworths Group Limited (ASX: WOW) is into food, general merchandise, and specialty retailing via chain store operations. The market capitalisation of the company stood at ~$45.82 billion as on 17th June 2020. Recently, the company successfully priced senior unsecured five-year notes of $400 million and $600 million of ten-year notes (Notes) under its Euro Medium Term Note Programme. The Notes have been priced at 1.85% for the five-year notes and 2.80% for the ten-year notes. WOW would use the proceeds for the refinancing of future debt maturities of around $1 billion later in the calendar year 2020.

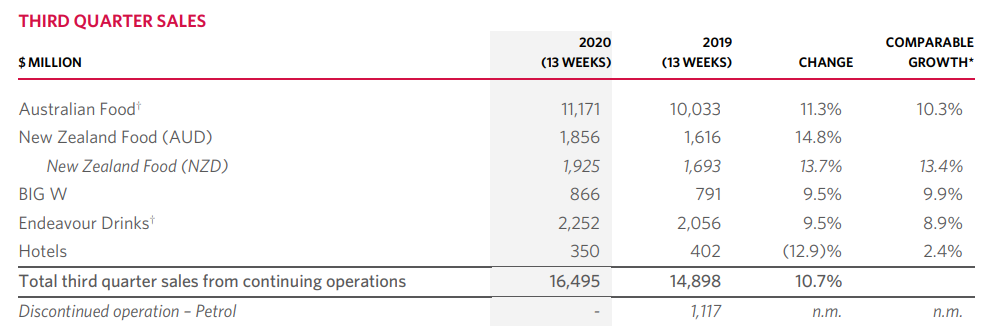

During Q3 FY20, the company reported sales from continuing operations amounting to $16.5 billion, reflecting a rise of 10.7% while the online sales went up by 34.0% to $817 million. The company also experienced a decent sales growth of 11.3% and 13.7% in Australian Food and New Zealand food segments, respectively.

Key Summary Q3 FY20 (Source: Company Reports)

Anticipated Costs: During Q4 FY20, the company is likely to experience incremental costs in the range of $220 million - $275 million. Also, the company is not in the capacity to evaluate the net impact of COVID-19 on the financial year 2020 result.

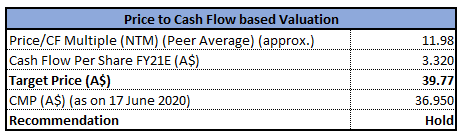

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: As the company operates in a retail environment, it is exposed to numerous strategic, operational, compliance and financial related risks.

Stock Recommendation: The company is in a strong operational and financial position. WOW has significant headroom under rating agency metrics and banking covenants. Over the past five-years (2015-2019), the company has maintained positive free cash flow, reflecting prudent use of working capital. Debt to equity of the company stood at 1.92x in 1H FY20 as compared to the industry median of 1.58x. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Wesfarmers Ltd (ASX: WES), Coca-Cola Amatil Ltd (ASX: CCL), JB Hi-Fi Ltd (ASX: JBH).

Thus, considering the strong operational and financial position, decent growth in sales and prudent use of working capital, we give a “Hold” recommendation on the stock at the current market price of $36.950 per share, up by 1.847% on 17th June 2020.

Premier Investments Limited

Reopening of Stores: Premier Investments Limited (ASX: PMV) operates numerous specialty retail fashion chains within the specialty retail fashion markets in Australia, New Zealand, Asia, and Europe. The market capitalisation of the company stood at $2.52 billion as on 17th June 2020. The company recently announced that one of its Directors, Mr. Mark Mcinnes has made a change to holdings in the company by acquiring 250,000 ordinary shares on 18th May 2020. In another update, the company announced the reopening of the balance of its stores in Australia in line with Step 1 of the Australian Government’s “3 Step Framework for a COVIDSafe Australia. Moreover, PMV’s stores in New Zealand has been reopened from 14th May 2020.

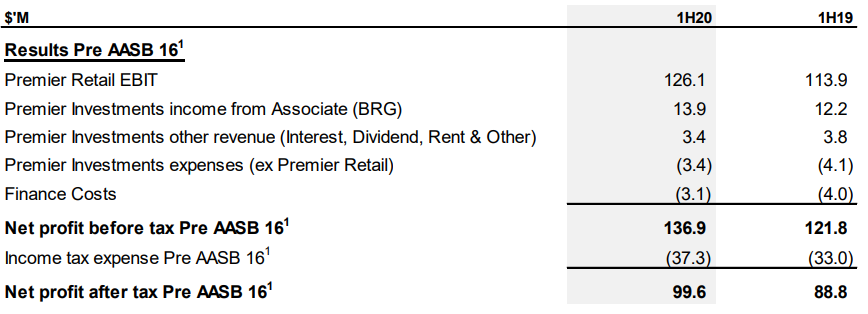

During 1H FY20, PMV reported NPAT amounting to $99.6 million with a rise of 12.2% over 1H FY19. In order to please shareholders, the company has declared a fully franked interim dividend of 34 cps.

Key Financials (Source: Company Reports)

Future Aspects: The company is optimistic about the future growth of the business. However, PMV is not able to assess the impact of COVID-19 on the earning for 2H FY20.

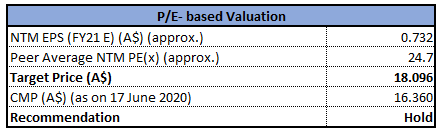

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: In the upcoming phase of economic recovery, the Premier Retail’s sales and margin by store, by country, by brand and by region are highly uncertain.

Stock Recommendation: As at 1 May 2020, the cash position of the company stood at $256.2 million and it maintains access to undrawn facilities of $91.8 million, placing the Group in a decent position to begin the recovery. Current ratio of the company stood at 1.26x in 1H FY20 as compared to the industry median of 1.18x. This reflects that the company is in a decent position to address its short-term obligations.PMV also maintains a strong balance sheet. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers such as Bapcor Ltd (ASX: BAP), Breville Group Ltd (ASX: BRG), Accent Group Ltd (ASX: AX1), etc.

Hence, in light of the current trading levels, decent liquidity position, strong balance sheet and reopening of stores, we give a “Hold” recommendation on the stock at the current market price of $16.360 per share, up by 3.023% on 17th June 2020.

Baby Bunting Group Limited

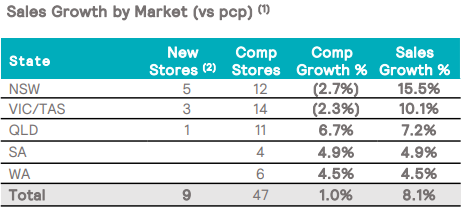

Decent Growth in Sales: Baby Bunting Group Limited (ASX: BBN) is engaged in retailing of baby goods. The market capitalisation of the company stood at ~$386.52 Mn as on 17th June 2020. In a recent business update, the company stated that during the 2H (30 December 2019 to 17th May 2020), the company’s total sales growth stood at 13.2%. The sales performance indicates the less discretionary nature of the baby category. During 1H FY20, the company experienced a total sales growth of 8.1%, primarily driven by decent performance from new stores.

The company made some adjustments to its capital expenditure program and introduced a prudent cost management program in the month of March and April 2020 in anticipation of potential future cash flow pressures.

Sales Growth (Source: Company Reports)

Suspension of Guidance: Previously, the company has suspended its guidance for FY20 because of increasing uncertainty arising from the unknown potential impact of COVID-19.

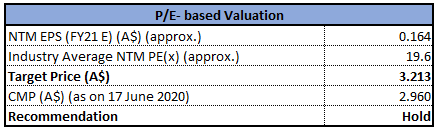

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: BBN is exposed to economic, environmental, and social sustainability risks, which impacts the ability of the company to operate at a level of economic production over the long-term.

Stock Recommendation: During the pandemic period, the company’s stores were open as the nature of its business comes under essential services. The company possesses a strong balance sheet with undrawn debt facilities of around $35 million. During 2016- 2019, the company reported a CAGR of 155.42% in free cash flows, reflecting prudent use of working capital. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of high single-digit (in percentage terms). Thus, considering the strong balance sheet, effective use of working capital and growth in sales, we give a “Hold” recommendation on the stock at the current market price of $2.960 per share, down by 2.31% on 17th June 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...