.png)

Stocks’ Details

Woolworths Group Limited

Decent Start to FY20:Woolworths Group Limited (ASX: WOW) is engaged in food, general merchandise and specialty retailing with the help of chain store operations. The market capitalisation of the company stood at A$46.94 Bn as on 10th January 2020.The company experienced a strong 2H FY19 even with the challenging start to the year. The sales from continuing operations experienced a rise of 3.4% on a normalised basis and EBIT on the same basis witnessed a rise of 5.0% in FY19. The online sales of the group continued to grow strongly with a rise of 32% on a normalised basis and the figure stood at $2.5 billion.

For Q1 FY20, the company reported sales from continuing operations of $15.9 Bn with a rise of 7.1% and the online sales stood at $802 million.The Australian food sales were increased by 7.8% to $10.7 Bn. Notably, Australian Food sales growth was because of the successful Lion King Ooshies and Woolworths Discovery Garden campaigns as well as online.

.png)

Q1 FY20 Sales (Source: Company Reports)

What to Expect:The company is focused on providing the best possible customer experience throughout all of its businesses as it manages a material change agenda in the 1H. This includes the implementation of its new customer operating model in Woolworths supermarkets, the launch of Fresh Made Easy as well as the ramp-up of the MSRDC (Melbourne South Regional Distribution Centre). However, for FY20, the company anticipates headwinds from a challenged consumer environment, the cost impact of its new enterprise agreements and input cost pressures.

Valuation Methodology: P/E Based Approach

.png)

P/E Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: For Q1FY20, the company stated that the WooliesX further enhanced the connected customer as well as a digital experience with the relaunch of its delivery subscription model named as Delivery Unlimited. We have valued the stock using the P/E based approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering the decent start to FY20, strong 2HFY19 performance, and favourable valuation, we give a “Hold” recommendation on the stock at the current market price of A$37.820 per share, up by 1.612% on 10th January 2020.

Metcash Limited

A Look at 1HFY20 Results: Metcash Limited (ASX: MTS) happens to be a wholesaler to independent retailers in the food, grocery, liquor, hardware and automotive industries. The market capitalisation of the company stood at A$2.32 Bn as on 10th January 2020. The company recently announced that Allan Gray Australia Pty Ltd and its related bodies corporate, as an investment manager for the funds or investment mandates has made a change to their substantial holdings in the company on 2nd January 2020 and the current voting power stands at 14.64% as compared to the previous voting power of 13.60%.

For the half-year ended 31st October 2019 (or 1H FY20), the company reported a rise of 1.2% in total food pillar sales.For the first time since FY12, the Supermarkets wholesale sales excluding tobacco were positive.

.png)

1H FY20 Results (Source: Company Reports)

Looking for Opportunities:As per the release, the growth in Supermarkets wholesale sales ex tobacco posted in 1H FY 2020 continued in the first five weeks of 2HFY20, which excludes the impact of Drakes. In 2HFY20, the company anticipates that total supermarkets sales would be adversely impacted by ceasing to supply Drakes in South Australia from 30 September 2019. MTS continues to look for opportunities in order to exit onerous lease contracts, though the contribution to profit from this activity in future periods is anticipated to decrease.

Valuation Methodology: P/B Based Approach

.png)

P/B Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company added that the market fundamentals for Hardware remain positive over the medium to longer term. The construction activity is anticipated to be supported by population growth as well as an undersupply of housing. We have valued the stock using the P/B based valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering the decent performance in 1HFY20, outlook and valuation, we give a “Buy” recommendation on the stock at the current market price of A$2.520 per share, down 1.176% on 10th January 2020.

Super Retail Group Limited

Sales Growth in First 16 Weeks of 2019/2020:Super Retail Group Limited (ASX: SUL) is in the operations of specialty retail stores in the automotive, tools, leisure and sports categories. The market capitalisation of the company stood at A$2.01 Bn as on 10th January 2020.Recently, the company announced that UBS Group AG and its related bodies corporate has become an initial substantial holder in the company on 23rd December 2019 with the voting power of 5.86%. Even with the relatively subdued economic conditions, the group delivered a solid result for the financial year 2019. The company experienced a growth of 5.4% in total sales and delivered LFL sales growth throughout all its divisions. Moreover, the group has reported total sales growth of 4.2% and like for like sales growth of 3.2% in the first 16 weeks of 2019/2020.

.png)

Sales Growth of Four Divisions for First 16 Weeks (Source: Company Reports)

Focused on Investment:For the growth of core 4 brands, the company is focused on investment in Supercheap Auto, Rebel, BCF and Macpac. It is planning to execute organic growth opportunities in 1) Supercheap Auto services, 2) Rebel top 25 store performance, 3) BCF underpenetrated online, and 4) Macpac store expansion and hub strategy.

Valuation Methodology: P/E Based Valuation Approach

.png)

P/E Based Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:Net margin of the company stood at 5.1% in FY19 as compared to the industry median of 3.4%. This reflects that the company possesses better capabilities to convert its top-line into the bottom-line as compared to the broader industry. Return on equity of the company stood at 17.5% in FY19 against the industry median of 14.5%, reflecting better returns provided to the shareholders. We have valued the stock using the P/E based valuation approach and arrived at a target price, offering an upside of lower double-digit (in percentage terms). Therefore, considering the strong start to FY20, decent returns provided to shareholders and improvement in key margins, we maintain a “Hold” rating on the stock at the current market price of A$10.070 per share, down 1.178% on 10th January 2020.

Coles Group Limited

Decent Set of Sales Number in Q1 FY20: Coles Group Limited (ASX: COL) is engaged into retailing of products like fresh food, groceries, household goods, liquor, fuel and financial services via stores and online. As on 10th January 2020, the market capitalisation of the company stood at A$20.3 billion. The company recently announced that BlackRock Group and subsidiaries have ceased to be a substantial holder in the company with effect from 6th January 2020. In another update, the company announced that, Coles Group Treasury Pty Ltd (which is wholly owned subsidiary) has priced $600 million of fixed rate Australian dollar medium-term notes. These notes comprise $300 million of 7-year notes and $300 million of 10-year notes. Q1 FY20 was proved as the first quarter of positive comparable fuel volume growth in four years, and in the same time span, the company reported a rise of 1.8% in sales revenue to $8.7 billion.

.png)

Q1 FY20 Sales (Source: Company Reports)

What to Expect:COL is committed to operate in a way which is transparent and builds trust with its team, customers and community. The company might undertake future acquisitions and divestments and may enter into other third-party relationships so that it can more effectively execute its strategy.

Valuation Methodology: EV/EBITDA Based Approach

.png)

EV/EBITDA Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company’s RoE stood at 32.6% in FY 2019 which is higher than the industry median of 13.3%. Therefore, it can be said that COL has provided better returns to its shareholders as compared to broader industry. Notably, its net margin stood at 2.8% in FY19 as compared to the industry median of 2.0%. We have valued the stock using EV/EBITDA Multiple approach and arrived at a target price, which is offering an upside of mid-single digit (in percentage terms). Thus, on the back of decent performance in Q1FY20, outlook, and expected upside, we give a “Hold” recommendation on the stock at the current market price of A$15.660 per share, up 2.891% on 10th January 2020.

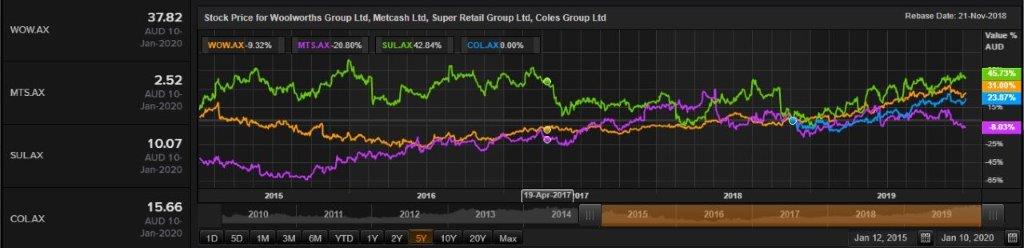

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...