.png)

Stocks’ Details

Resolute Mining Limited

Extension of US Dollar Denominated Gold Hedge Position: Resolute Mining Limited (ASX: RSG) is a gold mining company engaged in the development of resource projects and prospecting and exploration for minerals. As on 27th December 2019, the market capitalization of the company stood at $1.06 billion. The company has recently announced that it has extended its US dollar denominated gold hedge position and has forward sold an additional 30,000 ounces of gold at an average price of US$1,501 per ounce, which is scheduled monthly deliveries of 5,000 ounces between the time span from July 2020 and December 2020.

Strong Quarterly Performance: The repair of Syama Roaster resulted in a strong quarterly performance, wherein the company produced 103,201oz of gold at an AISC of US$1,202/oz. For the quarter ended 30 September 2019, the company made gold sales of 127,265oz at an average gold price of US$1,362/oz.

.png)

Quarterly Production and Costs (Source: Company Reports)

Future Opportunities:The company expects that Stage 2 of the Ravenswood Expansion Project would be commenced during 2020 with a timeline to complete implementation in around 24 months post investment decision. The company further expects that the production lost from the Syama roaster downtime is expected to be compensated by the processing of stockpiled transitional ore mined from the Beta satellite open pit. RSG has also revised its group AISC guidance and expects it to be US$1,020/oz. The company has also announced that it has completed the stage 1 of Ravenswood Expansion Project, which is targeting a production of approximately 80,000oz of gold at an AISC of around A$1,600/oz in 2020.

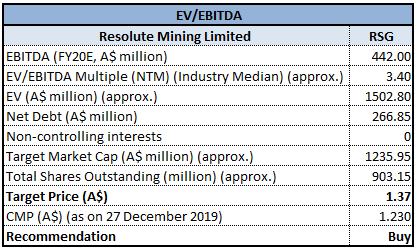

Valuation Methodology:EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gave a return of 8.80% in the last one month and trading at the lower band of its 52-weeks’ trading range of $0.965 - $2.120, proffering a decent opportunity for accumulation. For 1H19, gross margin of the company improved and stood at 21.3%, up from 11% in the second half of FY18. Considering the price movement, current trading levels, improvement in gross margin and decent outlook, we have valued the stock using EV/EBITDA based relative valuation method and arrived at the target price of lower double-digit upside, in percentage terms. Hence, we recommend a “Buy” rating on the stock at the current market price of $1.230, up by 4.681% on December 27, 2019.

Bellevue Gold Limited

Continues to Expand with Further High-Grade Results: Bellevue Gold Limited (ASX: BGL) is engaged in gold exploration at Bellevue Gold Project. As on 27 December 2019, the market capitalization of the company stood at $299.21 million. The company announced further high-grade drill results from extensive drilling at Deacon Lode discovery, which include 2.3 m @ 39.0 g/t from 819 m in DRDD273, 3.0 m @ 10.4 g/t from 587.5 m in DRDD295, 0.8 m @ 69.2 g/t from 577.8 m in DRDD290, 3.0 m @ 12.0 g/t from 571 m in DRDD313, 1.1 m @ 22.2 g/t from 658.9 m in DRDD106 ext. The company has started early site works and has also appointed Craig Jones as the Chief Operating Officer.

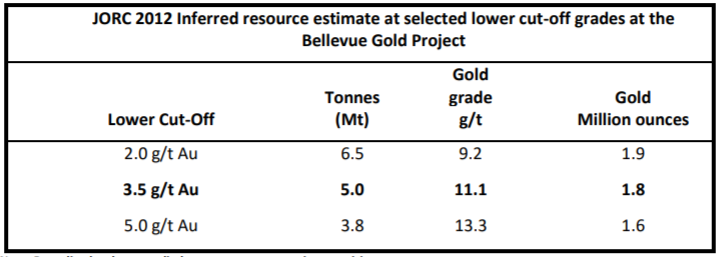

As at 30 September 2019, BGL had a strong cash position of $32.8 million and has delineated 1.8 Moz gold in less than 18 months from discovery. The latest upgrade at Bellevue Gold Project represents a 25% increase in global tonnes, a 17% increase in contained metal and only a 5% reduction in global grade.

Upgrade at the Bellevue Gold Project (Source: Company Reports)

What to Expect from BGL, Going Forward:The recent institutional placement will enable BGL to undertake significant infill drilling to further define its existing resource base, in addition to expanding its step-out exploration drilling program over the next year. The Company will continue to develop the exploration of the Bellevue Gold Project and regional areas.

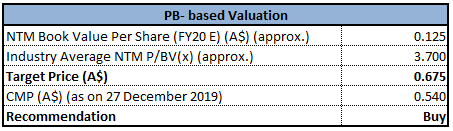

Valuation Methodology:Price/Book Value Multiple Approach

Price/Book Value Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gave a return of 15.38% in the past one month. During FY19, current ratio stood at 3.71x, higher than the industry median of 1.81x. This indicates that the company has sufficient liquidity to pay its short-term obligations. Debt/Equity stood nil as compared to the industry median of 0.13x. Considering the returns, higher margins and decent outlook, we have valued the stock using Price/Book value based relative valuation approach and arrived at a target price of double-digit upside, in percentage terms. Hence, we recommend a “Buy” rating on the stock at the current market price of $0.540, up by 2.857% on December 27, 2019.

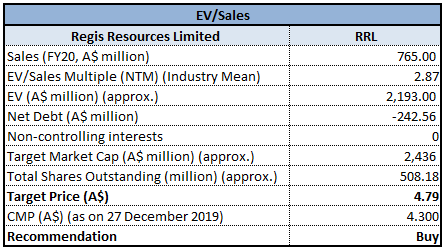

Regis Resources Limited

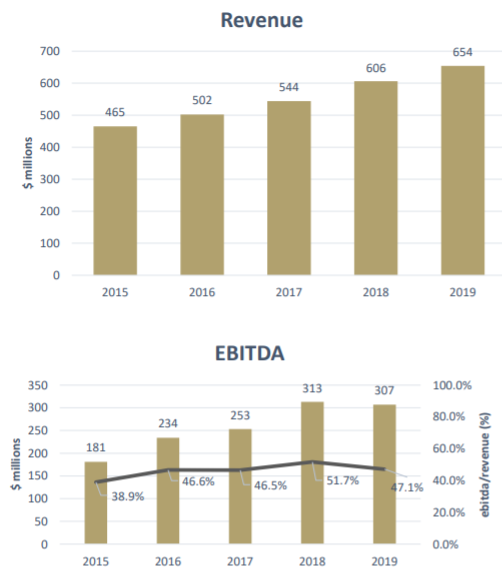

Decent Performance on Profit Measures: Regis Resources Limited (ASX: RRL) is engaged in gold and mineral exploration. As on 27 December 2019, the market capitalization of the company stood at $2.13 billion. The company has recently appointed Stuart Gula as Chief Operating Officer. During FY19, the company reported a strong balance sheet with zero debt and a cash balance of $147 million. In the same time span, the company reported revenue of $654 million, up from $606 million. EBITDA of the company stood at $306.8 million with EBITDA margin of 47%. The company also gave a record annual gold production of 363,418 ounces with AISC of $1,029 per ounce for FY2019.

Financial Performance (Source: Company Reports)

Growth Opportunities: The company has provided a gold production guidance and expects it to come in the range between 340,000oz to 370,000oz with an AISC between $1,125/oz and $1,195/oz and Growth Capital of approximately $62 million for FY2020.

Valuation Methodology:EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-weeks’ low of $4.005. In the time span of 4 years from FY15 to FY19, the company witnessed a CAGR of 8.92% in revenue and a CAGR of 16.79% in gross profit. During FY19, EBITDA margin of the company stood at 47.8%, higher than the industry median of 28.7%. In the same period, return on equity was 24.1% as compared to the industry median of 12%. Considering the trading levels, gross profit CAGR, higher EBITDA and ROE and decent growth opportunities, we have valued the stock using EV/Sales based relative valuation approach and arrived at a target price of lower double-digit upside, in percentage terms. Hence, we recommend a “Buy” rating on the stock at the current market price of $4.300, up by 2.625% on December 27, 2019.

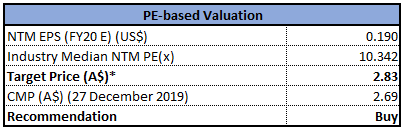

OceanaGold Corporation

OGC’s Share Surged ~7% Over Increase in Oil Prices:OceanaGold Corporation (ASX: OGC) is a multinational, mid-tier gold mining company with significant global operating, development and exploration experience. Recently, Dr. Nora L. Scheinkestel ceased to be the company’s Director, effective from 19 December 2019.

In another update, the company amended its existing $200 million Revolving Credit Facility with its banking partners, reflecting the strong confidence of lenders in the business. The major changes include the elimination of the 2019 amortisation or “step-down” with the Facility remaining at $200 million, combined with an extension of the Facility now maturing in December 31, 2021.

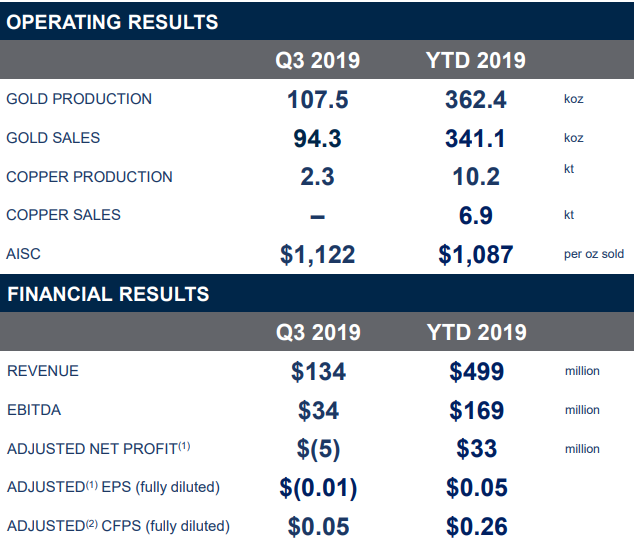

September’19 Quarter Key Highlights:Revenue for the period was reported at $134 Mn, reflecting a fall from Q2FY19 revenue of $186 Mn, mainly due to “nil” sales from Didipio, partially offset by the higher gold price received. The company had a similar quarter on quarter production at Haile & Macraes and produced 107.5 koz of gold at a group AISC (All in Sustaining Costs) of $1,122 per oz sold.

Quarterly Operating and Financial Performance (Source: Company Reports)

What to expect:FY19 production at Macraes and Haile is expected to rise and be in the range of 460,000 and 480,000 ounces of gold and 10,000 to 11,000 tonnes of copper. The consolidated All-In Sustaining costs (AISC) for FY19 has been anticipated between US$1,040 and US$1,090 per ounce sold.

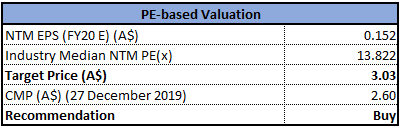

Valuation Methodology: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months, *1 US$ = 1.44 A$

Stock Recommendation:The stock generated a negative YTD return of 51.27%. Gross margin stood at 41.3% in Q3FY19, higher than the industry median of 7.5%. EBITDA margin for Q3FY19 came in at 26% as compared to the industry median of 3.3%. Considering the improvement in gross and EBITDA margin and modest outlook along with current trading levels, we have valued the stock using one relative valuation method, i.e., Price to Earnings (PE)multiple, and arrived at a target price of lower double-digit upside (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.690, up by 7.6% on December 27, 2019.

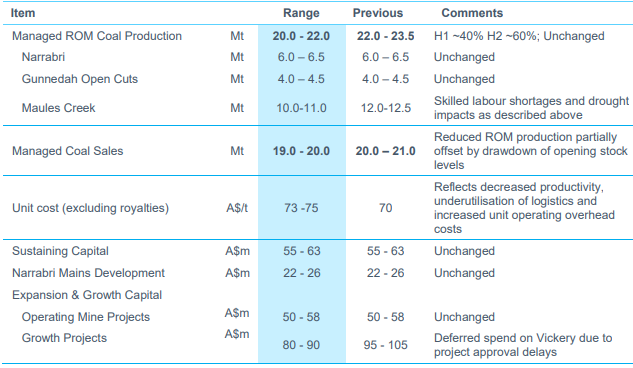

Whitehaven Coal Limited

WHC Revises FY20 Guidance:Whitehaven Coal Limited (ASX: WHC) is engaged in the business of development and operation of coal mines in New South Wales. Recently, Lazard Asset Management Pacific Co increased its stake from 10.95% to 12.58% in the company, effective from December 18, 2019. In another update, Prudential plc and its subsidiary companies ceased to be a substantial holder in the company, effective from December 16, 2019.

On December 5, 2019, the company revised its FY20 guidance due to challenges pertaining to sourcing skilled operators for Maules Creek and impacts from dust events related to severe and ongoing drought conditions in North West NSW.

September’19 Quarter Key Highlights: The managed saleable coal production rose by 23% on pcp, to 4,909k tonnes, and the company’s managed total coal sales stood at 5,546k tonnes during the quarter, up by 14% y-o-y. Total equity coal sales for the quarter stood at 4.5 million tonnes, with equity own coal sales of 3.9 Mn tonnes, which remained in-line with the previous quarter.

Revised FY20 Guidance (Source: Company Reports)

Valuation Methodologies:

Method 1: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

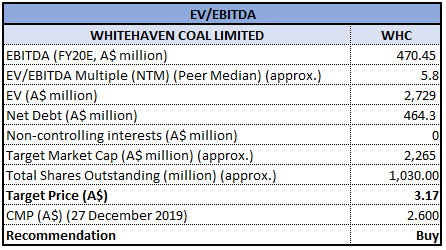

Method 2: EV/EBITDAMultiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock generated a negative YTD return of 36.02% and is currently trading towards its 52-week low of $2.490. Its gross margin, EBITDA margin, and net margin for FY19 stood at 54.6%, 59.1% and 21.2%, better than the industry median of 44.3%, 32.2%, and 15.3%, respectively, implying decent fundamentals of the company. ROE for FY19 stood at 15.1%, better than the industry median of 13.2%. The debt to equity ratio for FY19 stood at 0.12x, lower than the industry median of 0.24x. Considering the company’s September Quarter production data, updated FY20 production guidance, and current trading levels, we have valued the stock using relative valuation methods, i.e., PE and EV/EBITDA multiples approach and arrived at a lower double-digit growth (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.600, up 1.562% on December 27, 2019.

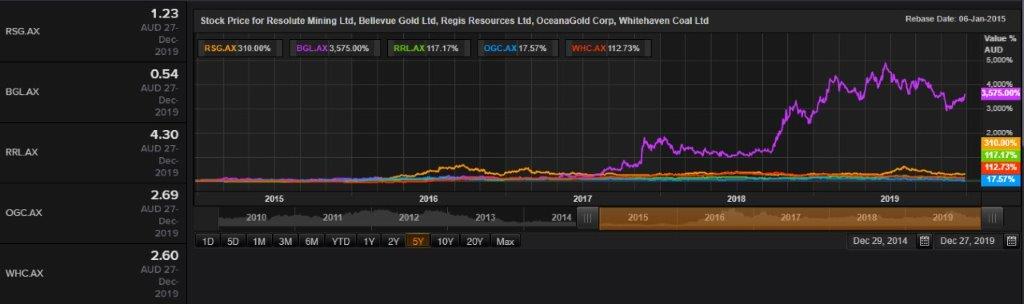

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...