.png)

Stocks’ Details

Amcor Plc

Decent Quarterly Performance: Amcor PLC (ASX: AMC) is involved in the development and production of rigid and flexible packaging for numerous food, beverage, pharmaceutical, medical device. The market capitalisation of the company stood at $21.68 Bn as on 15th June 2020. Recently, S&P Dow Jones Indices announced changes in the S&P/ASX indices, which will be effective from 22nd June 2020. As per the announcement, Amcor PLC will be removed from the S&P/ASX 20 Index on the effective date. During the quarter ended 31st March 2020, the company reported net sales amounting to US$3,141.0 million, reflecting a rise of 36.0% on pcp. Net income for the period went up by 61.2% to US$181.5 million. With respect to the Flexible segment, net sales, including intersegment sales stood at US$2,434.8 million, indicating a rise of 54.4%. Gross profit for the period stood at US$652.0 million with aa rise of 55.3%. The increase was primarily in the Flexibles reporting segment driven by the Bemis acquisition.

.png)

Key Financials (Source: Company Reports)

Improved Guidance: For FY20, the company has improved its estimated adjusted EPS constant currency growth in the range of 7%-10%. Cash flow before dividends is expected to be over US$1 billion.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: The Novel Coronavirus has presented a period of unprecedented uncertainty and challenge. The ultimate near-term impact of the pandemic on its business, including on its fiscal fourth quarter, would depend on (1) the extent and nature of any future disruptions throughout the supply chain, (2) the duration of social distancing measures and other government-imposed restrictions and (3) the nature and pace of macroeconomic recovery in key global economies.

Stock Recommendation: The company is optimistic that it is well-positioned to address the challenges of the COVID-19 pandemic. AMC’s business is almost entirely exposed to defensive end markets which have demonstrated the same resilience experienced through the past economic cycle. Net margin of the company stood at 5.7% in March 2020 quarter as compared to the industry median of 5.3%. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers such as Orora Ltd (ASX: ORA), Pro-Pac Packaging Ltd (ASX: PPG), Gage Roads Brewing Co Ltd(ASX: GRB). Therefore, in light of improved guidance, decent growth in net sales and improved net margin, we give a “Buy” recommendation on the stock at the current market price of $13.830 per share, up by 0.29% on 15th June 2020.

Boral Limited

Update on Litigation with Wagners: Boral Limited (ASX: BLD) is engaged in the manufacturing and supply of building and construction materials. The market capitalisation of the company stood at $4.27 billion as on 15th June 2020. Recently, the company has appointed Zlatko Todorcevski on the position of Chief Executive Officer, which will be effective from 1st July 2020. With respect to litigation with Wagners Holding Company Limited, the Supreme Court of Queensland via reserving the final orders have announced that the pricing notices filed by BLD on 1st March 2019 and 1st April 2019 are not effective and valid under the Cement Supply Agreement between the parties. In contrast, the Pricing Notice issued on 2nd October 2019 is valid.Moreover, the findings of the court provided some clarity for the parties moving forward around BLD’s ability to issue and rely on a Pricing Notice.

BLD has successfully completed a new US Private Placement note issue of US$200 million. In addition, the company has also successfully completed the execution of its new bilateral two-year bank loan facilities amounting to around A$365 million and completed its new bilateral loan facilities of US$740 million and maturing in June 2024. Due to volume and cost pressures associated with bushfires in Australia in January followed by COVID-19 impacts more broadly, revenues for the first four months of 2H FY20 witnessed a decline as compared to pcp.

.png)

Liquidity Profile (Source: Company Reports)

Suspension of Guidance: For FY20, the company has suspended its earnings guidance in light of the high level of uncertainty surrounding the spread, duration and impact of COVID-19 on the markets in which it operates.

Key Risk: The company has recently increased its bank loan facilities, and during 1H FY20 its debt to equity stood at 0.48x, reflecting a rise of 20.5%. The company is exposed to various industry and market risks, including structural and cyclical demand changes, macroeconomic and geopolitical conditions, and future resource supply constraints.

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

.png)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company is maintaining a strong liquidity position and a robust balance sheet. As at April 2020, the net debt of the company stood at A$2.6 billion up from A$2.3 billion as at Dec-2019 mainly due to the weakening of AUD/USD exchange rate from 0.7018 to 0.6526. The stock of BLD has provided returns of 27.94% and 6.10% in the last one month and three months, respectively. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). Thus, considering the strong balance sheet, robust liquidity position and returns in the past months, we give a “Buy” recommendation on the stock at the current market price of $3.540 per share, up by 1.724% on 15th June 2020.

Advance Nanotek Limited

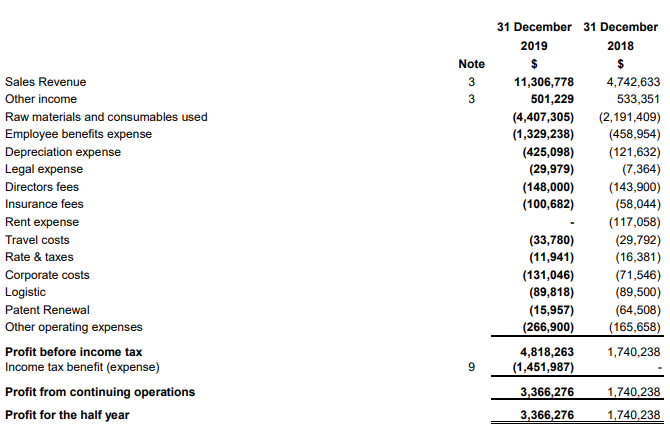

Completion of First Lab Trials: Advance Nanotek Limited (ASX: ANO) is involved in the development and manufacturing of advanced materials products. The market capitalisation of the company stood at $262.25 million as on 15th June 2020. As per the recent quarterly rebalance of S&P/ASX indices, the company has been added to All Ordinaries, which will be effective from 22nd June 2020. In another update, the company announced that it has successfully completed its first lab scale trials of product using its new lab scale high shear mixing equipment. The company would invest in new equipment and repurpose unutilised equipment from its Perth facility with the objective to commence full-scale production of products not currently being manufactured and sold by its end users, within the next 12 months. The below picture gives an overview of the income statement for 1H FY20.

Key Financials (Source: Company Reports)

Rise of 2.5x in FY20 Profit: As of now, the company expects that all of its products will be sold in Europe and the US. ANO forecast to produce up to 8,000 tubes per batch in order to allow the introduction of new products to Europe and the US. The company is likely to have a small positive impact on revenue in FY21. For FY20, it expects to have net profit before tax of around $8.4 million, reflecting a rise of 2.5x over FY19.

Key Risk: Previously, the company anticipated a modest negative effect on its sales target of $30 million for FY20 as the company was experiencing a short-term negative impact from the coronavirus on sales. ANO is mainly exposed to financial risk, including market risk, credit risk and liquidity risk.

Stock Recommendation: Gross margin and EBITDA margin of the company stood at 61.6% and 42.9% in 1H FY20, reflecting YoY growth of 7.0% and 10.5%. Current ratio of the company stood at 3.96x with YoY growth of 3.4%. This implies that the company has improved its position to address its short-term obligations. The stock of ANO has corrected 18.52% and 24.79% in the last one month and six months, respectively. The stock is currently inclined towards its 52-week low of $3.200, offering a decent opportunity to accumulate. Thus, considering improved liquidity position and key margins, decent outlook and key risks, we give a “Speculative Buy” recommendation on the stock at the current market price of $4.350 per share, down by 1.136% on 15th June 2020.

Incitec Pivot Limited

Decent performance in 1HFY20: Incitec Pivot Limited (ASX: IPL) is in the manufacturing and distribution of industrial explosives, industrial chemicals and fertilisers. The market capitalisation of the company stood at $3.73 billion as on 15th June 2020. The company has recently completed its share purchase plan and raised around A$57.5 million. Previously, the company has also completed A$600 million fully underwritten institutional placement. The company would the proceeds from placement to repay drawn balances of syndicated facilities, with any remaining amount held as cash on deposit. This capital raising supports the commitment to maintain a strong investment-grade credit rating profile.

During 1H FY20, the group revenue stood at $1,848 million, reflecting a rise of 6% as compared to pcp while its Earnings Before Interest and Tax (EBIT) amounted to $159 million with an increase of $41 million over pcp.

.png)

Key Metrics (Source: Company Reports)

Strategy for Growth: The company’s strategy revolves around improving shareholder value via profitable growth, underpinned by premium technology solutions for its customers and manufacturing excellence. IPL added that industrialisation, digitisation, urbanisation and population growth are generating demand for explosives and fertilisers.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: During 1HFY20, COVID-19 introduced new risks to recovery in commodity prices and global economic uncertainties. These risks might impact the customer demand in future.

Stock Recommendation: IPL is positioned in the most attractive explosives markets in the world and leading fertilisers distribution business in Eastern Australia. The company possesses a robust balance sheet with improved liquidity. Current ratio of the company stood at 0.91x, reflecting YoY growth of 56.3%. This implies that the company has enhanced its liquidity position to address its short-term obligations.We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers such as Orica Ltd (ASX: ORI), Nufarm Ltd (ASX: NUF), Aurizon Holdings Ltd (ASX: AZJ). Therefore, in light of improved liquidity position, increasing demand for explosives and fertilisers and recent capital raising, we give a “Buy” recommendation on the stock at the current market price of $1.885 per share, down by 3.333% on 15th June 2020.

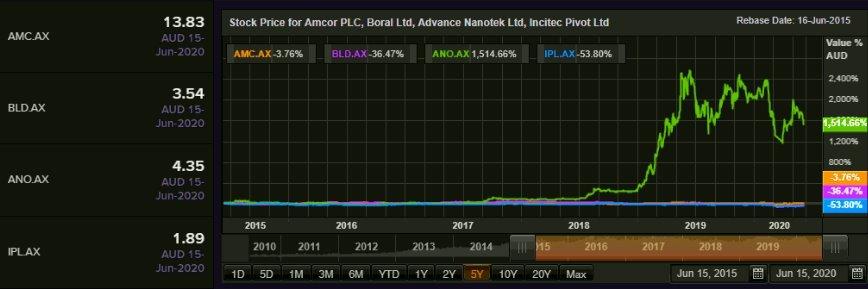

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...