Downer EDI Ltd

.png)

DOW Dividend Details

Maintained dividends despite performance pressure: Downer EDI Ltd (ASX: DOW) revenues fell by 1.2% year on year (yoy) to $3.5 billion in the six months ended on December 2015, as its major divisions were under pressure, with Transport Services’ revenue falling by 12.3% yoy to $802.9 million on the back of decrease in Government expenditure and extreme weather conditions at NSW and WA. But, the group’s technology and Communication Services’ revenue rose by 2.0% yoy to $249.9 million driven by enhanced contracts in Australia and New Zealand. Utilities Services revenue also surged by 83.7% yoy to $376.5 million due to power and gas projects contribution and better activity at the Ararat wind farm project in Victoria. However, mining revenue segment was under pressure with revenues falling by 5.2% yoy to $781.6 million due to reduced volumes and contract completions on the back of ongoing commodity prices pressure. Rail revenue declined by 1.0% to $420.1 million, due to 28.9% fall in core rail revenue. Consequently, the group’s EBIT plunged by 20.1% yoy to $113.2 million, impacted by write off of bid costs related to Capital Metro, while Net Profit after Tax (NPAT) fell by 23.9% to $72.1 million.

.png)

Financial performance (Source: Company Reports)

On the other hand, DOW maintained its interim dividend at 12.0 cents per share in the first half of 2016 in line with the prior corresponding period (pcp) despite the group’s performance pressure during the period. Moreover, the group has written off $13 million in pre-tax bid costs during the first half of 2016 as its ACTivate consortium was not fruitful for Capital Metro bid. DOW now forecasts an NPAT of over $180 million (down from the earlier stated $190 million) for the full year of 2016. Meanwhile, DOW corrected over 23.98% (as of February 17, 2016) in the last one year placing the stock at very cheaper valuations with a lower P/E and an outstanding dividend yield. We maintain our positive stance on the stock and issue a “BUY” recommendation at the current price of $3.27

DOW Daily Chart (Source: Thomson Reuters)

Cedar Woods Properties Ltd

.png)

CWP Dividend Details

Strategically acquired Brisbane Infill Site: Cedar Woods Properties Ltd (ASX: CWP) is strengthening its Queensland property via its $24.6 million acquisition of a 3.81 hectare infill site at Wooloowin, located in Brisbane’s inner north. This acquisition is expected to add the group’s earnings from 2018. Meanwhile, CWP is also enhancing its funds to position itself in the current challenging market conditions and stretched its three-year $135 million corporate finance facility by further year till November 2018. Even though its top line fell to $178.6 million in fiscal year of 2015 against $214.5 million in FY14, CWP enhanced its net profit after tax by 5.6% yoy to $42.6 million during the period.

.png)

NPAT and Gearing performance (Source: Company Reports)

During the first quarter of 2016, CWP’s pre sales rose to $184 million against $170 million in pcp. CWP estimates its FY16 to be in line with its FY15 NPAT at $42.6 million. The group is also trading at very attractive valuations with a cheaper P/E and has a solid dividend yield. Accordingly, we give a “BUY” recommendation on the stock at the current price of $4.01

.PNG)

CWP Daily Chart (Source: Thomson Reuters)

Contango Microcap Ltd

.png)

CTN Dividend Details

Delivered strong performance: Contango Microcap Ltd.’s (ASX: CTN) stock corrected about 2.11% (as of February 17, 2016) during this year to date. However, CTN has delivered strong performance for half year ended at December 2015, wherein the revenues rose to $17.45 million against a revenue loss of $3.037 million in pcp. Consequently CTN’s profit rose to $9.055 million during the period as compared to a loss of $4.088 million in pcp. Contango Microcap’s NTA of investments before tax reached $1.102 in January 2016 against $1.151 in December 2015.

.png)

Performance as compared to S&P/ASX Small Ords Accum (Source: Company Reports)

Meanwhile, Contango’s management is constantly seeking for firms with solid capital position and growth prospects so that these firms could be defensive from the volatile economic conditions. The group has also been a good dividend player with a strong dividend yield. We rate a “BUY” on CTN at the current price of $0.915

CTN Daily Chart (Source: Thomson Reuters)

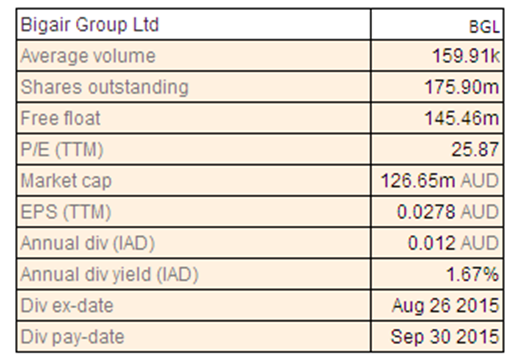

BigAir Group Ltd

BGL Dividend Details

Strengthening business via acquisitions and offerings: The shares of BigAir Group Ltd (ASX: BGL) plunged over 9.88% (as of February 17, 2016) during this year to date on investor’s concerns over the group’s potential performance coupled with the ongoing global financial markets turmoil. On the other hand, BGL was able to deliver a five year compound annual EBITDA growth of 43% to $18.9 million during fiscal year of 2015 and maintained their dividend policy by reporting a fully franked dividend of 1.2 cents per share. The group was also boosting its offerings by finishing two acquisitions - Oriel Technologies Pty Ltd and Integrated Data Labs Pty Ltd in fiscal year of 2015 as well as added Cloud Managed Services to its present data network offerings.

We believe that investors need to leverage the correction to enter BGL and accordingly issue a “BUY” recommendation at the current price of $0.75

BGL Daily Chart (Source: Thomson Reuters)

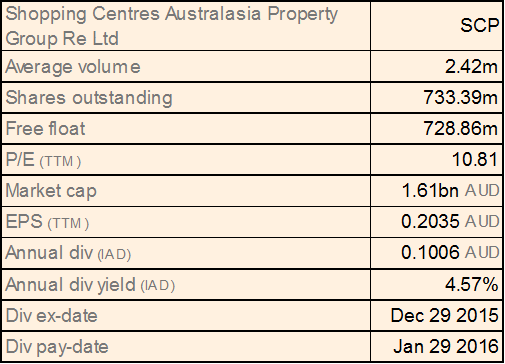

Shopping Centres Australasia Property Group Re Ltd

SCP Dividend Details

Bottom line pressure: Shopping Centres Australasia Property Group Re Ltd (ASX: SCP) generated a net property income increase by 10.9% on a year over year basis in the first half of 2016, driven by better Anchor rental income and Specialty rental income on the back of acquisitions. SCP’s fair value of investment properties fell by 18.8% during the period against pcp. The above decrease coupled with fall in fair value of derivatives and financial assets as well as unrealized foreign exchange losses during the period impacted its bottom line.

As a result, the group’s net profit after tax plunged 7.5% yoy to $90.8 million. We believe that the ongoing challenging market conditions coupled with concerns over SCP’s organic growth and ongoing fall in Australian dollar might impact the group’s performance in the coming period. The stock is currently trading close to its 52-week high price. Hence, we put an “Expensive” recommendation on the stock at the current price.

SCP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...