.png)

Stocks’ Details

Spark New Zealand Limited

Spark Finance Extends Standby Facility: Spark New Zealand Limited (ASX: SPK) provides telecommunication services and development and offers fibre network construction, internet services etc. As on 1 April 2020, the market capitalization of the company stood at $7.35 billion. The company has recently announced that Spark New Zealand Limited has extended the term of its NZ$200 million committed standby revolving credit facility by one year and will mature on 30 April 2023, with a commitment stepdown to NZ$167 million for the period from 1 May 2022 to 30 April 2023. SPK has also recommended Deloitte to be appointed as its new external auditor but is subject to approval at its AGM which is to be held on 6 November 2020.

Decent Increase in Revenue and EBITDAI: During 1H20, the company has delivered the strongest revenue growth in three years to NZ$1,824 million. This was mainly due to strong performance in mobile, with high-margin mobile service revenue, with an increase in market share to 40.1% and growth in security and service management. Strong revenue growth momentum and focus on execution and cost management resulted in a slight increase of 2.2% in EBITDAI to NZ$500 million.

.png)

1H20 Financial Highlights (Source: Thomson Reuters)

Future Expectations and Guidance: The company has provided guidance for FY20 and expects EBITDAI in between NZ$1.1 billion to NZ$1.12 billion and dividend to be around 25 cents per share. The company’s approach will continue to build on many of Spark’s existing strengths and is investing in the right capabilities to remain competitive into the future.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

.png)

EV/Sales Multiple Based Approach (Source: Thomson Reuters), *1NZD=0.97 AUD

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of SPK is inclined towards its 52-weeks’ high level of $4.720. During 1H20, net margin of the company witnessed an increase over the previous year and stood at 9.2%, up from 8.7% in 1H19. In the same time span, ROE of the company stood at 11.6%, higher than the industry median of 5.1%. Considering the trading levels, higher margins and decent outlook, we have valued the stock using EV/Sales valuation approach and have arrived at a target upside of higher single-digit (in percentage terms). For the said purposes, we have considered TPG Telecom Ltd (ASX: TPM), Vocus Group Ltd (ASX: VOC) etc. as peers. Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $4.210, up by 5.25% on 1 April 2020.

News Corporation

Sale of News America Marketing to Charlesbank Capital: News Corporation (ASX: NWS) is engaged in publishing of global newspaper and books, media and information services, integrated marketing services, digital real estate and education services, sports programming and pay-tv distribution in Australia. The company has recently announced that it has entered into an agreement to sell its News America Marketing business to Charlesbank Capital Partners for a cash consideration of $235 million. The company will also benefit from NAM’s future success through an option to retain up to 15% equity.

Quarterly Results: The company has recently released its results for the half-year ended 31 December 2019, wherein it saw growth at several news businesses and an increased profit contribution from Move, operator of realtor.com®. During the half-year, revenue of the company stood at US$4,819 million and reported a total EBITDA of US$728 million.

.png)

Interim Financial Highlights (Source: Company Reports)

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation

.png)

Price to Cash Flow Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months, 1USD=1.65 AUD

Stock Recommendation: As per ASX, the stock of NWS gave a negative return of 23.16% in the past one month and is trading close to its 52-weeks’ low level of $13.360. During 1H20, gross margin of the company witnessed an increase over the previous half and stood at 45.8%, up from 43.3% in 2H19. In the same time span, ROE of the company stood at 1% as compared to the industry median of 2.6%. Considering the trading levels, negative returns and margins and decline in revenues and EBITDA, we have valued the stock using the price to cash flow-based relative valuation approach and have arrived at an indicative downside of middle single-digit (in percentage terms). Hence, we recommend our investors to keep an eye on the stock and give a watch stance at the current market price of $14.70, up by 0.685% on 1 April 2020.

Hutchison Telecommunications (Australia) Limited

Decent Growth in EBITDA and Fixed Customers: Hutchison Telecommunications (Australia) Limited (ASX: HTA) provides telecommunication services under the Vodafone brand in Australia. As on 1 April 2020, the market capitalization of the company stood at $1.76 billion. The company has recently released its full-year results for the period ending 31 December 2019 wherein it reported an EBITDA growth of 6.9% to $589.4 million and an increase of 245.5% in fixed customers to 114k.

.png)

FY19 Financial and Operational Metrics (Source: Company Reports)

Regulatory Clearances – CFIUS and FCC: The company has recently announced that the key condition for the proposed merger between Vodafone Hutchison Australia Pty Ltd and TPG Telecom Limited has been satisfied and it has received required clearance from the Committee on Foreign Investment in the United States and the required consent from the United States Federal Communications Commission.

Growth Opportunities: The company expects intense market competition in the telecommunications market. It is focusing on reducing costs to manage its financial performance and will also continue its strategy of maintaining stability between keeping a sustainable business model, whilst delivering value to Australian customers.

Stock Recommendation: As per ASX, the stock of HTA gave a negative return of 10.34% in the past one month and is inclined towards its 52-weeks’ low level of $0.098. During FY19, current ratio of the company stood at 0.74x, up from 0.08x in FY18. Considering the trading levels, negative returns, regulatory clearance from FCC and modest outlook, we recommend a watch stance on the stock at the current market price of $0.130 on 1 April 2020.

Event Hospitality and Entertainment Ltd

Decline in Expenses and Growth in EBITDA: Event Hospitality and Entertainment Ltd (ASX: EVT) operates hotels and restaurants, ownership and operation of Thredbo Alpine Resort, ownership of cinema, hotel and other rental properties. As on 1 April 2020, the market capitalization of the company stood at $1.21 billion. The company has recently released its interim results for the period ending 31 December 2019, wherein it reported an increase of 6.1% in entertainment group revenue and a growth 4.4% in hotel group profit. The company also well managed its underlying costs with progress in business transformation initiatives and a decline in unallocated expenses by 5.8%.

.png)

1H20 Financial Performance (Source: Company Reports)

Future Expectations: It is challenging to provide guidance amidst the outbreak of COVID-19, but March trading in hotel indicates an impact of around $2 million to $3 million on monthly profit before interest and tax. The company is focusing on growth in existing business revenue and maximize asset performance.

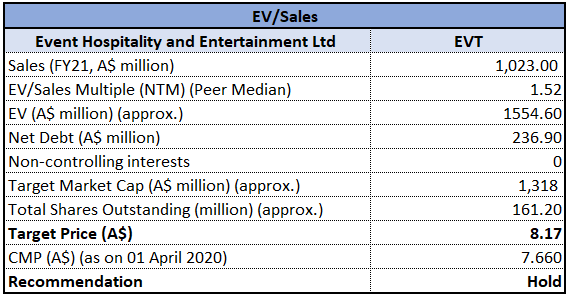

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of EVT is inclined towards its 52-weeks low level of $5.440. The company has a strong balance sheet underpinned by property assets and is focused on dealing with the impact of Coronavirus. During 1H20, net margin of the company improved over the previous half and stood at 11.3%, up from 8.7% in 2H19. In the same time span, ROE of the company went up to 5.2%, up from 3.7% in 2H19. Considering the trading levels, decent financial position and improvement in margins, we have valued the stock using EV/Sales valuation approach and have arrived at a target upside of higher single-digit (in percentage terms). For the said purposes, we have considered Village Roadshow Ltd (ASX: VRL), Ardent Leisure Group Ltd (ASX: ALG), etc. as peers. Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $7.660, up by 2.133% on 1 April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...