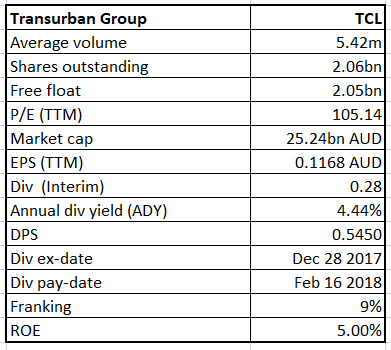

Transurban Group

TCL Details

Successfully completed the Institutional Entitlement Offer:Transurban Group’s (ASX: TCL) stock got a boost (up 4.2% on December 15, 2017) as the company successfully completed the Institutional Entitlement Offer of its $1.9 billion Entitlement Offer. The company has raised approximately $1.35 billion through the Institutional Entitlement Offer, and issue of approximately 118 million New Securities. Further, TCL will also complete the retail component of the Entitlement Offer in early February. TCL is raising fund through Entitlement Offer to contribute towards funding of the Transurban’s share ($4.0 billion) of the West Gate Tunnel Project (WGTP or the Project), and for general corporate purposes. The construction phase of the project has commenced, and is due to complete in 2022. Additionally, TCL has reaffirmed its distribution guidance of 56.0 cps for FY18, inclusive of the recently announced interim distribution of 28.0 cps for the six months ending 31 December 2017. Given TCL’s potential and infrastructure industry trends, we put a “Buy” recommendation on the stock at the current price of $12.80

.png)

TCL Daily chart (Source: Thomson Reuters)

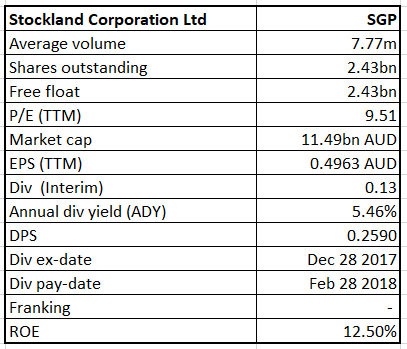

Stockland Corporation Ltd

SGP Details

'

Estimated distribution as per expectation: Stockland Corporation Ltd (ASX: SGP) has announced an estimated distribution for the six months to 31 December 2017 of 13.0 cents per Ordinary Stapled Security. This is as per SGP’s previous guidance that its full year distribution payment for FY18 is projected to be 26.5 cents per Ordinary Stapled Security. The Record Date for this is 29 December 2017 and the distribution payment will be made in February 2018. Meanwhile, it is worth noting that SGP’s retail, logistics and office segments account for 65% of earnings while remaining comes residential development with retirement living operations contributing to 7%. Growth in funds from operations per security and in distribution along with a positive outlook indicate a good tracking of the performance. We maintain a “Hold” recommendation on the stock at the current price of $4.69

.png)

SGP Daily chart (Source: Thomson Reuters)

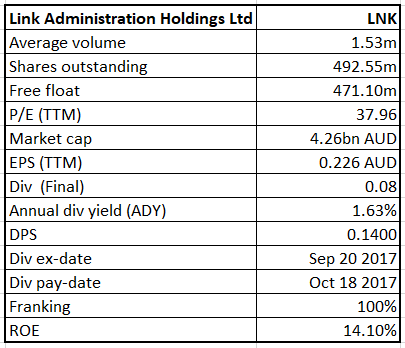

Link Administration Holdings Ltd

LNK Details

Completed the acquisition of Capita Asset Services:Administration services provider for the superannuation funds industry in Australia, Link Administration Holdings Ltd (ASX: LNK) has completed the £888 million acquisition of Capita Asset Services. Moreover, LNK in FY18, expects Fund Administration revenues to remain flat as the underlying organic growth drivers of contracted price escalations and member growth are offset by the full year impact of the Superpartners’ price discounts. The expected benefits from RBF, the recent client win, is expected to shift in the 2H of FY2018, which will again partially offset the expected loss of Kinetic in the June quarter of FY18. Meanwhile, LNK stock has risen 13.62% in three months as on December 14, 2017 and trades at a high level. While there may be some strategic benefits, we believe that the stock is “Expensive” at the current price of $8.59

.png)

LNK Daily chart (Source: Thomson Reuters)

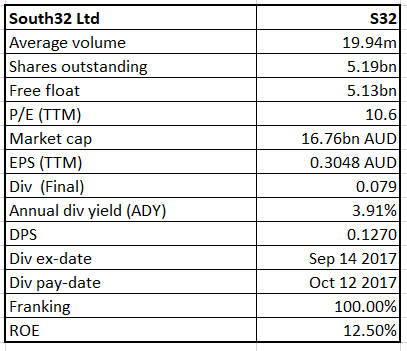

South 32 Ltd

S32 Details

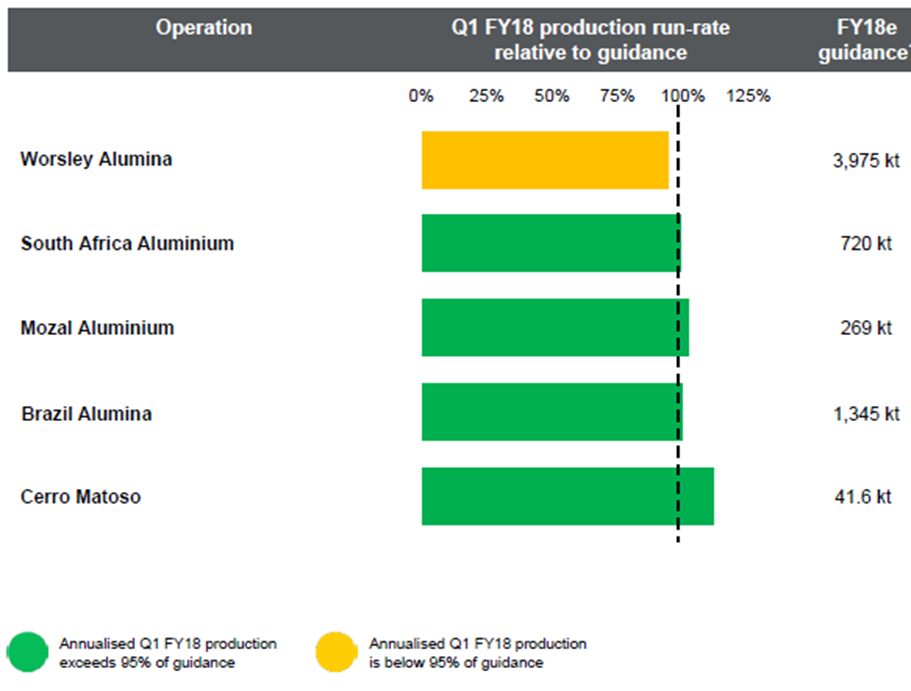

Reaffirmed prior FY18 production guidance:South32 Ltd (ASX: S32) has reaffirmed its prior FY18 production guidance for the operations and provided production and unit cost guidance for Illawarra Metallurgical Coal for the first time, while the company has restarted one longwall at the Appin colliery in October 2017. S32 has also confirmed that sustaining capital expenditure of US$470M is now expected in FY18 (compared to prior expectations of US$500M), with two thirds of the reduction associated with the deferral of underground development at Appin. Moreover, for Illawarra Metallurgical Coal in FY18, the saleable production is now expected to be 4.5Mt (3.35Mt metallurgical coal, 1.15Mt energy coal) at an operating unit cost of US$130/t2. However, the production will be weighted to the second half of FY18 due to the recent outage at the Appin colliery.

Unchanged Production Guidance (Source: Company Reports)

The company expects to have Appin colliery returning to its prior two longwall configuration in the December 2018 quarter, after which S32 has planned to ramp-up Illawarra Metallurgical Coal production safely and sustainably towards historical rates of more than 8Mtpa. Further, for Illawarra Metallurgical Coal, the sustaining capital expenditure is now expected to be US$120M in FY18 (previously US$150M). With more potential to be unveiled, we give a “Hold” recommendation on the stock at the current price of $3.22

.png)

S32 Daily chart (Source: Thomson Reuters)

AxsessToday Ltd

AXL Details

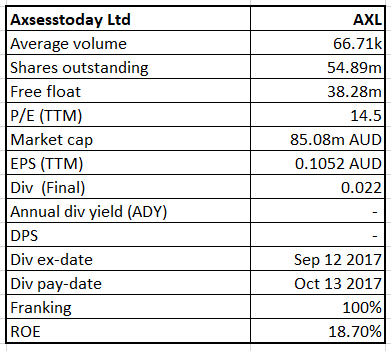

Share Purchase Plan:Equipment financier, AxsessToday Ltd (ASX: AXL) seems to be tracking well to deliver an FY18 NPAT of at least $6.5m, and finds support from expanded distribution network and product offering and IT systems related investment with a good capital accessibility through a healthy funding mix. The exposure to wide ranges of sectors including hospitality and transport, offer good opportunities. Recently, the group announced a Share Purchase Plan (SPP) in the month of October 2017, and offered eligible shareholders the opportunity to subscribe for new shares up to a maximum value of $15,000 at a share price of $1.50. For this, a total of approximately $2.05 million in applications was received from 165 shareholders and the level of applications exceeded the company’s target of $0.5 million. AXL has planned to increase the size of the SPP and to scale-back applications. Therefore, AXL has increased the amount raised to a total of approximately $1 million with 667,498 new shares issued. The scale-back was not applied to any applications for $5,000 or less, and applied at approximately 47.5% for all other eligible applications. Given the growth prospects, we put a “Speculative Buy” recommendation on the stock at the current price of $1.54

AXL Daily chart (Source: Thomson Reuters)

Boral Ltd

BLD Details

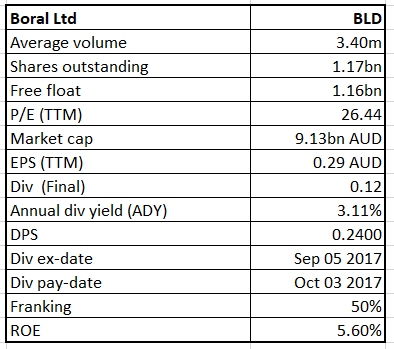

Outlook for FY18:Building supplies group, Boral Ltd (ASX: BLD) expects Boral Australia to witness an increase in energy costs at the upper end of $15-$20 million in FY18, while the Property earnings are expected to be at lower end of the range of $8m–$46m, skewed to the second half, with high single-digit EBIT growth. In FY18, USG Boral’s profit is expected to grow at a high single-digit growth rate, and Sheetrock might deliver price, volume and cost benefits across all markets with second half improvements expected from Indonesia and Thailand businesses, while softer activity is expected in Australian and Korean residential construction markets. Boral North America is expected to have significant growth in EBIT in FY18 from the full year contribution of Headwaters along with US$30–35m of year 1 synergies. Meridian Brick JV is expected to contribute an earnings uplift from market growth and synergies. There is an assumption for delivery of market growth projection of approximately 8% in housing starts (to approximately 1.29 million), approximately 5% increase in US infrastructure activity, approximately 12% growth in Non-residential and approximately 6% growth in Repair & Remodel. Overall, BLD is maintaining and strengthening the leading position in Australia at the back of position in the east coast where conditions are strong, and the quarry reinvestment leverages the ability to deliver major projects. Further, BLD is having transformational growth in the USA with the Headwaters acquisition and Meridian Brick JV. Meanwhile, BLD stock has risen 14.88% in three months as on December 14, 2017 and there is more momentum expected. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $7.65

.png)

BLD Daily chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...