.png)

Stocks’ Details

CSL Limited

Double-Digit Profit Growth in 1HFY19: CSL Limited (ASX: CSL) is engaged in research, development, manufacture and distribution of biopharmaceutical and allied products. As per a recent announcement, Anjana Narain was named as the Executive Vice President and General Manager of the company’s Seqirus business. The appointment came in after Gordon Naylor announced his retirement from the said position.

FY20 Transition to Own Distributor Model in China: The company recently provided an estimate of the ‘one-off’ financial effects of the planned transition to its own Good Supply Practice License in China in FY20. The financial impact will include lower reported albumin sales of approximately $340 million - $370 million, profit effect in line with historical CSL Behring margins and a more modest impact on cashflow from collection of outstanding receivables from existing distributors.

1HFY19 Highlights: During the first half, the company reported sales revenue amounting to $4,505 million, up 11% at constant currency. Earnings before interest and tax amounted to $1,553 million, representing constant currency growth of 6%. Reported net profit after tax stood at $1,161 million, up 10% at constant currency.

.png)

Group Financial Results (Source: Company Reports)

FY19 Guidance: The company expects FY19 net profit after tax to be around the upper end of the earlier guidance range of $1,880 million-$1,950 million at constant currency.

Stock Recommendation: The stock of the company generated returns of 6.43% and 15.29% over a period of 1 month and 3 months, respectively and ~25% on YTD. Currently, the stock is priced close to its 52-week high level of $226.450. During the first half, the company delivered double-digit profit growth with outstanding performance from its Immunoglobulin, Influneza Vaccines and Speciality Products franchises. The period was characterised by a solid financial result followed by a strong comparative period. Currently, the stock is trading at a price to earnings multiple of 40.550x. EV/EBITDA multiple at 25.7x is above to the industry median of -4.6x, indicating the overstretched valuation. Considering the expensive valuation and current trading levels, we are of the view that most of the developments are priced in at the current juncture. Hence, we give an “Expensive” recommendation on the stock at the current market price of $226.450, down 2.405% on 05 August 2019.

Sonic Healthcare Limited

Revised Earnings Guidance to Incorporate Aurora Acquisition: Sonic Healthcare Limited (ASX: SHL) is engaged in the provision of medical diagnostic services and provision of administrative services and facilities to medical practitioners. The company recently updated the exchange regarding the issue of 68,000 fully paid ordinary shares for the purpose of exercise of options. Out of this, 33,000 shares were issued at $27.34 per share on the exercise of options with an exercise price of $19.78 per option. 35,000 shares were issued on the exercise of options with an exercise price of $12.57 per option.

The company also updated that it has sold its shareholding in GLP Systems GmbH to Abbott. The sale of an 85% share in GLP is expected to generate an after-tax profit of around A$48 million. This will also return approximately A$130 million cash to the company. Through the cash, the company plans to repay its debt and aims for further laboratory acquisitions with the additional balance sheet capacity.

Financial Highlights: During the six months ended 31 December 2018, the company reported revenue amounting to A$2.9 billion, up 9% on pcp. Underlying EBITDA for the period stood at A$485 million, up 7% on pcp. Net profit for the period amounted to A$223 million, up 7% on pcp.

.png)

H1FY19 Financial Summary (Source: Company Reports)

FY19 Guidance: The company upgraded full-year earnings guidance to 6% - 8% underlying EBITDA growth at constant currency. Earlier, the company had provided a guidance range of 3% - 5%, which was revised to incorporate Aurora Diagnostics acquisition.

Stock Recommendation: Over a period of 6 months, the stock generated returns of 22.52%. Currently, the stock is priced close to its 52-week high level of $28.660. FY19 first half was characterised by strong earnings growth in the US, Swiss, and Australian laboratory operations. The company also expanded its US business through the acquisition of Aurora Diagnostics. The company has an EV/EBITDA multiple of 14.4x, which is higher than the industry median of 9.4x. Price/Earnings multiple for the company stands at 25.67x as compared to the industry median of 15.0x. We believe that most of the positive factors are already price in, and the stock is currently trading at stretched valuation. Hence, considering the aforesaid facts and current trading levels, we give an “Expensive” recommendation on the stock at the current market price of $27.990, down 1.235% on 05 August 2019, and suggesting that investors should wait for few more catalysts that may drive the stock higher.

National Australia Bank Limited

Decent 1H19 Performance Amidst Challenging Environment: National Australia Bank Limited (ASX: NAB) is engaged in the provision of banking services. The bank recently updated that Geraldine Celia MCBRIDE acquired 1,743 ordinary shares for a total consideration of $49,239.75. In another recent update, the bank also notified regarding the issue of US$1,500,000,000 3.933% subordinated notes, pursuant to its US$100,000,000,000 global medium-term note programme.

Appointment of Key Personnel: In the month of July, the bank appointed Susan Ferrier as Group Chief People Officer and Ross McEwan as the Chief Executive Officer.

1HFY19 Highlights: During the period, the bank reported cash earnings amounting to $2,954 million, up 7.1% on the prior corresponding period. Diluted cash EPS was reported at 102.5 cps, up 3.7% on pcp. The bank generated a statutory profit amounting to $2,694 million, up 4.3% on pcp.

.png)

Key Financial Metrics (Source: Company Reports)

Outlook: Despite the challenges faced in the first half, the bank expects underlying profit growth to be driven by productivity benefits. The bank also has the potential to grow the dividend in the medium term with increased flexibility to accommodate earnings volatility and regulatory changes.

Stock Recommendation: The stock generated returns of 7.63% and 10.93% over a period of 1 month and 3 months, respectively. During the first half, the bank reported an increase of 19 basis points in Common Equity Tier-1 ratio, at 10.4%. The period also saw an increase of 7.1% in cash earnings and 16.2% in the dividend paid. Despite the challenging operating environment, the bank witnessed an H-o-H revenue growth of 0.9%. Hence, considering the aforesaid factors, we give a “Hold” recommendation on the stock at the current market price of $28.150, down 1.263% on 05 August 2019.

WAM Capital Limited

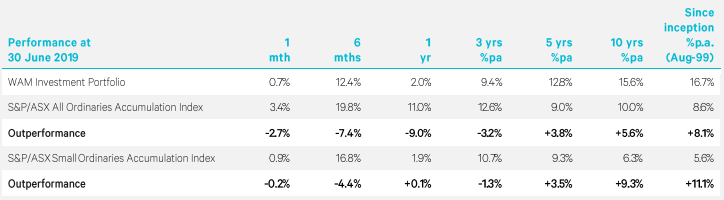

Portfolio Performance Driven by Mining Companies: WAM Capital Limited (ASX: WAM) is primarily engaged in investments in listed companies. The company recently updated that Chris Stott resigned from the position of Director on the Board.

Investment Update: In the latest investment update for June 2019, the company reported an increase of 0.7% in its investment portfolio for 1-month. Over a period of 6 months, the portfolio witnessed a rise of 12.4%. Gross assets for the month were reported at $1,324.7 million as compared to gross assets of $1,318.1 million in May 2019. The period reported pre-tax net tangible assets of $1.84 and a fully franked dividend yield of 7.7%.

Portfolio Performance (Source: Company Reports)

Portfolio Update: During the month, the company witnessed an increase of 6.1% in its holding in Codan Limited (ASX: CDA), a communication, metal detection and mining technology manufacturer in Adelaide. CDA is expected to maintain its momentum in earnings generated from broadening sales products, new products and market-leading intellectual property. Another key contributor to the portfolio performance was Ausdrill Limited (ASX: ASL), a mining services company with operations across India, UK, Africa and Australia.

Stock Recommendation: The stock of the company generated returns of 4.33% and 5.85% over a period of 1 month and 3 months, respectively. As per the investment update for June 2019, the company reported an increase of 0.7% over 1 month as compared to 0.1% in May 2019. The portfolio performance for the month was driven by the company’s investment in Codan Limited and Ausdrill Limited. Furthermore, the company is expected to benefit from the expected earnings growth from Codan Limited and the recent mining contract signed by Ausdrill Limited. Both the businesses will add to the portfolio performance with their significant revenue and earnings potential. Hence, considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $2.120, down 2.304% on 05 August 2019.

Credible Labs Inc.

Enters into Merger Agreement with Fox Corporation:Credible Labs Inc. (ASX: CRD) is engaged in providing an online marketplace which permits the users to obtain financial product offerings from FIs (financial institutions). Formed in November 2012 in the USA, CRD was previously named as Stampede Labs Inc. Later, the company was renamed as Credible Labs Inc. in December 2013.

The company recently announced that it has entered into a definitive merger agreement to be acquired by a subsidiary of Fox Corporation (Fox). As per the agreement, the shareholders will receive A$2.21 cash per CDI. Under the agreement, pursuant to certain conditions, the founder and CEO (Mr. Stephen Dash) will exchange shares equal to 33.33% of CRD’s outstanding common stock into newly created Fox subsidiary. The founder will also be entitled to A$55.25 per share of common stock in CRD for ~1 million shares (net of exercise of Mr. Dash’s outstanding options), being the maximum number of shares of common stock that Mr. Dash is permitted to sell. The transaction is subject to a number of customary closing conditions, including regulatory and shareholder approvals.

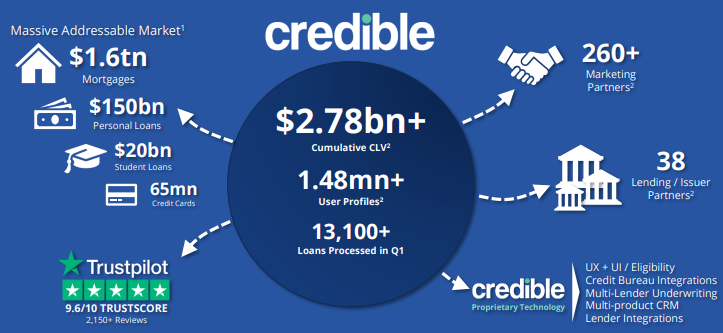

Highlights of Quarter Ended 30 June 2019: During the quarter, the company reported customer lifetime value (CLV) amounting to US$405 million, up 115% on the prior corresponding period CLV of US$188 million. Unaudited revenue for H1FY19 amounted to US$19.7 million, up 124% in pcp revenue of US$8.8 million. Gross profit for the period amounted to US$6.0 million, up 231% on the prior corresponding period profit of US$1.8 million.

As per a presentation released in April 2019, the company had a cumulative CLV of over $2.78 billion.

Stock Recommendation: The stock of the company generated returns of 49.28% and 168.40% over a period of 3 months and 6 months, respectively. The company’s originations more than doubled in the first half as compared to pcp accompanied by an expansion in gross margins and gross profit growth of over 230%. Furthermore, the company maintained a strong cash position and cash-like resources position of US$24.3 million at the end of the quarter. Currently, the stock is trading close to its 52 weeks high level of $2.230, which increases the probability for a correction in the near term. Hence, we have a watch view on the stock at the current market price of $2.190, up 6.311% on 05 August 2019 and suggesting that investor should wait for better entry levels.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...