Stocks’ Details

BHP Billiton Limited

Strong ROE’s and improving leverage position: BHP Billiton Limited (ASX: BHP) have announced as on January 12, 2019, that it will distribute a special dividend on its ordinary fully paid shares of USD 1.02 per share. These distributions would be fully franked and will be paid on the 30th January 2019. The record date for determining the eligibility of distribution was 11 January 2019.

It is noteworthy here that the proceeds of this distribution have come from the net proceeds derived from the sale of its Onshore US assets.

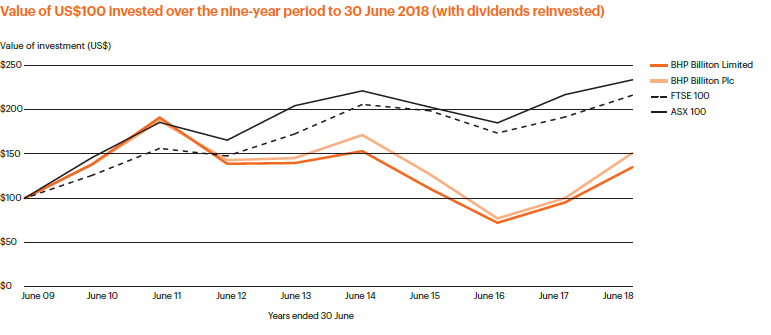

BHP’s cost optimization and unit costs (Source: Company Reports)

On the financial metrics front, the company has provided a ROE of 15.90% while the mining industry has a median ROE of 11.50%, which means that the company is more efficiently utilizing the shareholders’ funds. Moreover, the company has a strong balance sheet which is evident from the reducing YoY Debt-to-equity ratio which signifies that the firm has been able to optimize its debt profile over the year.

Meanwhile, the stock price has risen by 4.01% over the past three months as on 18 January 2019 and is trading close to 52-week higher level. Hence considering the robust ROE’s & constantly improving debt profile, we maintain our “Hold” recommendation on the stock at the current market price of $33.11.

Woodside Petroleum Limited

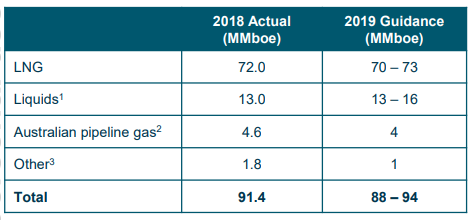

Planed turnovers for FY19:Woodside Petroleum Limited (ASX: WPL), based in Perth, Australia, is engaged in the exploration and production of oil and gas. The company has completed the construction of Wheatstone LNG gas plant with first domestic gas production expected in 1Q19. As per its 2019 production guidance, it is expected to produce 88-94 MMboe gas. The company has planned major turnarounds for Pluto LNG, Goodwyn Project, and integrated NWS Project in April-May 2019, July 2019, and September 2019 respectively.

FY19 gas production guidance (Source: Company Reports)

Over the past few years, the margins of the company have improved and are reported above the industry median.It reported an EBITDA margin and Net margin of 71.4% and 24.8% respectively in 1H18 as compared to the industry median of 33.9% and 10.4% respectively. The company reported a higher than the industry dividend yield (Trailing 12 months) of 5.6% as compared to the industry median of 3.0% showing that the company is generating more income for its shareholders.

Over the past 1 month, the stock has been in an uptrend and is expected to rise moreand has generated a positive return of 10.21%. It is currently trading at $33.890. With the planned turnarounds in FY19, better FY19 production guidance, higher dividend yield and the uptrend seen through the chart, we, therefore, maintain our ‘buy’ recommendation on the stock at the current market price of $33.890.

Aristocrat Leisure Limited

Sale of Video Lottery Terminal to begin in 2019:Aristocrat Leisure Limited (ASX: ALL), based in Sydney, Australia, is a leading gaming solution provider and gambling machine manufacturer. The company has launched Video Lottery Terminal (VLT) in 2018 and will begin its commercial sale in 2019.

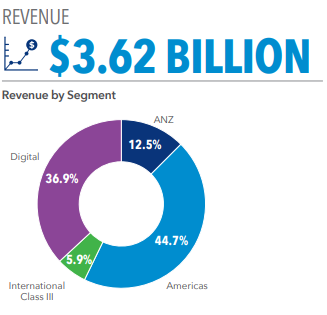

Revenue Breakup for FY18 (Source: Company Reports)

From FY13 to FY18, the margins of the company have improved and are reported above the industry median.It reported an EBITDA margin and Net margin of 37.2% and 15.3% respectively in FY18 as compared to the industry median of 21.0% and 10.5% respectively. Further, the company is generating better returns for its shareholders than its peers as it reported a ROE of 35.3% above the industry median of 13.0%.

During the past three months, the stock has generated a negative yield of 20.45% and is trading close to lower level. Today, the stock was up by 0.127% as compared to the previous close, currently trading at the price of level $23.560. The Relative Strength Index is seen in a negative position with the price moving towards the upper band of the Bollinger band. With the improving and better than industry margins, and the sale of VLT to begin in 2019, we have a wait and watch stance on the stock at the current market price of $23.560, and we suggest to investors that they should wait for a few more trading sessions to get the better entry levels.

Magellan Financial Group Limited

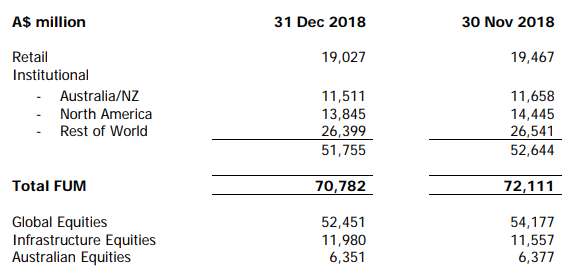

Dividend payment in January 2019:Magellan Financial Group Limited (ASX: MFG) is an Australian financial company engaged in generating returns for its clients by investing in various global equities and global listed infrastructure companies. As per the latest updates of December 2018, the total FUM was reported at $70.782 billion with a net inflow of $41 million including the net retail inflow of $90 million, and net institutional inflows of $49 million. The company is expected to pay ~$54 million as distribution (net of reinvestment) in January 2019 and the adjustment will reflect in February month announcement in relation to January 2019 FUM update.

Funds Under Management (Source: Company Reports)

Over the past few years, the margins of the company have improved and are reported above the industry median.It reported an EBITDA margin and Net margin of 78.0% and 47.0% respectively in FY18 as compared to the industry median of 62.1% and 30.4% respectively. Further, the company is generating better returns for its shareholders than its peers as it reported a ROE of 39.7% above the industry median of 10.0%.

During the past six months, the stock has generated a positive yield of 12.46% and is currently trading at the price of level $27.970. The Relative Strength Index is seen in a negative position with the price touching the upper band of the Bollinger band. With the improving and better than industry margins and the distribution of dividends in January 2019, we maintain our ‘hold’ position on the stock at the current market price of $27.970.

Australia and New Zealand Banking Group Limited

Royal Commission final report due in February 2019: Australia and New Zealand Banking Group Limited (ASX: ANZ) provides various banking and financial products and services.The bank has planned to demerge IOOF Holdings Limited, Zurich Financial Services Australia, Retail, Commercial and SME banking business in PNG region, and 55% stake in Cambodia JV ANZ Royal Bank in FY19.

.png)

FY18 Group Performance (Source: Company Reports)

During FY18, the bank reported a net interest margin of 1.87% which was slightly below the industry median of 1.94%. The efficiency ratio reported at 50.0% was also slightly below the industry median of 52.0% and has declined by 3.6% over the past five years. However, the Tier 1 Risk-Adjusted Capital Ratio was reported at 13.40% which has improved by 2.7% over the past 5-years and is above the industry median of 11.13% showing that the bank's financial health is improving.

On the valuation front, the bank reported a higher P/BV multiple of 1.3x as compared to the industry median of 1.1x indicating that the bank is earning a good return on the assets.Various hearings by the Royal Commission has led the overall banking industry to fall. Over the past one month, the stock has generated a positive yield of 10.05% and is currently trading at the price of level $26.070. With theimproving and better than industry margins, higher than industry P/BV multiple, and Demerger plans for FY19, we maintain our ‘Buy’ recommendation on the stock at the current market price of $26.070.

.PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...