.png)

Stocks’ Details

Clinuvel Pharmaceuticals Limited

Revenues Soared 11% Year Over Year: Clinuvel Pharmaceuticals Limited (ASX: CUV) is involved in the development of a photoprotective drug for the treatment of a wide range of severe skin diseases due to the exposure to light and harmful UV radiation. As on 3 March 2020, the market capitalisation of the company stood at ~$844.92 million. Recently, the company received a confirmation from the US Food and Drug Administration (FDA) for a meeting on April 29, 2020, relating to North American development program for SCENESSE® for the treatment of vitiligo.

CUV’s SCENESSE Drug Unaffected by Coronavirus Impact: On 2 March 2020, the company addressed several public enquiries, to assure that CUV’s business operations (drug substance in SCENESSE) within the European Economic region or the US were unaffected by the coronavirus outbreak.

1HFY20 Financial Highlights: The company has recently released its half-year results, wherein it reported a healthy balance sheet with no debt. During 1H20, revenue of the company went up by 11% to $9.971 million and reported an 8th consecutive half-year with net profit, which came in at $1.059 million.

.png)

1H20 Key Financial Highlights (Source: Company Reports)

Other Recent Updates: The company recently stated that it is investing in VALLAURIX R&D facilities for further expansion in Singapore. The new facility is expected to open on July 1, 2020, which is supported by The Singapore Economic Development Board (EDB) with up to A$547,000 for over 3 years. The company is adding new, highly skilled local personnel to its existing team to aid the progress of its product pipeline.

Valuation Methodology:P/BV Multiple Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of CUV is trading close to its 52-weeks’ low level of $15.91, proffering a decent opportunity for accumulation. During 1HFY20, quick ratio and current ratio of the company stood at 14.9x and 15.38x, respectively, higher than the industry median of 4.7x and 4.95x, respectively. We have valued the stock using Price to Book Value based relative valuation method and have arrived at a target price offering an upside of lower double-digit (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $18.19, up by 6.374% on 3 March 2020, on the back of recent developments with respect to its key product SCENESSE.

Pro Medicus Limited

Revenues up 15.7% Year Over Year in 1HFY20: Pro Medicus Limited (ASX: PME) is involved in the development and supply of software and IT solutions to the Public and Private Health sectors. As on 3 March 2020, the market capitalisation of the company stood at ~$2.15 billion.

1HFY20 Financial Highlights: During the period ended 31 December 2019, revenue of the company came in at $29.3 million, up 15.7% year over year. Net profit after tax witnessed a growth of 32.7% to $12.1 million.In the same time span, cash from operations grew strongly to $16.1 million, as compared to $6.4 million as at 31st December 2018. The company also reported a strong and stable balance sheet with no debt. The board of directors declared a fully franked interim dividend of 6 cents per share, with a payment date of 20 March 2020.

.png)

1HFY20 Financial Highlights (Source: Company Reports)

Stock Recommendation: The company is anticipating continuous growth from Partners Health, Duke Health, and existing clients. PME also remains on track to focus on growth strategies through new product offerings and extension in geographical markets. In 1HFY20, the company reported EBITDA margin of 63.5% as compared to the prior corresponding period margin of 62.4%. Net margin stood at 41% as compared to 35.7% reported in pcp. As per ASX, the stock of PME is trading at the lower band of its 52-week trading range of $14.447 and $38.39, offering decent opportunity for accumulation. Considering the above factors, we recommend a “Buy” rating on the stock at the current market price of $20.72, up by 0.242% on 3 March 2020.

Australian Pharmaceutical Industries Limited

Healthy Balance Sheet & Higher Revenues are Key Catalysts: Australian Pharmaceutical Industries Limited (ASX: API) is a leading seller, distributor & manufacturer in both the Pharmacy and Grocery channels, which offers allied products and services to retailers and manufacturers. Recently, API stated that one of its directors, named Richard Craig Vincent, has acquired 495,711 performance rights under the Long-Term Incentive Plan 2019 - 2022.

FY19 Financial Highlights for the Period ended 31st August 2019: During FY19, the company’s revenues went up 4.1% on y-o-y basis to ~$4 billion. The company delivered robust bottom-line growth with NPAT amounting to $56.6 million, an increase of 17.4% year over year. During the period, the company’s growth assets continued to perform well with 0.7% growth in its Priceline like-for-like sales. Rise in market share and positive impact from Priceline Pharmacy, consumer brands and Clear Skincare businesses were key positives in FY19. Further, robust result from the pharmaceutical wholesaling business also adds to the positive.

.png)

FY19 Financial Highlights (Source: Company Reports)

What to Expect: For FY20, the company is expected to deliver growth by focusing on leveraging its organisational, strategic and physical assets across Australia and New Zealand. Further, the company expects a robust working capital management on the back of a solid balance sheet.

Valuation Methodology:Price to Cash Flow Based Valuation

.png)

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of API is quoting at $1.18 with a market capitalisation of ~$573.94m. The stock is trading at the lower band of its 52-week trading range of $1.13 to $1.57. The stock has generated negative returns of ~11% in the last six-months. The company has a PE multiple of 10.4x, with an annual dividend yield of 6.65%. Considering the current trading levels and business prospects, we have valued the stock using Price to Cash Flow based relative valuation method. For the purpose, we have taken peers like Resmed Inc (ASX: RMD), Mayne Pharma Group Ltd (ASX: MYX) and Sonic Healthcare Ltd (ASX: SHL) and arrived at a target price of lower-double digit upside (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $1.18 per share, up 1.288% on 3 March 2020.

Paragon Care Limited

Sneak Peek in PGC’s H1FY20 Financial Highlights for the Period ended 31 December 2019: Paragon Care Limited (ASX: PGC) is involved in providing end to end healthcare solutions, which incorporates equipment and service solutions for acute, aged and primary care. PGC announced its half-yearly market update, wherein the company reported revenue at $120.7 million, up from $119.4 million reported in H1FY19. Gross margin for the period stood at 38%, flat year over year. The company reported normalised EBITDA at ~$12 million. The company reported a cash balance of ~$18 million as on 31st December 2019.

.png)

1HFY20 Financial Highlights (Source: Company Reports)

What to Expect: The company remained focused on increasing the market share and to become the leading supplier of New Zealand and Australia’s healthcare equipment as well as services. In order to achieve this, the company plans to undertake organic and inorganic methods for growth. In addition, the company is also planning to undertake certain acquisitions to expand its product and services as well as its geographic reach.

Stock Recommendation: The stock of PGC is trading at $0.235 with a market capitalization of $81.09 million. The stock made a 52-week low and high of $0.19 to $0.52, respectively, and is currently trading at the lower band of its 52-week trading range. The stock has delivered negative returns of ~40% in the last six months, with an annual dividend yield of 4.58%. The stock is available at an Enterprise Value to Sales multiple of 0.6x on trailing twelve months (TTM) basis as compared to the industry median (Healthcare Equipment & Supplies) of 7.2x. Considering the recent price correction, current trading levels and operational performance, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.235, down 2.083% as on 03 March 2020.

Estia Health Limited

EHE Achieved 93.7% in its Average Occupancy in 1HFY20:Estia Health Limited (ASX: EHE) is involved in providing services in residential aged care homes in Australia. As on 3 March 2020, the market capitalisation of the company stood at ~$506.51 million. Recently, the company stated that Perpetual Limited and its related bodies corporate, a substantial holder of the company, has increased its voting power from 11.02% to 12.18%. In another update, the company announced that it will distribute a dividend of $0.054per shareon March 27, 2020.

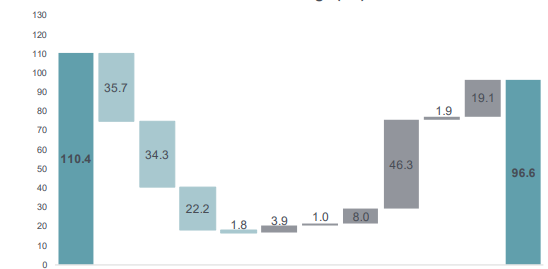

H1FY20 Financial Highlights for the Period ended 31 December 2019: The company has recently released its interim results, wherein the company achieved 93.7% growth in average occupancy in mature homes. EBITDA on mature homes stood at $40.9 million, and NPAT of the company was $14.3 million. EHE is accelerating its significant refurbishment program with a total of 42 homes and is qualifying for the higher accommodation supplement with additional eight homes to be completed in 2H20. During the period, the company’s net RAD inflows stood at $22.2 million, with $46.3 million capital investment in new homes and development of existing homes. Net debt at the end of the period stood at $96.6 million, with $211.0 million undrawn facilities.

Net Debt Position (Source: Company Reports)

Guidance: EHE has provided guidance for FY20 and expects EBITDA to be in the range of $78 million to $82 million. The company also expects capital investment to be in the ambit of $58 million to $64 million in 2HFY20 and is targeting bank debt gearing in between 1.5x-1.9x EBITDA.

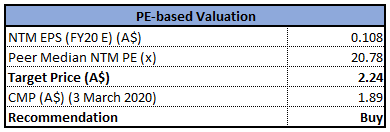

Valuation Methodology:Price to Earnings Based Valuation

Price to Earnings Multiple Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of EHE is trading very close to its 52-weeks low level of $1.85, proffering a decent opportunity for accumulation. During 1H20, EBITDA margin of the company stood at 20.6%, higher than the industry median of 9%. In the same time span, net margin of the company was 4.5% as compared to the industry median of 3.4%. The company has a P/E multiple of 14.65x, with an annual dividend yield of 6.8%. Considering the trading levels, higher EBITDA and net margin and decent outlook, we have valued the stock using price to earnings multiple based relative valuation method and arrived at a target price of lower double-digit upside (in percentage terms). For the purpose, we have taken peers like Resmed Inc (ASX: RMD), Regis Healthcare Ltd (ASX: REG), Japara Healthcare Ltd (ASX: JHC), to name few. Hence, we recommend a “Buy” rating on the stock at the current market price of $1.89, down by 2.577% on 3 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...