Xero Limited

.png)

XRO Details

Announcement of Annual Meeting and Proxy Forms: Xero Limited (ASX: XRO) has announced to invite shareholders to attend the Annual General Meeting (AGM) which will be held on August 16, 2018 at Level 3, Establishment, 252 George Street, Sydney, NSW, Australia and asked to vote undirected proxies in favour of each item of the business. These proxies are: fixing the remuneration of the Auditor, election of Dale Murray, Rod Drury, Craig Winkler, Graham Smith as a Director to the Board, approval of the Issue of shares to Lee Hatton and Bill Veghte, and adoption of new Constitution. On the financial front, the group improved operating and investing cash flow margins from -71% to -9%, respectively during FY15-18 and its revenue grew at a CAGR of 49% over the same period. Moreover, the total lifetime value of Xero subscribers at 31 March 2018 was recorded at $3.2 Bn, representing about 45% rise in FY18 as compared to the last financial year. XRO’s ROE as at 2018 was reported at -12.5% against -26.7% as at 2017; and an account receivable turnover ratio at 2018 was 15.7% and as at 2017, the same was 12.4%.

.png)

Improving Cash Outflow as % of Revenue (Source: Company Reports)

On the other hand, the group informed the market that the Chief Operating and Financial Officer, Mr. Sankar Narayan will leave the company at the end of December 2018 to pursue other opportunities. In turn, the company will be appointing its Chief Accounting Officer, Kirsty Godfrey-Billy as a Chief Financial Officer effective October 01, 2018. Meanwhile, the stock was up by 48.54 per cent in the last six months, and by 2.09 per cent in the last one week (as at July 17, 2018). Based on its improving financials and new product launches such as Xero HQ App Suite, Xero HQ Ask and Xero Discuss, we maintain our “Hold” recommendation on the stock at the current market price of $ 45.45, considering decent outlook ahead.

.png)

XRO Daily Chart (Source: Thomson Reuters)

NetComm Wireless Limited

.png)

NTC Details

Turnaround in Profitability: NetComm Wireless Limited (ASX: NTC) is a small cap company with the market capitalization of circa $ 163.89 Mn (as at July 18, 2018). It has a decent outlook ahead at the back of tremendous opportunity for Fixed Wireless, Distribution Point Units (DPUs) and M2M business in Australia, North America, and Europe. For that, the group is well placed into the market to capitalize on these opportunities based on the demonstrable real-world experience with Tier 1 customers and its bespoke solution methodology i.e., Listen-Innovate-Solve approach. During the first half of the year, the group posted strong performance at the back of execution of its key projects such as an expansion of M2M business and delivered the initial order of fixed wireless units to AT&T in the US for its rural broadband project. Moreover, the group has recently announced that it will increase the roll-out of its fibre-to-the-curb (FTTC) footprint by 440,000 additional homes, bringing the total rollout plan to around 1.5 million homes by 2020 – representing the positive picture in terms of receiving further orders over the coming years. In 1HFY18, sales and net profit grew by 88.6% and 317.2%, respectively as compared to the prior corresponding period. EBIT margin turned around to be positive and recorded 3.8% during the same period. The company can generate profit in years to come at the back of several developments and initiatives such as contract with Bell Canada, expansion of its nbn fixed wireless activation and coverage, focus on increased partner base at a global level, etc.

.png)

Strong EBITDA Increase Follows Strategic Investment (Source: Company Reports)

As of now, we maintain our “Buy” recommendation on the stock at the current market price of $ 1.110 (down by 0.893% on July 18, 2018), considering organic and inorganic growth expected to push profitability ahead.

.png)

NTC Daily Chart (Source: Thomson Reuters)

Nearmap Ltd

.png)

NEA Details

Enhanced Group ACV Portfolio: Nearmap Ltd.’s (ASX: NEA) stock climbed up 3.497 per cent on July 18, 2018 as the group exceeded its guidance which was provided at the time of the 1HFY18. According to the FY18 preliminary report, closing group annualised contract value (ACV) portfolio grew by 41% in FY18 and amounted to $66.2 Mn against previous year ($ 47 Mn), led by portfolio expansion in both Australia and the United States. During the period, the group’ US portfolio more than doubled for the first time in Nearmap’s history, marking 143 % growth on year on year basis. Given the expanding global subscriptions portfolio, and group average revenue per subscription (ARPS) expected to increase during the year, the group expects to grow further while delivering higher value products. The group’s cash reserve was slightly down and recorded $17.5 Mn as at June 30, 2018 from $ 20.6 Mn as at December 2017 due to strategic investment in sales and marketing capability and expanded HyperCamera 2 capture program. Following this, the group reduced cash investment in the second half of the year. We expect that the company will continue to drive top-line growth at the back of disciplined cost management with focussed investment capabilities.

.png)

Nearmap Group ACV Portfolio (Source: Company Reports)

On the other hand, Ms. Sue Klose completed her role as an Interim Chief Marketing Officer on July 05, 2018 and was back to her previous role as a Non- Executive director of the company, effective from July 06, 2018. However, the group is still looking for a full-time appointment and this is expected to be announced shortly. Meanwhile, the share price has rallied over 111.85 percent in the past six months and is trading at the higher level. Hence, we give a “Hold” recommendation on the stock at the current market price of $ 1.480, as we remain optimistic about NEA to continue its growth momentum in the upcoming period.

.png)

NEA Daily Chart (Source: Thomson Reuters)

Afterpay Touch Group Limited

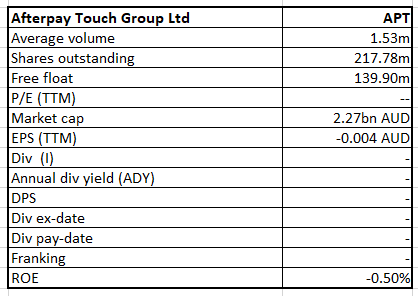

APT Details

Entrance into the US Market – Catalyst for Growth: Afterpay Touch Group Limited’s (ASX: APT) stock climbed up 4.598 per cent on July 18, 2018 as per the positive market sentiments related to the expecting great chance of repeating its success in the US markets. In the mid of May Month, the group announced that it will commence transacting in the United States in a phased manner with several significant lifestyle retailers and will provide U.S. customers with a new way to pay. U.S. launch partners include Urban Outfitters, Inc. (URBN), whose brands include Anthropologie, Free People and Urban Outfitters. We assume that it is a very important step for the company to expand its footprint in the US market because the US online fashion market size is 20 times higher than the Australian market (US$3.0 Bn). The early engagement has been positive across its initial target market with over 50 retailers having signed contracts or term sheets which are in varying stages of integration. Besides this, the group provided the strong business update for the three-month period ended 31 March 2018 wherein revenue increased by 400% and amounted to $1.45 Bn in Q3FY18 against prior corresponding period ($290 Mn in Q3FY17). Further, the company has recorded merchant growth of 45% in Q3FY18 against pcp while the number of new customers grew by 30% in Q3FY18 from the prior corresponding period. In past six months, the stock price was up by 33.85 per cent (as at July 17, 2018) and is trading at a point near to 52-week high level ($11.400).

.png)

Strong Overall Performance (Source: Company Reports)

Hence, we maintain our “Hold” recommendation at the current market price of $10.920, considering strong fundamentals and ongoing developments that involve expansions and new innovations which are the drivers for the sustainable growth.

.png)

APT Daily Chart (Source: Thomson Reuters)

Bionomics Limited

.png)

BNO Details'

Topline Data Expected to be Reported in Third Quarter 2018: Bionomics Limited (ASX: BNO) is a small cap biopharmaceutical company with the market capitalization of $ 243.81 Mn as of July 18, 2018. Recently, the group announced that it had completed treatment in its all 193-patient Phase II clinical study of BNC210 for post-traumatic stress disorder (PTSD). The RESTORE clinical study completed the treatment phase on time and the company stated that it aims to provide topline data by the end of the third quarter 2018. According to the release, the group had enrolled 193 patients under RESTORE trials at it 25 clinical sites in the US and Australia. During the trial period, patients were evaluated by using the Clinician-Administered PTSD Scale for DSM-5 (CAPS-5) as the primary endpoint. The study was also about examining the anxiety and depression level, which could provide insight into other avenues of treatment for the drug. On the balance sheet front, the current ratio and quick ratio stood at 6.17 x and 6.11 x in 1HF18, representing a healthy liquidity position of the firm. Account receivable days substantially increased from 87.6 days to 882.3 days in that past six months. However, we expect that the company will decrease its receivables days at the back of strategic management policy. The Group reported a cash balance of $32.254 Mn at 31 March 2018 with net operating cash inflow during the quarter ended 31 March 2018 of $0.158 Mn. Meanwhile, the stock price was declining for the last three months that is by 18.55 per cent post rising by 33% in last six months. Hence, we give a “Buy” recommendation on the stock at the current market price of $ 0.500, considering end-of-treatment milestone met in phase 2 clinical trial of BNC210 for the treatment of PTSD.

.png)

BNO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...