.png)

Stocks’ Details

New Hope Corporation Limited

Rise in Production Costs: New Hope Corporation Limited (ASX: NHC) is engaged in coal mining, exploration, port operation, conventional oil, etc. The market capitalisation of the company stood at $1.55 Bn as on 21st February 2020. The company recently updated the market with the activities for the quarter ended 31st January 2020 and stated that it has experienced continued improvement in safety performance. For the six months ended 31st January 2020, the company reported an incremental increase in Bengalla production, which stood at 5.4 million tonnes. There was a rise in production costs per tonne at New Acland because of the decline in production rate as a result of decline in reserves at Stage 2.

.png)

Production Statistics (Source: Company Reports)

Focus for Future: The company is well placed to address the rising energy demands of its Asian customers. With respect to coal operations, the company is planning to increase production levels and aims for careful cost management.

Valuation Methodology:P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:Net margin of the company stood at 16.1% in FY19 as compared to the industry median of 12.5%. This reflects that the company has better capabilities to convert its topline into the bottom line against the broader industry. Gross margin and EBITDA margin of the company stood at 45.2% and 39.6%, against the industry median of 42.9% and 32.2%, respectively. We have valued the stock using P/E based-relative valuation method, and for the purpose, we have taken peer such as Coronado Global Resources Inc (ASX: CRN), Fortescue Metals Group Ltd (ASX: FMG) and Rio Tinto Ltd (ASX: RIO). We have arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering the growth in margin, capabilities to convert the topline into profits and decent valuation upside, we give a “Buy” recommendation on the stock at the current market price of $1.595 per share, down by 14.247% on 21st February 2020.

Cochlear Limited

Rise in Reported Net Profit: Cochlear Limited (ASX: COH) is involved in the sale and manufacturing of the Cochlear implant system. The market capitalisation of the company stood at $14.02 Bn as on 21st February 2020. For the half-year ended 31st December 2019, the company reported sales revenue amounting to $777.6 million with a rise of 9%. It also experienced a rise of 23% to $157.7 million in reported net profit. This comprises $25.0 million of non-cash after-tax gains from the revaluation of innovation fund investments. The company is increasing its investment in R&D for advancing the long-term technology development pipeline. The Board of the company declared an interim dividend amounting to $1.60 per share with a rise of 3%, reflecting a payout ratio of 70% of underlying net profit.

.png)

Sales Revenue (Source: Company Reports)

Fall in Guidance: Due to an anticipated impact from the novel coronavirus, the company has reduced its underlying net profit guidance from the range of $290-300 million to $270-290 million. However, the reduced guidance reflects a rise of 2%-9% on the underlying net profit of FY19. For FY20, the company anticipates capital expenditure and investments to rise to ~$180 million. COH expects continued strong growth in cochlear implant units in developed markets for 2H.

Valuation Methodology:EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company possesses substantial free cash flow, which provides funding for market growth activities and R&D. This also provides the capability to reward shareholders with a growing dividend stream. We have valued the stock using EV/Sales based relative valuation method and for the purpose, we have taken peers such as CSL Ltd (ASX: CSL), Resmed Inc (ASX: RMD), Sonic Healthcare Ltd (ASX: SHL) etc., and arrived at a target price, which is offering corrections of high single-digit (in percentage terms). As per ASX, the stock of COH is trading towards its 52-week high levels of $254.400. Thus, in light of expected correction in valuations and current trading levels, we give an “Expensive” recommendation on the stock at the current market price of $231.600 per share, down by 4.436% on 21st February 2020.

EML Payments Limited

Robust Rise in GDV: EML Payments Limited (ASX: EML) is an issuer of pre-paid financial cards. The market capitalisation of the company stood at $1.55 Bn as on 21st February 2020. For 1HFY20, the company reported a rise of 59% in Gross Debit Volume on pcp, which amounted to $6.6 billion. GDV reflects the debit volume processed by the Group via its proprietary processing platforms. EML experienced a decent rise in group revenue of 25% to $59.2 million. This has been fueled by the impact of its acquisition of Flex-eCard in late FY19. Moreover, the company has inked a binding agreement for the acquisition of PFS in consideration of an enterprise value amounting to GBP226 million plus an earn-out of up to GBP55 million.

.png)

Financial Overview (Source: Company Reports)

EBITDA Guidance for FY20: The company is expecting EBITDA in the range of $39.5 million-$42.5 million for FY20, which reflects growth of 36%-43%. Moreover, it expects revenue in the ambit of $120 million - $129 million.

Stock Recommendation: Gross margin and EBITDA margin of the company stood at 75.1% and 24.6% in FY19. Net margin of the company stood at 8.7% in FY19 with YoY growth of 5.6%. This reflects that the company has improved its position to convert its topline into the bottom line. Return on equity of the company stood at 6.2% in FY19 as compared to 1.8% in FY18. Debt to equity multiple of the company stood at 0.10x in FY19 as compared to the industry median of 0.48x. Therefore, considering the growth in key margins, a deleveraged balance sheet, as well as recent acquisition, we give a “Hold” recommendation on the stock at the current market price of $4.630 per share, down by 2.526% on 21st February 2020.

Perpetual Limited

Fall in Net Profit After Tax: Perpetual Limited (ASX: PPT) is engaged in portfolio management, financial planning, executor services, investment administration and custody services. The market capitalisation of the company stood at $2.22 Bn as on 21st February 2020. During 1HFY20, the company reported a fall of 14% in NPAT, which amounted to $51.6 million. This fall in NPAT is due to net outflows, lower performance fees, and investment in strategic growth initiatives. The company experienced strong growth in Perpetual Corporate Trust in all lines of business. The Board of the company declared a fully franked interim dividend amounting to 105 cents per share, which is in line with the dividend policy of PPT.

.png)

Financial Performance (Source: Company Reports)

Outlook: The company is optimistic about the medium to long term outlook. The strategy of the company revolves around diversifying the business by adding new investment capabilities.

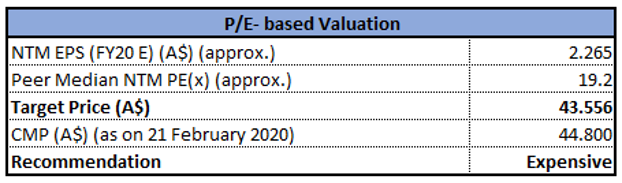

Valuation Methodology:P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 1.91x in FY19, reflecting YoY growth of 10.5%. This implies that the company has improved its position to address its short-term obligations. Return on equity of the company stood at 17.5% in FY19 as compared to the industry median of 6.3%, demonstrating decent returns provided to shareholders. We have valued the stock using P/E based-relative valuation method, and for the purpose, we have taken peers such as Pendal Group Ltd (ASX: PDL), Magellan Financial Group Ltd (ASX: MFG), Platinum Asset Management Ltd (ASX: PTM) etc., and arrived at a target price, which is offering corrections of lower single-digit (in percentage terms). As per ASX, the stock of PPT is trading close to its 52-week high level of $47.470. Thus, considering the expected correction in stock price and current trading levels, we give an “Expensive” recommendation on the stock at the current market price of $44.800 per share, down by 5.225% on 21st February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...