Costa Groups Holdings Limited

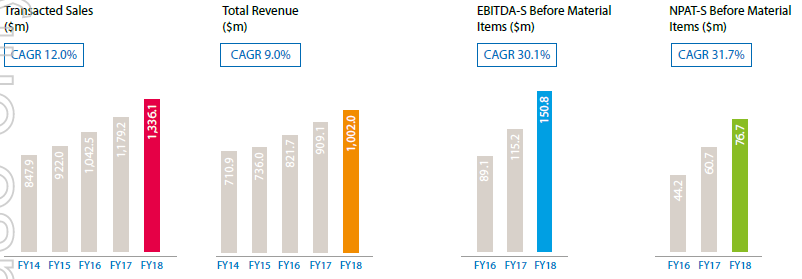

Strong Product Portfolio: Costa Groups Holdings Limited (ASX: CGC) is Australia’s leading grower, packer, and marketer of premium fresh fruits and vegetables & had a market capitalization of $2.20 Bn as on November 19, 2018. The company for the FY 2018 has clocked a revenue of $1,002 Mn, up 10.2% on PCP basis. It was mainly driven by the expansion of its international segment and continued development of its production capacity across its produce segment. Resultantly, EBITDA before SGARA grew by 30.9% to $150.8 Mn in FY18 as compared to the prior year. NPAT-S before material items came in at $76.7 Mn in FY18, exhibiting decent growth of 16.0% on Y-o-Y basis. On category wise, this year, the citrus category gave a strong performance because of the excellent crop quality and the strong export demand, however, the blueberry production was impacted by the lower yields due to pest pressures. This was also a robust year for the tomato category with yields surpassing the expectations. Henceforth, it is expected that the company will continue to build its capacities and significant growth in FY19 and will deliver low double-digit NPAT-S growth in the year ahead to 30 June 2019 on the back of robust growth in mushroom, avocados, tomatoes, and berries. In the meantime, the group’s financial position remains strong enough to undertake any further inorganic expansion required for growth purposes.

Recently, the company has entered into a conditional agreement for the acquisition of Nangiloc Colignan farms which is a grower of high-quality citrus and grapes. The objective of this acquisition is to open up the growth opportunity which is not available in the South Australian Riverland. The acquisition is expected to be completed in late 2018.

CGC’s key Financial metrics trends (Source: Company Reports)

Meanwhile, the stock price has risen by a modest 9.19 % over the past one month, also the YTD performance exhibits a return of 4.71%. Hence, considering the strong portfolio that it has and the underlying growth prospects, we maintain our “Hold” recommendation on the stock at the current market price of $6.970.

G8 Education Limited

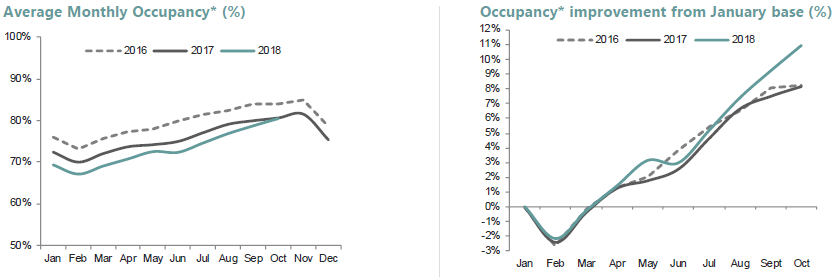

Decent Financials in 1HCY18: G8 Education Ltd (ASX: GEM) provides community-focused child care for families to foster their child's development. The Company also conducts a range of child care services that include child care centres acquisition, child care centres management, and industry-related project management, services and consultancy. The company is Australia’s largest for-profit early education provider & has a market capitalization of $1.29 Bn as on November 19, 2018. The company has a network of ~516 centres across the country. On the financial front, it posted decent 1H CY18 results with net revenue coming in 7.6% higher at $396.4 Mn compared to the prior corresponding period (PCP). It was mainly driven by fee increase, acquisitions, and new centre openings during the same period. However, underlying EBIT decreased by 21% in 1HCY18 against the prior corresponding period. It was primarily impacted by the rise of wages in Q1CY18 from regulatory changes to required staff ratios. Additionally, for CY18, the company is expected to deliver EBIT of $134 Mn to $136 Mn underpin by 2017 brownfield performance and wages performance which is line with expectation. With solid EBIT cash flow conversion of 99%, the balance sheet refinancing being on track and early adoption of the previously announced proportionate dividend policy, the Group is well positioned to drive the current growth phase while maintaining conservative gearing ratio of 29%.

On the other hand, we expect that going forward in CY 2018, the company will continue to face stiff competition due to oversupply & thus resulting in lower occupancy rates. Therefore, the company plans to respond to such an environment by focusing upon its Customer relationship management system which is expected to improve the conversion of inquiries, also the new government’s funding package is expected to drive the demand in the sector. Moreover, with all the investments that have been made by the firm over the past couple of years, the company seems to be well poised to reap the benefits of any opportunities that come over.

GEM’s Average Monthly occupancy rates & improvement trends (Source: Company report)

Meanwhile, the stock price has risen 11.37% in the past six months and up by 15.92% in the past one week (as on November 16, 2018). Thus, considering the improving occupancy margins in the 2H CY 2018 & increasing demand because of the Govt’s funding package, we maintain our “Hold” recommendation on the stock at the current market price of $2.930.

Future Generation Investment Company Limited

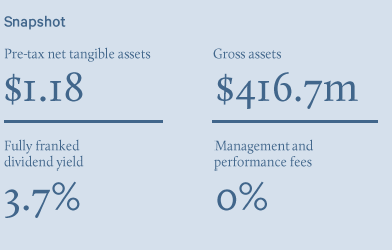

Decent Investment portfolio outperformance: Future Generation Investment Company Limited (ASX: FGX) is an investment company incorporated in Australia. The objective of the company is to provide exposure to a group of prominent Australian fund managers in a single investment vehicle. Recently, the company has successfully raised more than $43.9 Mn capital through its private placement programme. The shares were offered at an issue price of $1.18 per share. These additional funds will increase its annual investments in the Australian charities focused on children and youth at risk. The proceed of the additional capital will be invested in managing the company’s investment portfolio and redeeming investment. As at 31 October 2018, the firm’s Investment portfolio has provided an annual average performance of 8.5% per annum since inception thus outperforming the benchmark by 2.8%. This performance has been achieved with less volatility, i.e., 7.4% as compared to the market of 11.2%. FGX’s gross assets on 31 October 2018 were clocked at $416.7 Mn, of which 47.1% of the assets were allocated to long equities, 36.6% to absolute bias and 15.4% to market neutral strategies. The company has a market cap of $419.10 Mn as on November 19, 2018.

Growth Proposition: For the period ended 31 October 2018, the investment portfolio delivered a modest performance by increasing 4.9% thus outperforming the S&P/ASX All Ordinaries Accumulation Index by 1.8% considering a span of last one year and the outperformance of 2.8% is visible when the performance is evaluated since inception. Moreover, the net tangible assets as on date amounted to $1.18 per share.

Investment Update as on 31 October 2018 (Source: Company Reports)

Meanwhile, the stock price has fallen over the past one month by 7.75% and traded close to lower level of $1.130. Thus, considering the Investment portfolio’s outperformance over the benchmark & robust Net tangible assets position, we recommend a “Buy” rating on the stock at the current market price of $1.180.

Tabcorp Holdings Limited

Strong growth across the platforms along with operating synergies: Tabcorp Holdings Limited (ASX: TAH) operates as a holding company. The Company, through its subsidiaries, provides gambling, gaming, wagering, and entertainment services. Tabcorp Holdings serves customers in Australia and the United Kingdom. The company has a market cap of $9.11 Bn as on November 19, 2018. The company reported an EBITDA of $255.6 Mn up by more than 100% on PCP & a statutory NPAT of $28.7 Mn in FY 2018. The group delivered a strong second half year performance on the back off ‘Lotteries & Keno’ and ‘Wagering & Media’ business divisions which were attained because of the phenomenal growth in the digital platform as well as modest growth in their retail network. The financial position of the firm looks sound enough with successful refinancing of the $1.8 Bn Bridge facility which was taken to fund the Tatts combination. The company also issued US$ 1.4 Bn of notes to the US private placement market, with long-dated maturity thus these transactions have reduced the financial risk profile of the firm. The company has declared a fully franked final dividend of 10cps for the year ended.

Moreover, the company has completed its combination with the Tatts group & hence operates a diversified set of market-leading businesses. The firm is a market leader with a domestic market share of ~84% & 57% in the “Lotteries & Keno” and “wagering & media” segments, respectively. Thus, these well-established service segments underpin the stability of earnings. The recent ban on synthetic lottery & keno betting has brought in the much-needed regulatory certainty. The wagering and media segment remain to be very competitive however the firm’s unique combination of assets creates an opportunity to develop a differentiated customer experience and value proposition. Also, the completed combination with Tatts group is expected to create EBITDA synergies of at least $130 Mn in FY 21.

.png)

Australian gambling expenses by product segment (Source: Company Reports)

Meanwhile, the stock price has fallen 3.12% in the past three months as of November 16, 2018 and traded close to the 52-week lower level of $4.165. We believe that the company is poised to grow with the stable regulatory norms as well as the synergies on account of the combinations completed by it. Thus, we maintain our “Buy” recommendation on the stock at the current market price of $4.510.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...