Crown Resorts Ltd

.png)

CWN Details

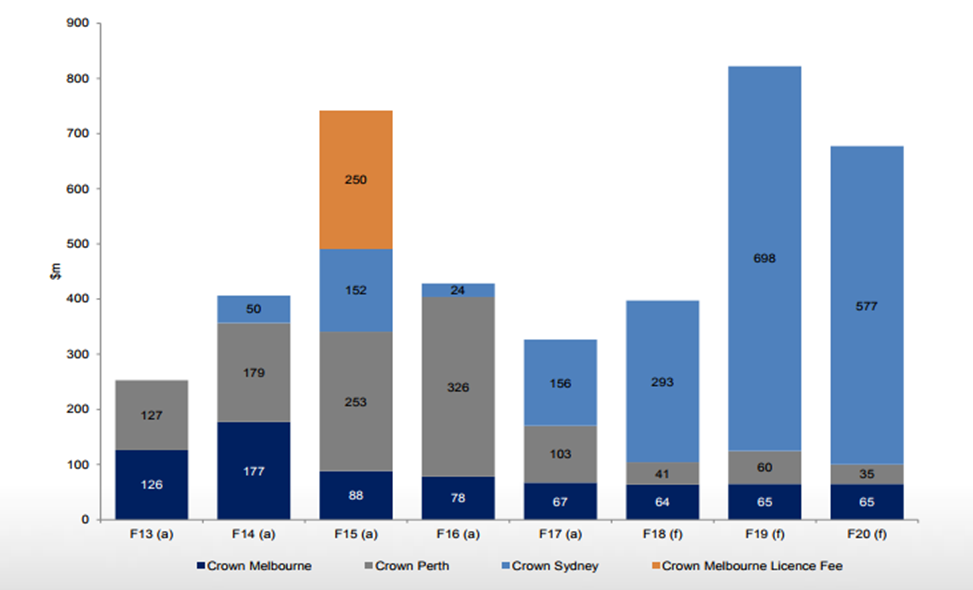

Improving performance: Crown Resorts Ltd (ASX: CWN) has been putting efforts in reducing opex to offset weak VIP business and managing gearing for potential partnership strategies. The group’s revenue from main floor gaming (excluding VIP program play revenue) was slightly up during July 1 to October 22, 2017 as compared to the prior corresponding period. Crown Melbourne’s main floor gaming revenue improved from prior corresponding period, but the non-gaming revenue was flat. Nonetheless, Crown Melbourne’s VIP program play turnover was better than expected and wagering and online businesses continued to show good revenue growth.

Investment in Australian Resorts (Source: Company Reports)

CWN stock rallied over 6.3% in the last four weeks (as of November 10, 2017) and has a strong dividend yield. The group is also expected to benefit from the rising number of travelers from Asia while CWN is building a healthy portfolio. The challenges owing to which CWN’s FY17 NPAT was down 15.5% seem to be subsiding in a gradual manner. We give a “Buy” recommendation on the stock at the current price of $12.17

.png)

CWN Daily Chart (Source: Thomson Reuters)

Bendigo and Adelaide Bank Ltd

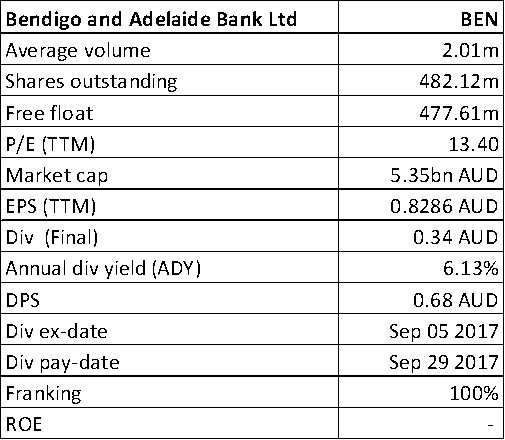

BEN Details

Concerns over bank’s fee income: Bendigo and Adelaide Bank Ltd (ASX: BEN) confirmed an aggregate offer size of $300 million while the margin has been set at 3.75% per annum with respect to its convertible Preference Shares 4. On the other hand, bank’s fee income remains a concern impacted by some factors like the recent removal of foreign ATM fees by some of the larger players. The group has thus forecasted a rise in costs of over 2%. Moreover, all the banks are forced to comply with the APRA requirements post the global financial crisis hurting the investor and interest only lending. The group’s medium-term outlook is challenging while the recent margin trends look decent. BEN’s re-pricing measures also appear to have impacted its balance sheet growth. The stock lost over 14.2% in this year to date (as of November 10, 2017) and we believe this pressure in the stock will continue in the coming months. We give an “Expensive” recommendation at the current price of $11.16

.png)

BEN Daily Chart (Source: Thomson Reuters)

FlexiGroup Ltd

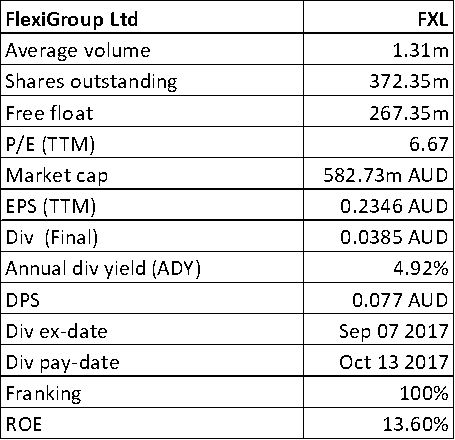

FXL Details

Efforts on digitization: FlexiGroup Ltd (ASX: FXL) delivered a statutory NPAT from continuing operations of $87.4 million in 2017 which is a rise of 74% on a year over year basis. The group declared a fully franked final dividend of 3.85 cents per share, leading to a total dividend of 7.7c per share. The group has built a large seller network of over 13,000 merchants. FXL also launched a proprietary, modern and mobile-friendly cards technology platform to expand the market in New Zealand. FXL Australian cards’ business performance across all key metrics was strong including 55% growth in receivables to $483 million.

Strategic Priorities (Source: Company Reports)

The group is well positioned to achieve $1 billion receivables and $35 million cash NPAT by FY20 for the Australian cards business. The group is also investing in capabilities with digitization and business consolidation efforts being undertaken. We give a “Speculative Buy” on the stock at the current price of $1.59

.png)

FXL Daily Chart (Source: Thomson Reuters)

Charter Hall Retail REIT

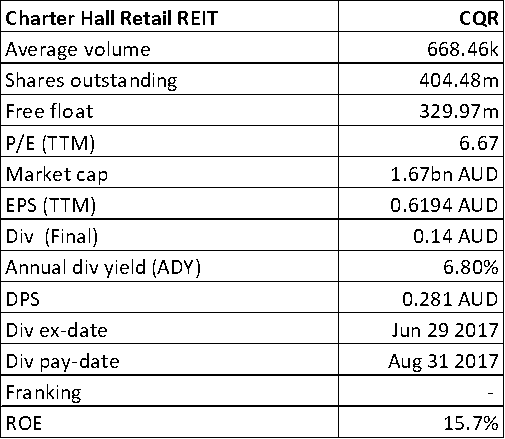

CQR Details

Sustainable income growth through acquisition and divestments: Charter Hall Retail REIT (ASX: CQR) had reported a property portfolio of 71 shopping centers, valued at $2.8 billion as at 30 June 2017. The group sold eight lower growth assets for $157.2 million at an average yield of 6.5% in FY17 to maintain their asset quality. Accordingly, they acquired three higher-growth, multi-tenanted assets for $282.6 million which included Salamander Bay Centre, NSW, Arana Hills Plaza, Qld, and Highfields Village, Qld. The group reported a 9% rise in NTA per unit to $4.13, with a 2.5% increase in operating earnings to $123.3 million. Earnings reached 30.4 cents per unit and unitholders while the group paid a full year distribution of 28.1 cents per unit, representing a payout ratio of 92.4%. Trading at an outstanding dividend yield at the back of growth based on a strong portfolio of neighborhood and sub-regional assets, we give a “Hold” recommendation on the stock at the current price of $4.14

.png)

CQR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...