.png)

Stocks’ Details

Ramelius Resources Limited

Latest Exploration Results: Ramelius Resources Limited (ASX: RMS) is engaged in the exploration, mine development, mine operations and the production and sale of gold. The market capitalisation of the company stood at $1.26 billion as on 10th June 2020. Recently, the company notified the market with excellent exploration results from West Australian gold projects. RMS added that significant gold mineralisation continues to be intersected at the Penny Project from deeper infill RC and diamond drill results such as 4m at 18.06 g/t Au from 216m, including 2m at 31.63 g/t Au and 3m at 18.42 g/t Au from 184m, including 2m at 27.39 g/t Au. At Mount Magnet, Eridanus continues to deliver very robust thicknesses of mineralised granodiorite below the designed Stage 2 pit cutback. Moreover, exploration around Edna May has also discovered a new drill target through reconnaissance Aircore drilling.

Recently, the company acquired Spectrum Metals Limited and currently has 91.29% stake of Spectrum. During the quarter ended March 2020, the company reported gold production of 51,825 ounces at an AISC of A$1,248/oz. RMS sold 53,173 ounces of gold at an average gold price of A$1,937/oz during the quarter.

.png)

FY20 Group Production Profile (Source: Company Reports)

Guidance: For FY20, the company expects gold production in the range of 210,000 ounces - 220,000 ounces at an improved AISC of between A$1,150/oz – 1,250/oz.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company closed the quarter with cash & gold balance of $125.4 million as compared to $87.7 million in December quarter. Net margin of the company stood at 12.9% in 1H FY20, reflecting YoY growth of 10.3%. This implies that the company has improved its capabilities to convert its topline into the bottom line. Debt to equity of the company stood at 0.10x against the industry median of 0.21x. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers such as Silver Lake Resources Ltd (ASX: SLR), Regis Resources Ltd (ASX: RRL), Gold Road Resources Ltd (ASX: GOR), etc. Hence, considering the recent acquisition of Spectrum Metals Limited, excellent exploration results from West Australian gold projects, improved net margins and deleveraged balance sheet, we give a “Hold” recommendation on the stock at the current market price of $1.655 per share, up by 4.088% on 10th June 2020.

Strike Energy Limited

Update on Exploration Targets: Strike Energy Limited (ASX: STX) is in the exploration of oil & gas. The market capitalisation of the company stood at $358.31 million as on 10th June 2020. The company recently provided an update on its high-value exploration targets in Greater Erregulla and Walyeirng regions. With respect to Greater Erregulla, the company stated that it has completed reprocessing of an initial subset of 23 historical 2D Seismic lines of several vintages, which covers the Greater Erregulla region. STX added that it experienced a decent improvement in data quality from the original dataset. In relation to Walyeirng region, the company has received final post-stack 3D seismic volumes. STX has wrapped up proprietary geological and geophysical workflows on this dataset.

During Q1 FY20, the company’s operations were focussed on preparation for the West Erregulla appraisal drilling campaign, which included long lead procurement for WE3, along with various Perth Basin seismic campaigns. STX invested considerable resources on its midstream tender process and pre-FEED activities for receipt of gas from West Erregulla. During the quarter, net cash outflow from the operating activities stood at $779,000.

.png)

Cash Flows (Source: Company Reports)

Outlook: The company is well capitalised to deliver targeted FID and commence exploration. The company is optimistic about the supportive and tightening WA gas market fundamental.

Stock Recommendation: Q1 FY20 witnessed the commencement of one of the sharpest economic downturns in history with the outbreak of COVID-19. In addition, the subsequent collapse in oil prices was preceded by a perceived oversupply in global LNG. The company managed to finish the quarter with a cash balance of $24.3 million and no debt. Therefore, in light of the aforesaid facts, focus of STX on preparation for the West Erregulla appraisal drilling campaign, and nil debt position, we give a “Hold” rating on the stock at the current market price of $0.205 per share, down by 2.381% on 10th June 2020.

Senex Energy Limited

Completion of Domestic Development Projects: Senex Energy Limited (ASX: SXY) is involved in the production and exploration of oil and gas. The market capitalisation of the company stood at $400.74 million as on 10th June 2020. Recently, the company announced that it has successfully finished 100% owned $400 million Surat Basin natural gas development project, which is placing the company as an important supplier of gas to the domestic market. In another update, the company announced that it would decrease natural gas supply to GLNG by approx. 1 PJ from June 2020 to August 2020 at the request of GLNG. This follows lower LNG offtake requirements at GLNG. The natural gas production continues to perform strongly at Roma North and Atlas in the Surat Basin, with production now surpassing 34 TJ/day.

Despite the outbreak of COVID-19 and lower oil prices, the company managed to deliver strong performance during March 2020 quarter with a production of 589 kboe, up by 31%. The production at Surat Basin gas continues to ramp and has exceeded 29 TJ/day.

.png)

Key Metrics (Source: Company Reports)

Upgraded Guidance: On the back of robust production performance throughout its Surat Basin assets, and assuming continued normal operations in the current pandemic environment, the company has upgraded its production guidance for in the range of 2.0 mmboe – 2.1 mmboe against the previous guidance of 1.8 mmboe – 2.0 mmboe. It anticipates EBITDA in the ambit of $45 million – $55 million.

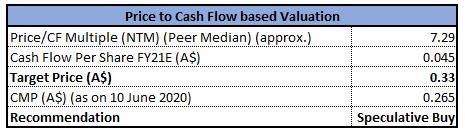

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company is in a strong financial position underpinned by diversified revenue streams, low-cost business model and free cashflow breakeven below US$30/bbl. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Cooper Energy Ltd (ASX: COE), Energy Resources of Australia Ltd (ASX: ERA), New Hope Corporation Ltd (ASX: NHC), etc. Thus, considering thestrong financial position, upgraded guidance and strong production at Surat Basin Gas, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.265 per share, down by 3.636% on 10th June 2020.

Karoon Energy Ltd

Acquisition of Baúna oil Field: Karoon Energy Ltd (ASX: KAR) is into oil and gas exploration. The market capitalisation of the company stood at $353.91 million as on 10th June 2020. The company recently announced that Mitsubishi UFJ Financial Group, Inc has made a change to their substantial holdings in the company on 1st June 2020 with the current voting power of 10.12% as compared to the previous voting power of 11.63%. During the March 2020 quarter, the company commenced a strategic review to assess whether strategic alternatives can deliver a superior outcome for shareholders in a post-pandemic world. KAR implemented permanent and temporary cost reductions including, consolidation and reduction of offices and workforce. The company is committed to complete the acquisition of the Baúna oil field and the undeveloped Patola oil discovery. The below picture gives an overview of cash flow from operating activities:

.png)

Cash Flow from Operating Activities (Source: Company Reports)

Positive about Future Energy: The company remains optimistic about the long-term future for energy despite the impact of COVID-19 on world energy markets in the short-term.

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

.png)

EV/EBITDA Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company is well funded with a cash balance of A$504.5 million and no drawn debt as at 31 March 2020. Gross margin of the company stood at 85.4% in 1H FY20 against the industry median of 52.1%. The stock of KAR has corrected 41.55% in the past six months, and as a result, it is inclined towards its 52-weeks low level of $0.340. We have valued the stock using EV/EBITDA based illustrative relative valuation method and arrived at a target price with an upside of low double-digit (in percentage terms). Thus, it can be said that the stock of KAR is undervalued at current trading levels. Hence, considering the strategic review, well-capitalised position and market conditions, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.630 per share, down by 1.562% on 10th June 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...