.png)

Stocks’ Details

Bingo Industries Limited

Medium Term Outlook Remains Positive:Bingo Industries Limited (ASX: BIN) provides recycling and waste management solutions, including waste collection, processing, separation and recycling components of the waste value chain.

Financial Performance for 1HFY20: During the half year ended 31st December 2019, the company reported robust growth in revenue and EBITDA, against a challenging operating environment. During the period, the company reported operating free cash flow amounting to $70.4 million, that went up by 49.1% on prior corresponding period. EPS for the period stood at 5.8 cents, up by 132% on the prior corresponding period EPS of 2.5 cents. On an operational front, the company has delivered good progress against its development program, with the completion of Mortdale and the Patons Lane advanced recycling equipment becoming fully operational.

.png)

Key Financial Metrics (Source: Company Reports)

Outlook: Going forward, the company aims to optimise its operations to maximise returns from assets and is targeting to achieve a cash conversion of 100%.For the full year FY20, the company expects to report solid growth, backed by the progress reported in the development program.

Stock Recommendation: The stock of the company generated positive returns of 29.58% over a period of 6 months. The company reported solid growth in 1HFY20 but expressed slight dissatisfaction at the same time with respect to certain controls. By FY21, the company expects several positive organisational and industrial factors to support the desired growth. Considering the robust performance in 1HFY20, strong balance sheet position, exuberant returns to shareholders, and a decent outlook, we give a “Hold” recommendation on the stock at the current market price of $3.170, down 0.938% on 20th February 2020.

Downer EDI Limited

DOW to Focus on Debt Reduction:Downer EDI Limited (ASX: DOW) designs and builds infrastructure and facilities and provides integrated services across Australia and New Zealand.

Half Yearly Performance: During the half year ended 31st December 2019, the company generated total revenue amounting to $6.8 billion, representing an increase of 3.3% on the prior corresponding period. EBITDA for the period came in at $214.8 million, down by 19.9% on the prior corresponding year. Growth in revenue was supported by the robust performance of the Road Services business, expanded contribution from Transport projects, along with a favourable performance of the Rollingstock Services business. EBITDA declined due to lower than expected performance by the Engineering, Construction and Maintenance (EC&M) division. During the year, the company’s gearing ratio increased due to lower operating cash flow as a result of project completion activities. Going forward, the company’s focus will be on reducing the gearing through debt reduction.

.png)

Financial Snapshot (Source: Company Reports)

Guidance: In FY20, the company expects NPATA before minority interests of ~$300 million. The guidance was revised by the company primarily due to underperformance of EC&M service line.

Valuation Methodology: EV/EBITDA Based Valuation

.png)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 18.49% over a period of 3 months and is currently inclined towards its 52-week low level of $6.450.While the management expressed its disappointment on 1HFY20 results, which were impacted by construction losses, the company’s confidence on future performance is based upon a strong pipeline of opportunities in its key markets, that boosted its work-in-hand to $46.4 billion as at 31st December 2019.We have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price with upside of lower double-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $6.900, up 2.985% on 20th February 2020.

Sydney Airport Limited

Coronavirus to Impact Traffic Performance in Feb’20:Sydney Airport Limited (ASX: SYD) owns and operates the Sydney Airport. The company recently updated about the traffic performance for January 2020. During the month, total traffic came in at 3.9 million passengers, down 0.6% on the prior corresponding month. While the traffic performance stood well despite the impact of bushfires, the company expects corona-virus outbreak to significantly impact the results in February.

.png)

Traffic Performance Jan’20 (Source: Company Reports)

FY19 Performance: During the year, the company’s passenger traffic remained almost flat in comparison to the previous year. However, revenue and EBITDA for the period went up on pcp, depicting the strength and resilience of the business. During the period, the company could maintain proper cost and quality control, with total controllable operating expenses going down by 1.6%. Success during the year can also be attributed to an increase in overall customer satisfaction scores across the international and domestic terminals. During the year, the company paid total dividend amounting to 39 cents per stapled security.

Valuation Methodology: EV/Sales Based Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over a period of 1 year, the stock gave positive returns of 22.32% and is currently moving towards its 52-week high level of $9.300. During FY19, the company made a capital investment of $300.8 million for expansion and enhanced customer experience. While the business has shown excellent resilience to bushfires in Australia, it may witness an economic shock due to the outbreak of coronavirus. Considering the above factors, we have valued the stock using EV/Sales based relative valuation method and arrived at a price correction of lower single-digit (in percentage terms). Hence, we have a watch stance on the stock at the current market price of $8.300, down 1.659% on 20th February 2020.

Qantas Airways Limited

Decent Performance in 1HFY20: Qantas Airways Limited (ASX: QAN) is one of the largest airlines based in Australia. The company recently announced about the off market buy back of shares, which is currently anticipated up to $150 million. Important dates with respect to the buyback are stated in the below picture:

.png)

Buy Back Schedule (Source: Company Reports)

First Half Performance: During the six months ended 31st December 2019, the company reported a strong financial performance on the back of capacity discipline, business transformation, and a growing market share. Underlying Profit Before Tax for the period came in at $771 million. Results were impacted by forex related cost impacts, global freight weakness, and increase in operating costs pertaining to sale of domestic airport terminals. The International segment performed well, reported a rise of $4 million in underlying EBIT. Returns to shareholders in the form of interim dividend payments and off-market share buy-back amounted to $647 million.

Outlook: During the second half, the company expects the impact of Coronavirus on the financial results. EBIT for the half is anticipated to see a negative impact in the range of $100 million - $150 million.

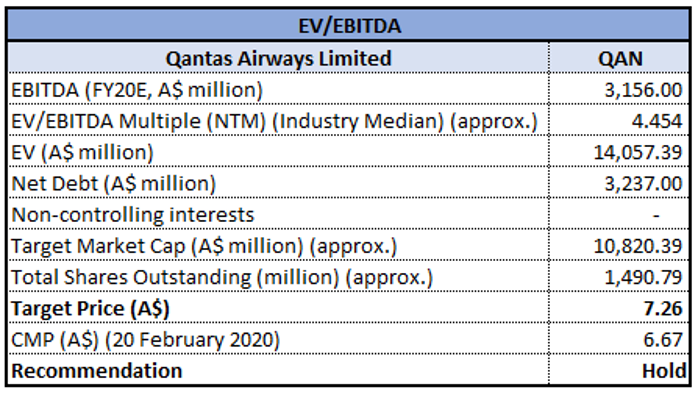

Valuation Methodology: EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over a period of 6 months, the stock of the company gave positive returns of 11.70%. The management stated that growth in the international segment helped offset the disruptions in Hong Kong. During 1HFY20, the company was able to deliver a convincing performance and is currently planning for a safeguard strategy against the upcoming adverse impacts due to Coronavirus. We have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price with upside of higher single-digit (in percentage terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $6.670, up 5.873% on 20th February 2020, taking cues from the release of half yearly results.

Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...