Stocks’ Details

BINGO Industries Limited

Modifications Approval Received for Recycling and Landfill Facility: BINGO Industries Limited (ASX: BIN) is a fully integrated recycling and resource management company focussed on providing solutions across the entire waste management supply chain. On 30 April 2020, the company announced that the New South Wales Independent Planning Commission has given approval for the proposed modification (Mod. 6) to BINGO’s existing planning approval at its recycling and landfill facility at Eastern Creek. This approval will help BINGO to create operational and network efficiencies in the near term and operate its current recycling facilities for more hours.

Covid-19 Update: On 23 March 2020, the company provided an update on Covid-19, wherein informed that it has withdrawn its FY20 earnings guidance, due to the uncertainty surrounding the pandemic. In response to Covid-19, the company is taking proactive measures to ensure the safety of its people and for the preservation of its cash flow. Further, the company has taken several measures to lower its capital expenditure.

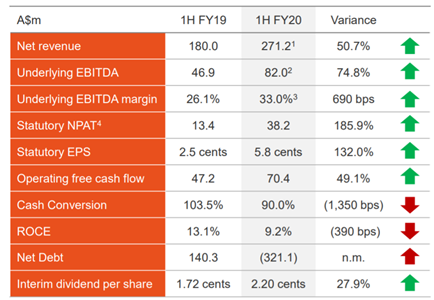

H1FY20 Performance: In the first half of FY20, the company reported strong revenue growth of 50.7%, underlying EBITDA growth of 67.9% and underlying EBITDA growth of 74.8%. During the period, the company saw strong growth in operating free cash flow which increased by 49.1% to $70.4 million.

H1FY20 Results Snapshot (Source: Company Reports)

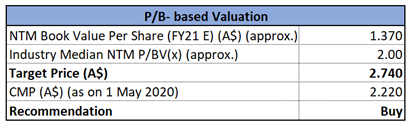

Valuation Methodology: P/BV Multiple Based Relative Valuation (Illustrative)

P/BV Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the past three months, the stock of BIN has declined by 15.47% and is currently trading towards its 52-week low, offering investors a decent opportunity for accumulation. The company currently enjoys a strong balance sheet, backed by significant property assets. We have valued the stock using Price to Book multiple based illustrative relative valuation method and arrived at a target price with lower double-digit upside (in percentage terms). Considering the company’s proactive measures taken in response to Covid-19 situation, it strong balance sheet, and recent modification approval, we give a “Buy” recommendation to the stock at the current market price of $2.220, down by 5.532% on 1st May 2020.

Cleanaway Waste Management Limited

Covid-19 Update: Cleanaway Waste Management Limited (ASX: CWY) is primarily involved in providing integrated total waste management solutions to its clients. On 24 March 2020, the company provided a trading update, wherein it informed that its financial performance for FY20 is currently in-line with its internal forecasts and FY20 earnings guidance and till date it has not observed any material change in volumes across any of its operating segments. However, due to the uncertainty surrounding the Covid-19 impacts, the company has suspended its earnings guidance.

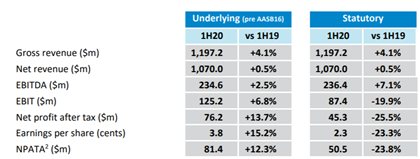

H1FY20 Results Highlights: For the six months ended 31 December 2019, the company reported Underlying NPAT of $76.2 million, up 13.7% on pcp. For the same time span, the company reported Underlying EBITDA of $234.6 million, up 2.5% on pcp. During the period the company completed the acquisition of the SKM recycling assets and the acquisition of a small solid waste collections business in western Victoria.

H1FY20 Results Snapshot (Source: Company Reports)

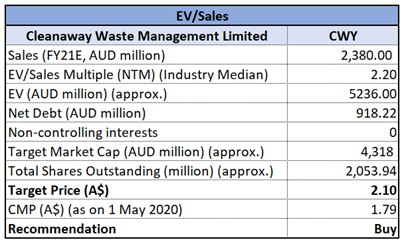

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months,

Stock Recommendation: The company currently enjoys strong balance sheet and significant liquidity, with over $357 million of committed headroom available at the end of February 2020 under existing banking facilities. We have valued the stock using EV/Sales based illustrative relative valuation method and arrived at a target price with lower double-digit upside (in percentage terms). Considering the company’s decent performance in the first half of FY20, its decent balance sheet, and its resilient performance amid Covid-19, we give a “Buy” recommendation on the stock at the current market price of $1.790, down by 4.278% on 1st May 2020.

NRW Holdings Limited

Retaining Access to Maximum Liquidity: NRW Holdings Limited (ASX: NWH) is a diversified provider of contract services to the resources and infrastructure sectors in Australia. On 26 March 2020, the company provided an update, wherein it informed that it has the ability to operate within its current cash and working capital facilities. However, to ensure that it retains access to the maximum liquidity available, it has decided to defer its interim dividend. Further, the company has implemented working practices in all operations across the group to minimise the risks from Covid-19.

H1FY20 Performance Highlights: In the first half of FY20, the company reported revenue of $808.7 million, up 55% on pcp. Further, the company reported NPATA of $41.2 million, up by 28% on pcp. During the period, the company completed the acquisitions of RCRMT and BGC Contracting.

H1FY20 Results Snapshot (Source: Company Reports)

What to expect: The acquisition of BGC is expected to make a significant contribution to the second half performance and support further business growth. For FY20, the company is expected to earn revenue of circa $2.0 billion, subject to any impact from Covid-19.

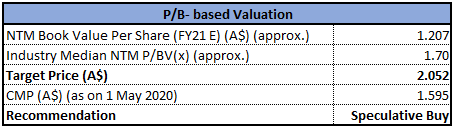

Valuation Methodology: P/BV Multiple Based Relative Valuation (Illustrative)

P/BV Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of NWH has declined by 24.22% in the last six months and is currently inclined towards its 52-week low. We have valued the stock using Price to Book Value multiple based illustrative relative valuation method and arrived at a target price with lower double-digit upside (in percentage terms). Considering the company’s recent steps on retaining access to the maximum liquidity, its decent H1FY20 results and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.595, down by 6.452% on 1 May 2020.

Decmil Group Limited

Significant Boost to Order Book: Decmil Group Limited (ASX: DCG) is a diversified industrial services provider involved in providing engineering and construction; accommodation services; and maintenance. The company recently announced two new projects in Queensland and Western Australia worth $36 million, bringing Decmil’s order book to $411 million. In Western Australia, the company has been confirmed as a contractor on the Bayswater Station Metronet project and in Queensland, it has been named preferred tenderer for an $11.5 million contract for roadworks on the Bruce Highway.

Closure of New Zealand subsidiary: On 16 April 2020, the company announced regarding the closing of its New Zealand subsidiary Decmil Construction NZ Limited (DCNZ). DCNZ suffered significant losses as a result of termination of a major contract by the NZ Department of Corrections, hence it became important for DCG to avoid incurring any additional liabilities, cease trading and wind up the New Zealand subsidiary’s affairs. The company has assured that its core Australian operations are not impacted by the closure of the New Zealand subsidiary and it remains positive on the outlook of the Australian business, which continues to add to its healthy pipeline of work in hand.

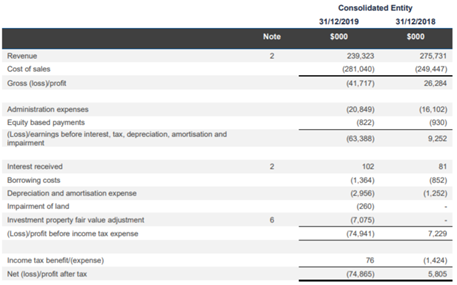

H1FY20 Results: In the first half of FY20, the company reported group revenue of $239 million and incurred a loss of $75 million. During the period, the company secured $207 million in new contracts, primarily from government customers. For FY20, the company has contracted revenue of ~$500 million, but coronavirus restrictions have the potential to impact timing. In FY20, the company expects its revenue to be in the range of $475 – $525 million, assuming construction sites in Australia are not shut down due to Coronavirus.

H1FY20 Income Statement (Source: Company Reports)

Stock Recommendation: In the past six months, DCG’s stock has declined by 73.84% on ASX and is trading near to its 52 weeks low price of $0.065, offering investors a decent opportunity for accumulation. On TTM basis, DCG is trading at a Price to Book multiple of 0.2x, lower than the Industry Median (Construction & Engineering) of 1.2x. Considering the aforesaid facts, the company’s recent boost in the order book, and its current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.210, down by 6.667% on 01 May 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...