.png)

Stocks’ Details

Macquarie Group Limited

Macquarie Bank Capital Notes 2 Bookbuild: Macquarie Group Limited (ASX: MQG) is a non-operating holding company which provides financial services like banking, financial advisory, investment and funds management services. As on 26 May 2020, the market capitalization of the company stood at $37.62 billion. The company has recently completed the bookbuild for its Macquarie Bank Capital Notes 2 which consisted of an institutional offer, a broker firm offer, and a securityholder offer and has opened its offer with a margin of 4.70% per annum. The size of the offer has been set at $500 million and will close on 29 May 2020. The bank has recently notified that Credit Suisse Holdings Limited ceased to be a substantial holder.

Financial and Operational Highlights: The company has recently released its results for the year ended 31 March 2020, wherein it reported an increase of 13% in annuity-style activities profit to $3,439 million but a fall of 35% in markets-facing activities profit to $2,009 million. In the same time span, the company witnessed a decline of 8% in net profit of $2,731 million.

.png)

FY20 Financial Highlights (Source: Company Reports)

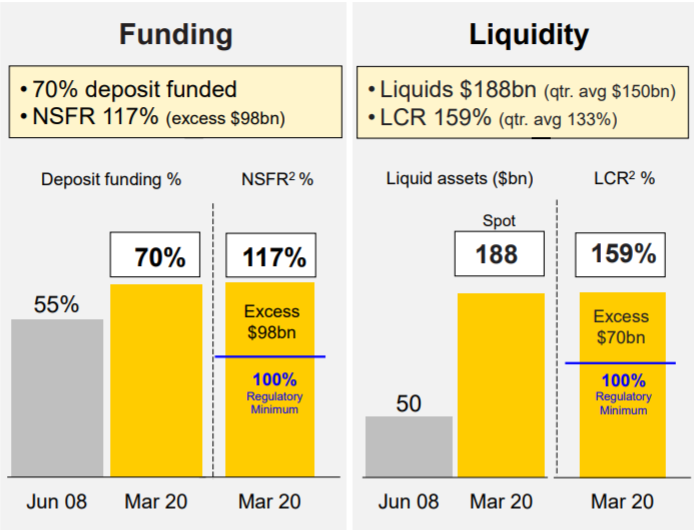

Outlook: Whilst the outlook is uncertain owing to the spread of the coronavirus, the company is expecting recovery in next 18 months. The company has a strong funded balance sheet with sufficient liquidity and strong regulatory ratios. Macquarie has been successful in pursuing its strategy of diversifying its funding sources by growing its deposit base. The company maintains a cautious stance with a conservative approach to capital, funding, and liquidity.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The diversity of the company’s operations, combined with a strong capital position and robust risk management framework has contributed to Macquarie’s 51-year record of unbroken profitability. As per ASX, the stock of MQG gave a negative return of 22.80% on YTD basis but a positive return of 7.24% in the past one month. The stock is also trading near the average of 52-weeks’ trading band of $70.45-$152.35. Considering the volatility in returns, current trading levels, and decent financial performance, we have valued the stock using price to earnings multiple based illustrative relative valuation method and have arrived at a downside of low single-digit (in percentage terms). Hence, we suggest investors to wait for the price correction and have a watch stance on the stock at the current market price of $108.71, up by 2.392% on 26 May 2020.

National Australia Bank Limited

NAB Completes A$3 Billion Institutional Placement: National Australia Bank Limited (ASX: NAB) provides banking services, access card services, international banking, fund management etc. As on 26 May 2020, the market capitalization of the company stood at ~$50.34 billion. The bank has successfully completed a $3 billion fully underwritten institutional placement wherein it issued 212 million new fully paid ordinary shares at a price of $14.15 per share.

Sound Divisional Performances but Covid-19 Impact at Group Level: During the half year ended 31 March 2020, the bank reported statutory profit of $1,313 million and cash earnings of $2,471 million. NAB is supporting over 1.5 million customers and has made a solid progress on transformation via cost management and productivity savings. The decent financial and operational performance enabled the Board to declare a dividend of 30 cents per share, payable on 3 July 2020.

.png)

1H20 Financial Highlights (Source: Company Reports)

What to Expect: The bank is making the decisions for the long-term to deliver sustainable outcomes for its stakeholders and is emphasizing on managing its costs base. The bank is well-positioned to return to growth post COVID-19 and maximize its organic capital generation. The bank will release its third quarter trading update on 14 August 2020.

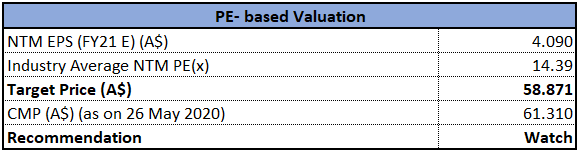

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of NAB is trading close to its 52-weeks’ low level of $13.195, proffering a decent opportunity for accumulation. Despite the market uncertainty posed by COVID-19, the bank continues to show resilience and is well positioned to benefit from further growth opportunities. Considering the trading levels, decent financial performance amidst the global pandemic and positive long term outlook, we have valued the stock using price to cash flow multiple based illustrative relative valuation approach and have arrived at a target price with an upside of low double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $16.64, up by 5.651% on 26 May 2020.

Westpac Banking Corporation

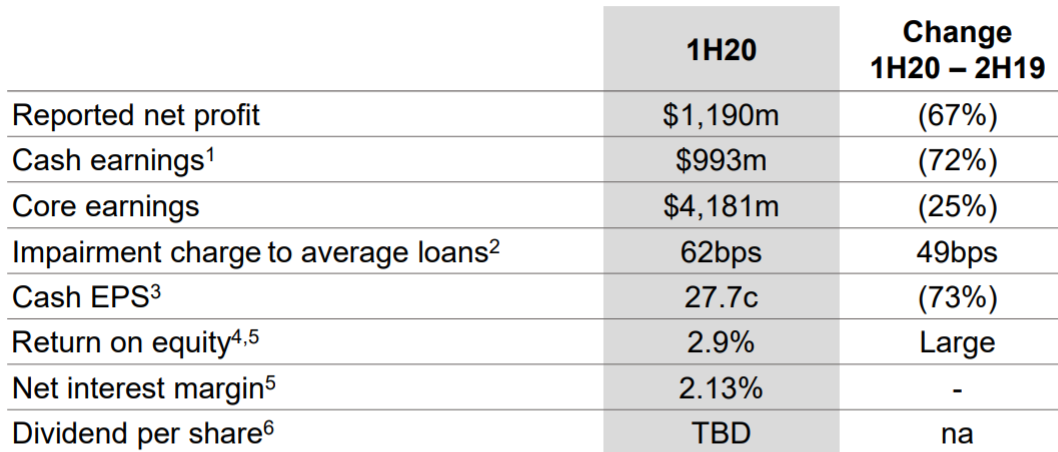

Strong Balance Sheet: Westpac Banking Corporation (ASX: WBC) provides financial services including lending, deposit taking, general finance etc. As on 26 May 2020, the market capitalization of the company stood at $55.37 billion. The bank has recently released its interim results for the period ended 31 March 2020 wherein it reported a strong balance sheet with strong capital, funding, and liquidity. During the half-year, the bank reported a net profit of $1,190 million and cash earnings of $993 million. In the same time span, return on equity of the company was 2.9% and net interest margin stood at 2.13%.

1H20 Financial Highlights (Source: Company Reports)

Dividend Update: The bank will not be paying dividend in June 2020 and has decided to defer the payment. The decision was taken considering the uncertain economic and operational conditions of the country led by the health crisis of COVID-19, that has not left WBC untouched being one of the largest banks in Australia and barometer of the economy. Westpac Banking Corporation has notified an unfranked interim dividend of $0.1650 per security for underlying securities of Orica Limited, which is to be paid on 08 July 2020. However, the Board will continue to review the dividend options over the course of this year.

Future Expectations: The bank is prioritizing to protect and build value for the long term. It has a growing customer base and simplified portfolio with strong balance sheet. WBC is targeting to provide sustainable long-term value for its shareholders and is resetting its cost base. However, in the short term, the bank expects various headwinds on earnings and is anticipating a deteriorating operating environment to continue.

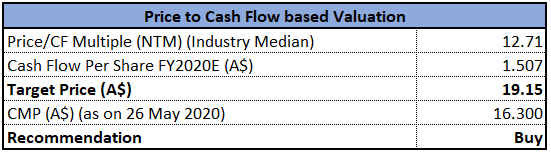

Valuation Methodology: Price to Cash Flow Multiple Based Approach (Illustrative)

Price to Cash Flow Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of WBC is trading close to its 52-week low levels of $13.470, proffering a decent opportunity for accumulation. The bank retains a strong balance sheet and has sufficient liquidity to navigate this uncertain macroeconomic environment posed by COVID-19. Considering the current trading levels, strong balance sheet and positive long term outlook, we have valued the stock using price to cash flow multiple based illustrative relative valuation method and have arrived at a target price with an upside of low double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $16.30, up by 6.327% on 26 May 2020.

Commonwealth Bank of Australia

CBA Sale of 55% Stake in Colonial First State: Commonwealth Bank of Australia (ASX: CBA) is a leading provider of financial services. As on 26 May 2020, the market capitalization of the company stood at $104.43 billion. The bank has recently entered into an agreement to sell a 55% interest in Colonial First State to KKR. Completion is expected to occur in the first half of calendar year 2021. On 19th May 2020, Genevieve Bell and Robert John Whitfield, directors in CBA, acquired 166 and 223 ordinary shares in the bank, respectively.

Strong Capital Position and Liquidity: The bank has recently released its results for the quarter ended 31 March 2020, wherein it reported strong deposit funding, significant excess liquidity, and unquestionably strong capital. The operating execution delivered growth in volume in core markets with a decline in underlying expenses by 1%. In the same time span, the bank reported cash NPAT of ~$1.3 billion, which was impacted by COVID-19 and customer remediation.

Strength in Funding and Liquidity (Source: Company Reports)

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of CBA gave a negative return of 26.51% on the YTD basis and a negative return of 0.93% in the last one month. The stock is trading at attractive levels, close to its 52-weeks’ low level of $53.44. Considering the current trading levels, decent financial and operational performance and uncertainty in the markets because of COVID-19, we have valued the stock using price to earnings multiple based illustrative relative valuation method and have arrived at a downside of lower single-digit (in percentage terms). Hence, we recommend our investors to keep an eye on the business activities and suggest a watch stance on the stock at the current market price of $61.31, up by 3.933% on 26 May 2020.

Daily Comparative Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...