Bank of Queensland Limited

.png)

BOQ Details

Decent 1HFY18 Results: Bank of Queensland Limited (ASX: BOQ) has delivered a decent 1HFY18 results with cash earnings of $182 million, representing a four per cent increase on 1H17 and a statutory net profit after tax of $174 million, an increase of eight per cent on year on year (YoY) basis. Revenue growth has remained subdued because of the intense competition in mortgage and term deposit markets. However, the lending growth across the Group has improved in 1HFY18 as the bank maintained its strategy on Retail and BOQ business. This led to a total lending growth that amounted to $671 million in 1HFY18 as compared to the contraction of $157 million in 1HFY17. The group’s balance sheet remains healthy with an increase in its Common Equity Tier 1 ratio (CET1) of three basis points to 9.42 per cent during the aforesaid period. Its net interest margin improved 1 basis point to 1.97%. The Board of Directors declared to pay an interim ordinary dividend of 38 cents per ordinary share fully franked which is consistent with 1HFY17 and 2HFY17. Furthermore, the business continued to focus on taking a prudent approach to credit risk and regulatory compliance, investing in technology and operating model simplification to enhance customer offerings and drive future business capability, while maintaining strong cost disciplines. On the other hand, the group has announced the sale of St Andrew’s Insurance business to Freedom Insurance Group Ltd for the total consideration of $65 million. Additionally, this deal is included in three-year distribution agreement for the provision of life insurance products to BOQ customers.

.png)

Key Drivers of the 1HFY18 Results (Source: Company Reports)

Meanwhile, BOQ stock has fallen 12.71 per cent in three months as on April 16, 2018 and fell 2.4% on April 17, 2018 as the market was expecting more from the group’s first half result. While the banking sector is witnessing an industry slowdown in terms of low credit growth, low interest rates, regulatory uncertainty, increasing consumer expectations, and increased scrutiny of conduct and culture, Royal Commission into the major four banks, BOQ is expected to mitigate the challenges through efforts that helped it witness mortgage lending that was over the average increase across the banking sector. Hence, we give a “Hold” recommendation on the stock at the current price of $ 10.660.

.png)

BOQ Daily Chart (Source: Thomson Reuters)

AMP Ltd

.png)

AMP Details

Confession on False or Misleading Statements made to ASIC: AMP Limited’s (ASX: AMP) stock tumbled 4.412 per cent on April 17, 2018 as the group was held guilty for misconduct at the royal commission and agreed that it made false or misleading statements to the Australian Securities and Investments Commission (ASIC) relating to issues on charging fee for no service being provided to its clients. On the other hand, the Group delivered improved results in FY17 and reported 347% rise in statutory profit and 114% on an underlying basis.

.png)

Underlying Profit Movement in FY17 (Source: Company Reports)

The profits surged up due to the recovery in Australian wealth protection earnings and strong operating earnings growth from AMP Bank (+17%) and AMP Capital (+8%). Harris Associates Investment Trust and its related bodies became the substantial holder of the Group since April 09, 2018, by securing 145,461,557 securities with 5.04 per cent of the voting power. On the other hand, the group and its related bodies is no longer substantial holder of Viva Energy REIT. Recently, the Group’s CEO confirmed his intention to retire around the end of 2018 and the Board will commence a search for his replacement. Meanwhile, the share price was down by 7.39 per cent in three months as on April 16, 2018. Looking at the developments, we maintain our “Expensive” recommendation on the stock at the current market price of $ 4.550.

.png)

AMP Daily Chart (Source: Thomson Reuters)

Medibank Private Limited

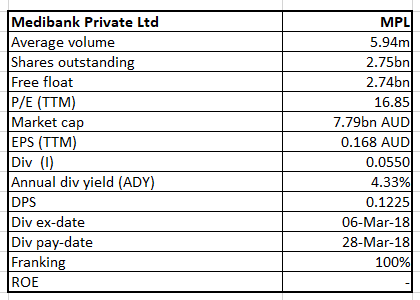

MPL Details

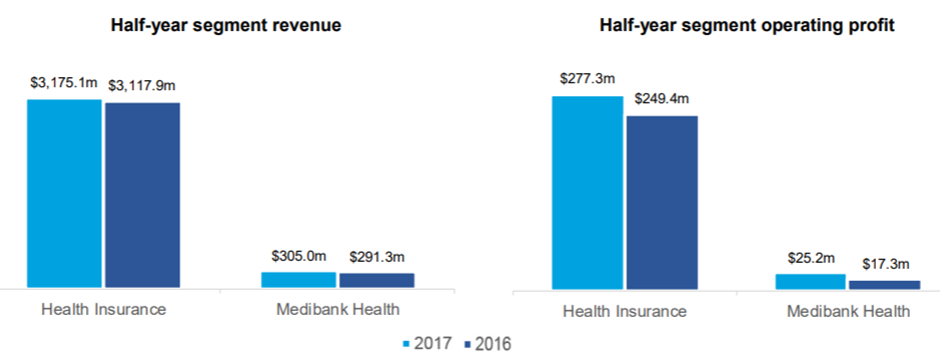

Slow industry volume growth in Health Insurance: Medibank Private Limited (ASX: MPL) is the second largest health insurance company in Australia. The group’s stock has been down by 13.7% this year to date (as at April 17, 2018) as it revealed mixed result for six months ended 31 December 2018 wherein, the Group’s net profit after tax increased 5.9% to $245.6 million in 1HFY18 from $231.9 million in 1HFY17 on the back of solid results from the Health Insurance and Medibank Health businesses. On business segment wise performance, Health Insurance premium revenue grew by 1.8% and amounted to $3,175.1 million and operating profit increased to $277.3 million, up from $249.4 million in 1H17. Medibank Health Revenue rose by 4.5 per cent and amounted to $291.9 million and operating profit rose by 45.7 per cent and reached to $25.2 million as compared to the same period in the last year.

Business Segment-Wise Performance (Source: Company Reports)

Medibank Health profit is the result of strong improvement in operating performance across all businesses, including the acquisition of HealthStrong and an increased contribution from diversified insurance businesses. However, net investment income fell by 22.3% to $59.7 million which was largely impacted by lower equity and credit market returns and a more defensive portfolio position during the period. The company is now positioning for growth which will allow to build the core business and transform into a broader health services company. The company continues to invest in the chronic disease management programs and expand footprint in the home programs. Despite the fall in the stock price, the stock looks “Expensive” at the current market price of $ 2.81 given the challenging scenario entailing factors such as slow industry volume growth in Health Insurance.

.png)

MPL Daily Chart (Source: Thomson Reuters)

HUB24 Limited

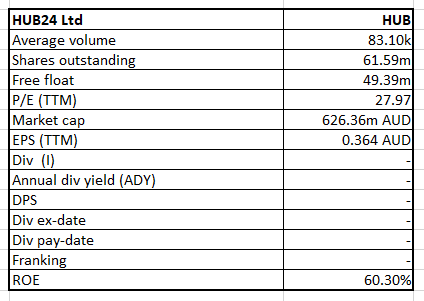

HUB Details

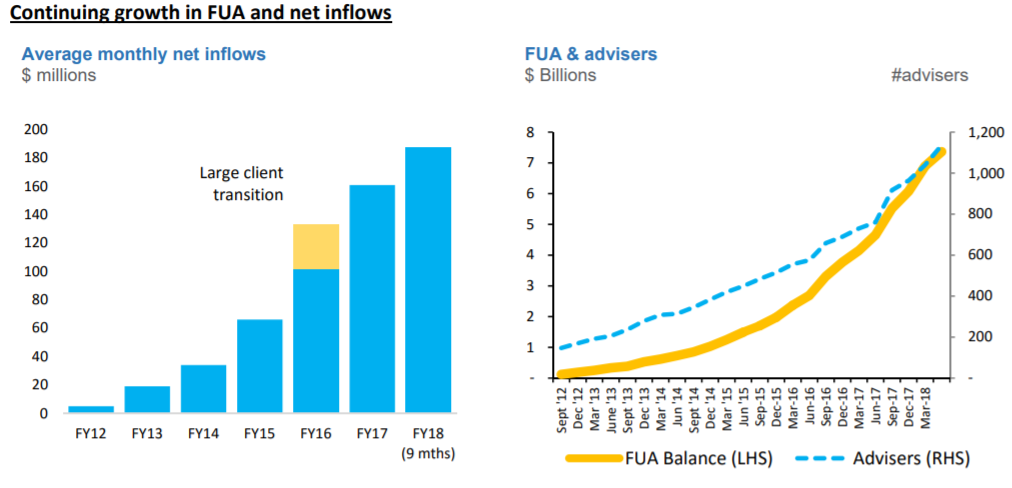

Strong Q3 FY18 performance: HUB24 Limited’s (ASX: HUB) stock zoomed up 5.211 per cent on April 17, 2018 after the release of strong third quarter results. During the third quarter, the group achieved net inflows of $595 Mn, marking a growth of 58% on the prior corresponding period. The inflows were majorly driven by the high-quality services and ongoing investment through its new and existing advisors during the period. Gross inflows stood at $820 Mn in 1HFY18. As a result of this, Funds under Administration (FUA) reached at $7.4 Bn at 31 March 2018, representing growth of 58% on the prior corresponding period. As per the latest market share data, the group has recorded 13.9% of net inflow in the December quarter. The market share of FUA has thus grown by 0.8% as at 31 December 2017 from 0.7% at June 2017. During the quarter, 96 new advisors were introduced to the platform across all licensees while 17 distribution agreements were signed with new licensees.

Continuing Growth in FUA and Net Inflows (Source: Company Reports)

On the other hand, the Group has launched new label version of HUB24 platform for a private wealth licensee. Net inflows have already commenced, and this new licensee will shortly commence using HUB24’s next generation managed portfolio capability which will be launched to the market in the next few weeks. Apart from aforesaid development, the group has signed another new white label client which is expected to be launched in August 2018. The stock price was up by 12.75 per cent in the past six months and still has room for growth. We give a “Hold” recommendation on the stock at the current market price of $ 10.700.

.png)

HUB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...